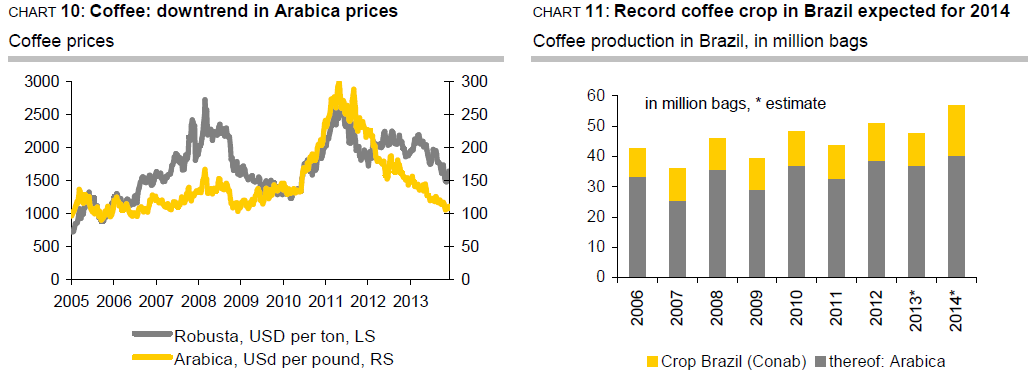

Arabica’s years-long downtrend has led the price of this coffee to its lowest level since 2006 (see chart 10 below). For a brief time it was even feared that the price would fall below the USD1 per pound mark. Moreover, the price looks like it will remain muted going forward as well: if Brazil’s current low-yield year for Arabica couldn’t boost prices and the roya (coffee rust) epidemic affecting a large part of Central America was only able to lift them briefly, we see little hope for a trend reversal in 2014. Not only is production in Columbia likely to increase further in 2014, but above all Brazil is slated for a high-yield year.

In fact, the term “low-yield year” has lost much of its edge due to the flattening of the 2-year cycle. This year Brazil posted a record high for production in such a low-yield year and in all probability will post a record-high for production in a high-yield year in 2014. In terms of aggregate coffee volume this could translate to an increase of 10m bags to 57m bags, and some estimates even go as high as 60m bags or more. That is anything but a signal of scarcity (see chart 11 below). Such estimates are supported not only by the good weather conditions so far, but also by the overall improvement in the state of plantation. The good state of plantations, however, is due not least to investments made following the high prices of 2011. The longer the low-price phase persists, the more the investment “dividend” will shrink.

As a minimum, the current low price phase will lead to lower yields in the medium term due to scrimping on fertilizer and crop protection. So far the plantations have continued to persevere despite prices that have often fallen below production cost – but they won’t be able to hold on indefinitely. The marked increase in production costs of an estimated 12% yoy combined with low prices is likely to lower the profitability of coffee farming further. Thus, for the longer run, the ICO views the assumption of a higher coffee supply as questionable. But for now, prices are not budging, not even after the auctions of the Brazilian government, in which options were arranged for planters to deliver 3 million bags to state stockpiles in March 2014. According to the ICO, this non-reaction indicates that the market is underestimating the impact of Brazil’s policy, which it believes is likely to lead to a “precarious” balance.

But that is still a long way off: Following a number of deficit years, 2012/13 has already ended with surplus of about 3m bags as estimated by the ICO. It is still not clear how global production volume will turn out in 2013/14, as increases in Vietnam and Columbia – the latter finally having emerged from its roya Odyssey of several years, which necessitated new plantings of more robust strains – will be offset by decreases in Brazil and currently roya-plagued Central America.

At present it seems there could also be surpluses in 2013/14 and 2014/15. The more diminished outlook for the years thereafter should, however, allow prices to rise slowly, so that after an intermittent low during the Brazilian harvest in 2014 we expect the price of coffee to recover to 110 US cents per pound in Q4 2014 and continue to rise thereafter.

Since summer, Robusta prices have moved in a similarly negative fashion as Arabica prices after far outperforming them for a very long period. Nonetheless, Arabica prices remain low relative to Robusta prices when compared to their history. This should lead to a substitution of Arabica for Robusta in coffee consumption. The ICO believes this trend is already recognisable. The recent recovery of Robusta prices was largely due to the fact that Vietnam’s latest export numbers came in low despite what seems to have been a record-high harvest. The policy of holding back is apparently paying off, at least in the short run. We doubt Robusta prices will be able to escape the pressure of a plenteous coffee supply in 2014 and don’t expect its price to recover until the second half of the year – to a level of USD1,600 per ton.