Analys

The thematic case for nickel

Nickel has exciting long-term prospects as its use in electric vehicle batteries is expected to drive its demand growth in the future. This structural trend has however not immunised it against the recent headwinds facing industrial metals. Industrial metals are cyclical commodities and their performance is fuelled by global economic growth. The sector has therefore been under pressure from trade wars and, more recently, coronavirus. In this blog, we want to shift the focus back to nickel’s strategic case. We remain cognizant that the current storm is not over yet but expect a smoother sail once the existing headwinds subside.

Analysing nickel’s recent history

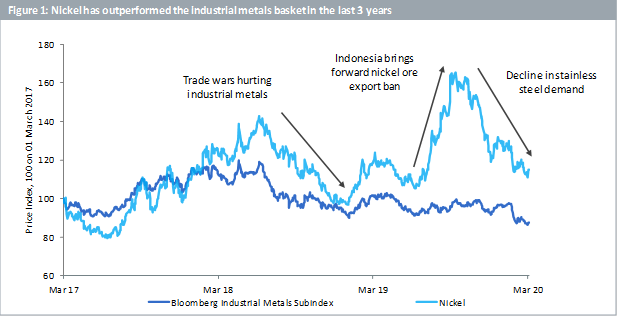

Nickel has strongly outperformed the industrial metals basket (composed of copper, zinc, aluminium and nickel) in the last 3 years (Figure 1). The sector has faced challenges since the advent of trade wars in 2018 both directly due to tariffs and indirectly via a resulting slowdown in global economic activity. Nickel too has had its share of price volatility during this time. The metal rallied sharply in July 2019 on the expectation that Indonesia, which produces a quarter of global nickel supply, will bring forward its nickel ore export ban by 2 years to January 2020. Indonesia announced this decision soon thereafter. Concerns of supply shortages drove the price in a market which was already in a deficit[1]. Nickel’s fortunes reversed in the last quarter of 2019 as stainless-steel demand, which currently accounts for nearly two-thirds of the metal’s use, dwindled. The dynamics of the nickel market are however changing which is why we have an optimistic view of the future.

Battery solutions to take a larger share of nickel

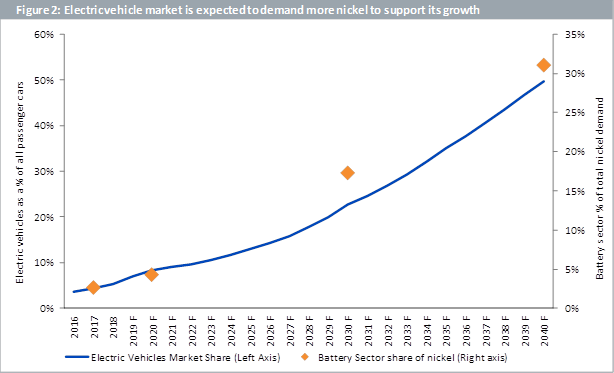

According to metal experts Wood Makenzie, battery solutions are expected to account for more than 30% of the total demand for nickel by 2040, up from around 4% today (Figure 2). This is because electric vehicles are forecasted to be around 50% of all passenger car sales by 2040, up from around 8% today. Batteries need to become more efficient to enable this growth and nickel is expected to play a pivotal role. According to the Nickel Institute, nickel containing Lithium-ion batteries are powering the electric vehicle revolution as nickel in batteries helps deliver higher energy density and greater storage capacity at a lower cost. This will allow electric cars to have both a longer range, i.e. the ability to drive longer distances without requiring a recharge, and lower cost promoting wider adoption.

Now, the impact on price from demand growth can, in theory, be offset by an equal increase in supply. We, however, believe that supply growth will be much slower as, according to Wood Mackenzie, the average time for a new nickel mining project to start producing the metal is around 9 years. Miners will seek higher prices to be incentivised to undertake such projects.

It is uncertain how quickly the current headwinds facing industrial metals will dissipate. Having said that, the market dynamics of nickel are changing and the long-term outlook appears promising for the metal supported by a thematic shift towards electric vehicles which is being powered by nickel containing batteries. With the nickel market already in a supply deficit, we expect growing demand to support its price in the long-term.

Mobeen Tahir, Associate Director, Research, WisdomTree

[1] According to the International Nickel Study Group, nickel’s supply deficit was 6.2% in 2018, 3.2% in 2019 and forecasted to be 1.8% in 2020 relative to its demand based on data available as of 31 October 2019.

DISCLAIMER

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.