Analys

The WTI bulls are coming. Curve set to flip to backwardation

A cocktail of bullish factors are hitting the supply side.

We have ongoing cuts by OPEC+.

Venezuela is deteriorating rapidly with latest news that due to a blackout its main port is now closed (accounts for about 90% of exports). The country exported 1.7 m bl/d of crude in early 2017 which declined to 1.25 m bl/d in 2018 but now rapidly seems to head to zero.

Algeria is the new runner up with crowds marching the streets while the military chief of staff is demanding that the 20 year ruling president Bouteflika should step down. US sanctions towards Iran are up for renewal in May and the US has signalled that it may be difficult to extend waivers. Algeria is today producing some 1 m bl/d.

Iran. The name of the US sanctions game is “a tightening screw”. It will likely still be possible for S. Korea and others to import oil from Iran, but the quota will most likely shrink in May. How much will depend on the oil price.

If the price is too high in the eyes of Donald Trump he may roll the current waivers forward in order to protect the US consumers (and his voters). US economic advisors have however recently stated that a higher oil price is now a positive for the US economy as it increasingly becomes an oil exporter. The negatives for the consumers are outweighed by the positives for the producers if the oil price is high. I.e. the US is becoming more like OPEC J.

US shale oil on debt dieting. The end of the shale oil boom or the slow-down of the shale oil boom has been called time and time again. There is no doubt that the boom so far has been fuelled by debt and that the industry is still largely running cash flow negative. Some macro analysts have lately stated that companies in general will start to deleverage. If that is the case then this will surely also be the case for US shale. Latest signals from the industry is Schlumberger stating this week that they expect a double digit drop in spending from its customers in North America this year (blbrg). Underlining this is Devon Energy which signals that it will cut its headcount from 2500 to only 1700. So maybe we now finally do see a slowdown in US shale oil production growth. There are however many sides to the US shale story of which one is that the industry completed the highest number of wells in February (1325) since 2015 in nominal terms and the highest ever in real terms. They still completed more than they completed.

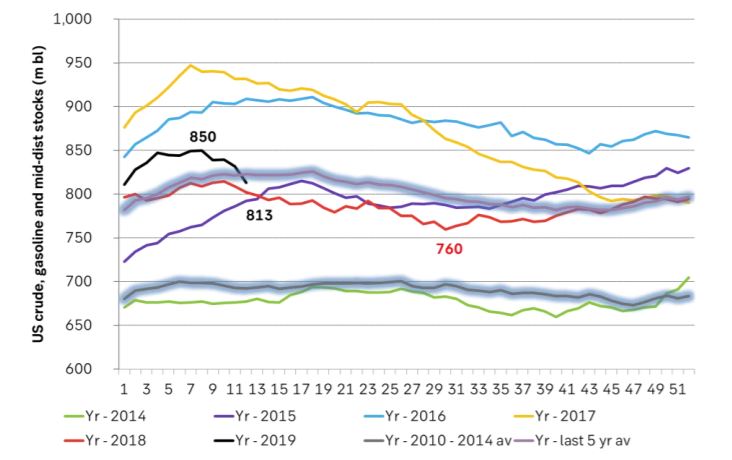

US oil inventories. API yesterday reported indicative numbers for US oil inventories last week. Crude: +0.7 m bl, Gasoline: -3.5 m bl and Middle Distillates: -4.3 m bl/d. Over the past 8 weeks the US crude, gasoline and middle distillate stocks have declined by 34 m bl. The seasonal normal (past 5yrs) is for a rise of 23 m bl. In total it equates to a seasonally adjusted draw of 57 m bl. Today at 15:30 CET we’ll have the actual data. But all indicates that we’ll get another solid draw overall for crude and products today.

Bulls, WTI, Brent, OPEC cuts and spec. We have argued several times that cuts by OPEC+ was a two stage process. 1) Dry up the global market and the Brent crude curve. 2) US exports rise and imports decline and the US market dries up as well. This is exactly what has happened. Over the past 8 weeks exports were 27 m bl higher in comparable terms to Q4-18 while imports were 14 m bl lower in comparable terms to Q4-18.

Crude curve convergence. Bulls coming to WTI. The consequence of the above point was that bulls were first to run into the Brent crude curve. Now that the US inventories are drying up the WTI curve is increasingly firming and bulls are piling in.

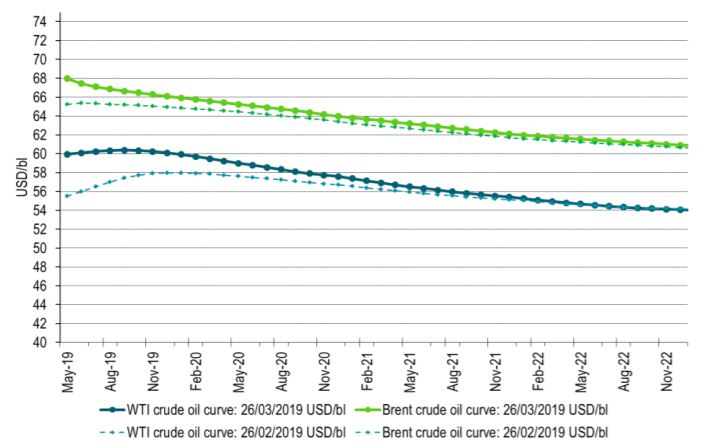

Ch1: Global market and the Brent crude curve firmed first. Now the WTI crude curve is just around the corner to shift into full backwardation as well. That will fuel the bulls to run towards positive roll yields in the WTI curve. It will lift WTI. The WTI front end contango has held back gains for Brent. So backwardation also in WTI will help to free the Brent bulls

Ch2) Sharp delcline in US crude, gasoline and mid-dist inventory as imports decline and exports rise

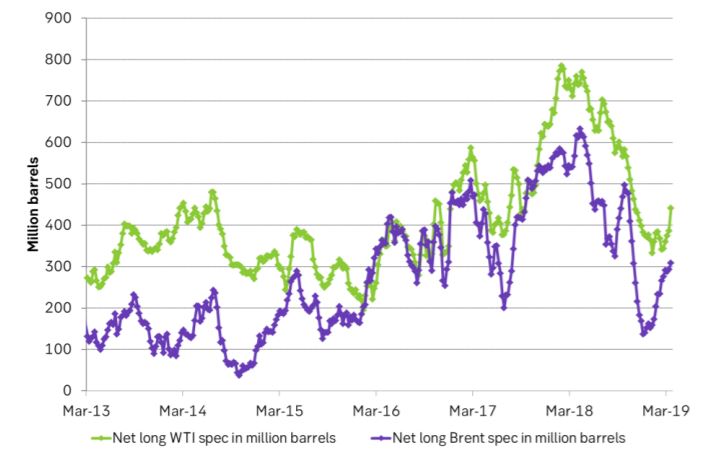

Ch3) Brent bulls came first. Now the WTI bulls are coming

Ch4): Brent and WTI crude curve convergence. The WTI crude curve shape is rapidly shaping up to the Brent curve shape