Analys

More US shale oil – But it will be needed

The front month Brent crude oil contract lost 2.4% yesterday with a close of $53.64/b. The longer dated contracts also lost some territory but not as much. Thus the front end of the curve pushed lower as the overly brave bulls who charged into the new year with record high net long WTI speculative positions took cover and shed some of their long specs. Last night the US EIA lifted its US crude oil production forecast for 2017 which also helped to push down the price. At the low Brent traded down to $53.58/b and thus just below the technical level of $53.63/b which we envisioned it would breach in this highly speculatively driven sell-off. We think that few envision that Brent crude at sub-$50/b is a viable price in H1-17 amid OPEC production cuts tightening up the market. If last night’s low of $53.58/b turns out to be the low point remains to be seen. However, we do think that buying in the territory between the current price of $53.88/b (this morning) and down to $50/b is probably as good as it gets for buyers in H1-17. Thus it comes back to this itching decision: Buy now at $53.88/b or hold out for possibly yet lower prices? This evening we have the US EIA’s oil inventory data at 16:00 CET and preliminary data points to no optimism for the bulls this time. The US API last night indicated that US oil inventories last week developed as follows: Crude: +1.5 mb, Gasoline: +1.7 mb and Distillates: +5.5 mb. So up across the board. On Friday we are probably going to see the first weekly rig count which was not impacted and overshadowed by the Christmas holidays. Also it is going to be now a full 6 weeks since OPEC decided to cut production back in Nov 30th and as such the effect of higher prices should start to filter through to higher rig counts. Thus still some bearish events which might hit the oil price bearishly. However, since the start of the year we have seen some increasing instability in both Libya and Nigeria which quickly could turn expectations for higher production to disappointment and thus higher prices.

The US EIA lifts projected US crude production yet higher – Will be the norm in H1-17

