Analys

US oil fundamentals deteriorating much more than global

US equities gained 1% yesterday and the USD index pulled back 0.2% but neither commodities in general nor oil prices specifically got any tailwind from that. Brent crude pulled back 1% ydy to $58.74/bl and the whole forward curve moved down more or less comparably much. This morning Brent crude is recovering some of its losses gaining 0.4% to $59/bl.

Despite the ongoing overarching bearish oil sentiment the Brent crude front month has continued to bounce off at around $57.5/bl more or less every time a flurry of sell-off has hit the contract. It is clear that the spike in oil prices and the strong increase in front-end backwardation from those spikes have fallen back since the attacks on Saudi Arabia some weeks ago.

Deteriorating US crude fundamentals places increasing bearish pressure on WTI. Permian pipes to USGC are not enough. USGC ship-out capacity is needed as well. This leaves more control to Saudi Arabia and more bullishness to Brent crude. An important detail here is that the WTI crude curve structure has weakened much more than the Brent structure and that the front month spread between Brent and WTI has widened out from a low of $3.5/bl in mid-Aug to now $5.9/bl. I.e. it is not enough to get a large increase in the pipeline capacity feeding oil out of the Permian basin. One needs to load it onto ships and send it out of the US Gulf as well.

Obviously there is a bottleneck here getting oil out of the US leading to increasingly bearish local fundamentals in the US geography. US crude stocks are rising as a result and especially so because US refinery activity now is at a low seasonal level as well. US data on this tomorrow at 17:00 CET.

The Brent – WTI spread has widened out and the WTI crude curve structure has weakened much more than the Brent structure which basically has stabilized. With a large part of the speculative oil market being WTI-centric this has a very important impact on the overall oil market sentiment. “US oil fundamentals are weakening” = “global oil fundamentals are weakening” is a typical market conclusion. I.e. the bearish US crude sentiment rubs off on the global oil sentiment.

The widening Brent – WTI front end price spread helps to depress US WTI as well as Permian crude prices with the Permian local crude oil price currently pricing at $53.2/bl. This will help to depress drilling activity going forward.

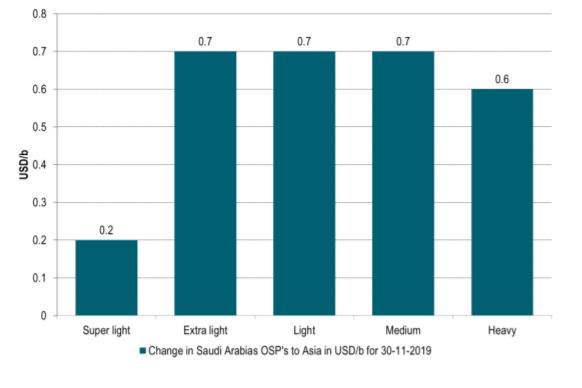

Saudi Arabia Official Selling Prices higher for all grades to Asia for November. The Brent crude oil curve is still in clear backwardation signalling a globally tight physical market. The front end price has so far defied much price action below the $57.5/bl. On interesting fact is that Saudi Arabia’s lifted all its latest OSP’s (Official Selling Prices) for November crude deliveries to Asia by $0.2-0.7/bl with all OSPs now above the 10 year average values.

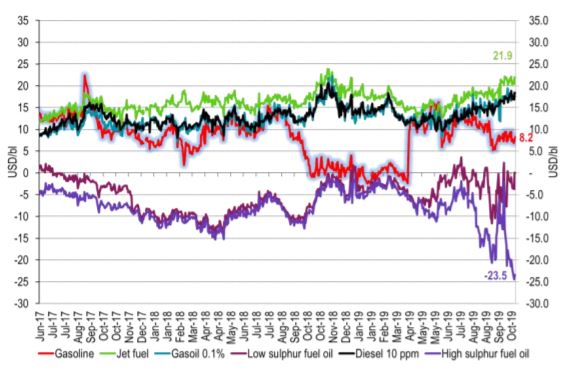

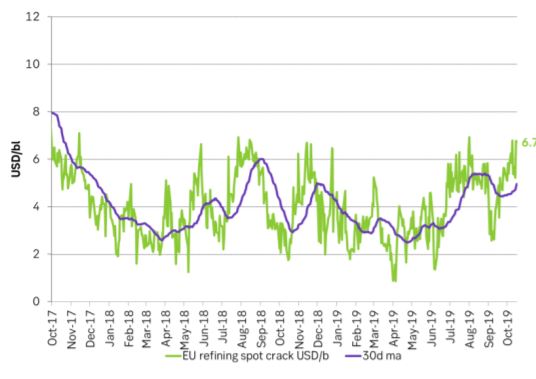

EU refining margins close to two year peaks. HFO 3.5% fuel drops like a rock and shipping consumes much more fuel. European refining margins are close to peak levels versus the peaks over the past 2 years. Middle distillate stocks are well below the 5-year average as we run into the northern hemisphere winter and the IMO-2020 is now kicking in harder and harder. What we see in the charts is that the high sulphur bunker oil spot price continues to fall like a rock versus Brent crude and is now trading at only $35.5/bl in the ARA region. The interpretation of this is that there is a surplus of this oil product in the market because it can soon no longer be legally used in the transportation sector. This product is being kicked out of the market and some other product needs to take its place instead. This is a tightening of the global liquids market which can be used for transportation uses. The skyrocketing tanker freight rates also means another thing: much higher shipping fuel consumption. The higher the rates, the faster the ships go and the more they consume. Much more.

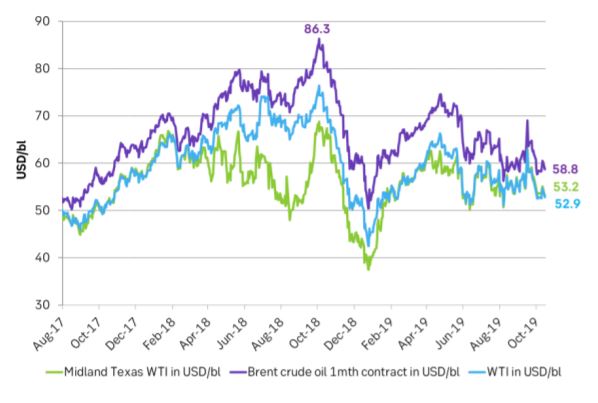

Ch1: The Brent to WTI price spread was close to $10/bl and then deteriorated all the way down to $3.5/bl in early August as new US pipelines from the Permian to the USGC came online. Lack of shipping capacity has however blown the two grades apart again to now close to $6/bl. I.e. US crude is again locked in leading to increasing localized US bearish and WTI bearish pressure.

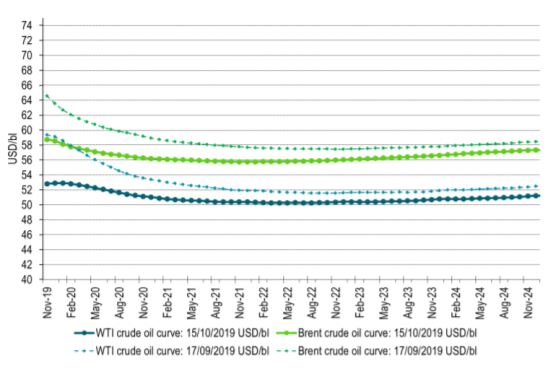

Ch2: Brent and WTI forward crude curves. Structures have weakened but WTI much more than Brent

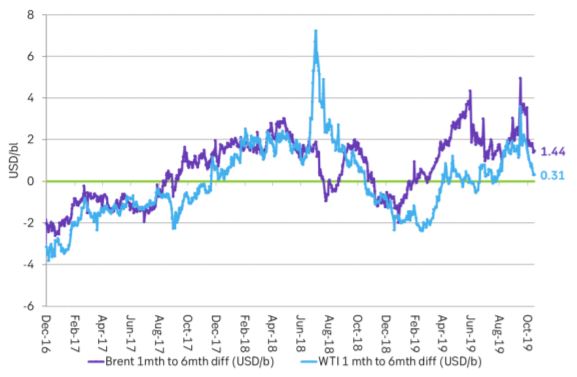

Ch3: The 1-6 month backwardation for Brent and WTI. For WTI now close to zero. For Brent down to $1.4/bl

Ch4: All crude grades are lower. But the increaseing spreads helps to push Permian basin below average levels for this year

Ch5: Saudi Arabia lifted OSPs for all grades to Asia for November

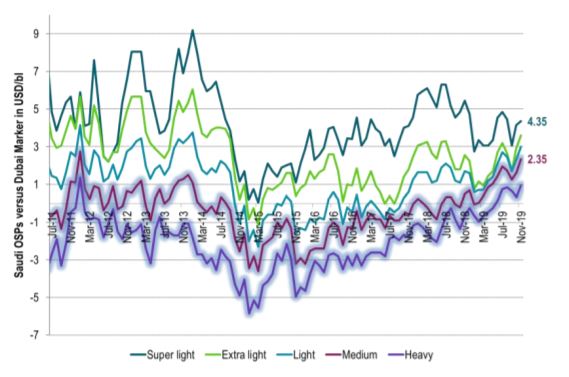

Ch6: Saudi Arabia’s OSPs to Asia ticking higher

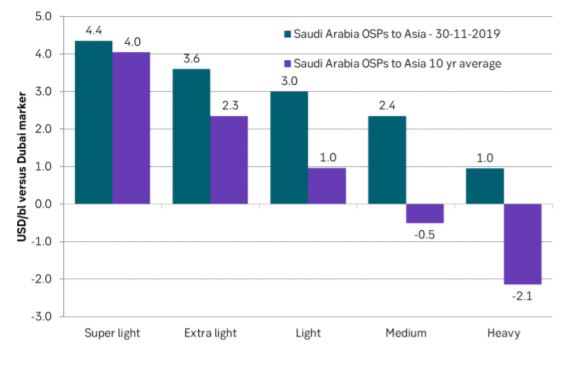

Ch7: Saudi Arabia’s OSPs are above the 10yr average for all grades to Asia

Ch8: The price of High Sulphur bunker oil (HFO 3.5%) continues to drop like a rock versus Brent crude in ARA. Mid-dist cracks continues to tick higher and we think it is just a matter of time before they jump higher.

Ch9: European spot refining margins are close to two year peaks

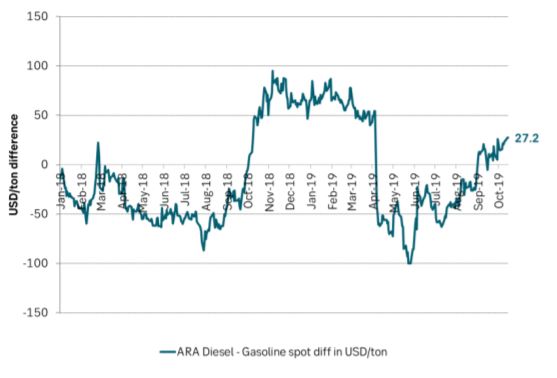

Ch10: ARA Diesel versus Gasoline. Diesel prices are getting relatively stronger and stronger but gasoline prices have not yet crashed to zero.

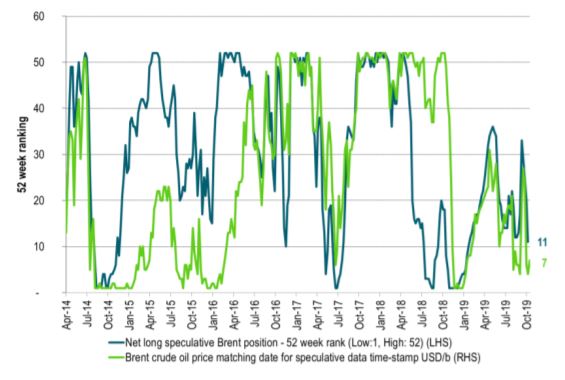

Ch11: Ranking versus 52 past weeks of Brent crude price and the net long speculative positions in Brent crude. Both are getting close to 52 weeks lows but not quite there yet.

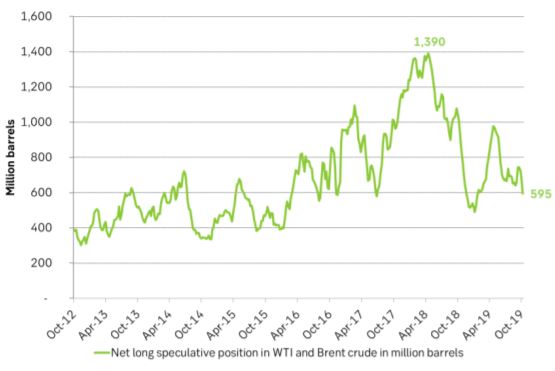

Ch12: Net long Brent and WTI speculative positions at fairly low levels but not yet all the way to the very lows.