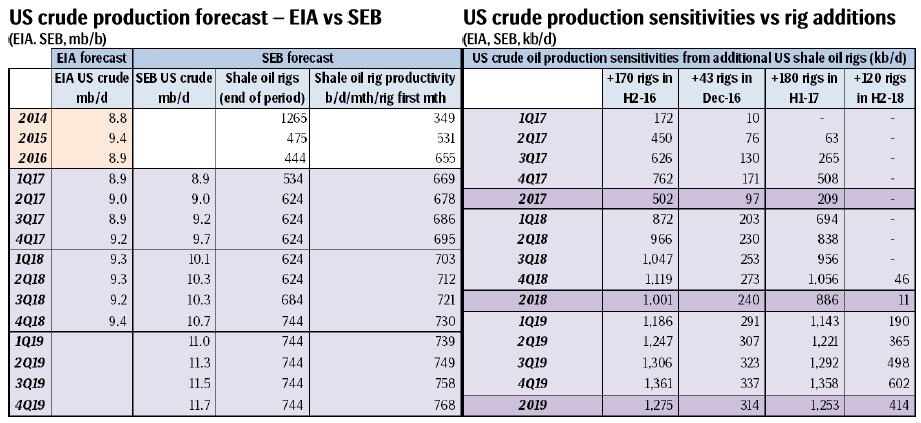

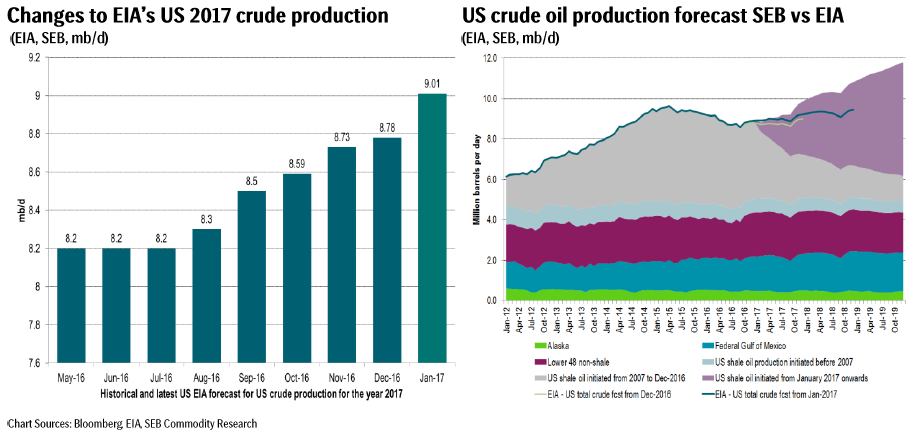

The US EIA yesterday released its January Short Term Energy Outlook (STEO) with yet another solid revision higher for its forecasted US crude oil production. For 2017 it lifted its predicted US crude production by 230 kb/d to 9.01 mb/d on average. Going back to July 2016 it has thus lifted its 2017 prognosis by 810 kb/d. Back in July 2016 it probably assumed no additions of US shale oil rigs for H2-16. A total of 170 rigs were however added into the market and volume productivity also continued to rise at an annual pace of 20%. In our US crude oil model, if we keep the latest updated shale oil volume productivity fixed at latest updated level and move the 170 shale oil rigs added in H2-16 in and out of our model we get a delta production of 502 kb/d of additional US shale oil crude production for 2017 delivery. Back in 2016 we stated that September 2016 probably would be the low point for US crude oil production. That is now also the forecast from the US EIA.

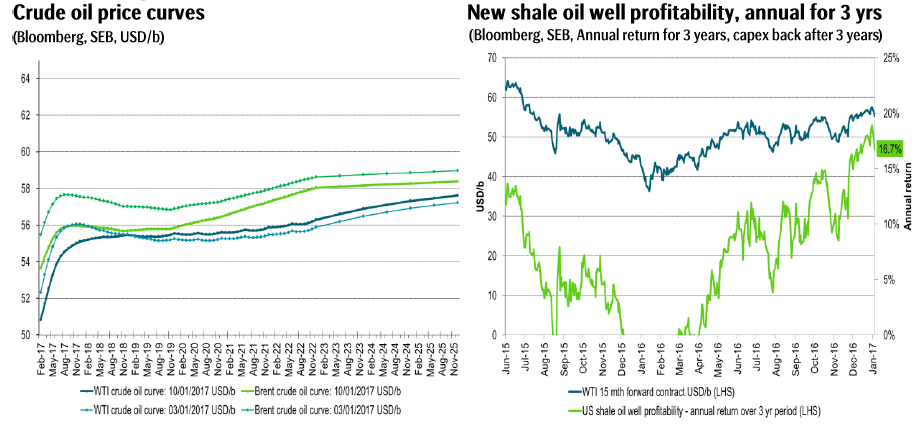

Our calculated return for a new shale oil well investment show that the annual, 3 year return, all money back after 3 years, no tail production profits had an average return of 1.2% in H1-16, 11.3% return in H2-16. Since OPEC decided to cut it has however averaged 16.7% boosting the incentive to invest yet further.

For H1-17 we expect 30 rigs per month or a total of 180 rigs for the half year to be added to the market as oil prices stay at $55-60/b during the period. In our view +180 rigs for H1-17 is a cautious estimate given that profitability for new shale oil investments will be substantially higher in H1-17 than in H2-16. We calculate that the extra 180 rigs in H1-17 will add 209 kb/d to our supply forecast for 2017 and 886 kb/d to our supply forecast for 2018. Only by bringing no additional rigs going forward do we get a US crude oil supply forecast on par with the latest US EIA forecast. As such we expect 30 rigs to be added each month through H1-17 and following we expect the US EIA to lift its 2017 and 2018 US crude oil production every month accordingly. Thus the relentless increase in US EIA’s forecasted US crude production which we experienced through H2-16 is set to continue also in H1-17. As far as we can see the US EIA hardly assumes any additional US shale oil rigs to be added into the market in H1-17 versus what is already active at the moment. We calculate every 30 shale oil rigs added and activated in H1-17 will add approximately 150 kb/d to the US 2018 crude production.

We expect to see constant revisions higher for US shale oil production in H1-17 by the EIA. This is not necessarily so bad because we think the oil will be needed. But the market will not need more rigs in H2-17 and the oil price has to adjust lower in H2-17 in order to avoid yet more rigs into the market.

Selected graphs and tables

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking