Analys

The crude oil market in June – Less of a crowded place

Saudi Arabia today reduced its official selling prices (OSPs) to Asia in June and crude oil prices are bouncing 6-9% on the back of that news. It signals that Saudi Arabia sees the June crude oil market as less of a crowded place and that it will be easier for the producer to place its desired volumes into the market. In a slight parallel to this we think that it is unlikely to be a wall of surplus oil banging on the door of Cushing Oklahoma in June of a comparable magnitude of May. There is probably a limited risk for a repetition of the crash to -$40/bl for the WTI June contract when it rolls off in only 9 trading days on May 19.

Crude oil prices have today been trading a little higher and a little lower until they jumped up 6-9% as Saudi Arabia increased its official selling prices for June versus other benchmarks. Higher official selling prices (OSPs) signals that Saudi Arabia no longer is seeking to push oil into the market at almost any price.

We all know that Saudi Arabia is cutting production down to 8.5 m bl/d but what this is saying is that Saudi sees the June crude oil market as less of a crowded place than before. It will need to work less hard to get oil out the door in June in the amounts it desires.

The WTI May contract crashed oil prices on April 20th. Then prices fumbled around for a week or so before a rally kick-started at the very end of April on the back of emerging signs of demand recovery, cuts by OPEC+ and declines by non-OPEC+ producers. On Tuesday the Brent front-month contract closed above $30/bl for the first time since 13th April before taking a little breather yesterday.

It is now only 9 trading days left until the WTI June contract rolls off and expires on May 19. Attention is again coming back to what happened on April 20 when the WTI May contract expired and traded down to -$40/bl before closing at -$37/bl. The market is concerned that we might get the same kind of end-of-contract disturbances for the June contract as we got for the May contract.

If so, it is highly unlikely that we would see -$40/bl again since the market now is prepared and knows such an event might happen. It is still possible that the WTI June contract could come under intense selling pressure over the coming 9 trading days as long positions move to exit.

The special thing about the WTI contract is of course that it is based and priced in-land in Cushing Oklahoma in the US. It is land-locked with flows in and out of the storage hub going by pipelines. If inventories in Cushing are full and pipes out of Cushing are full then prices can crash.

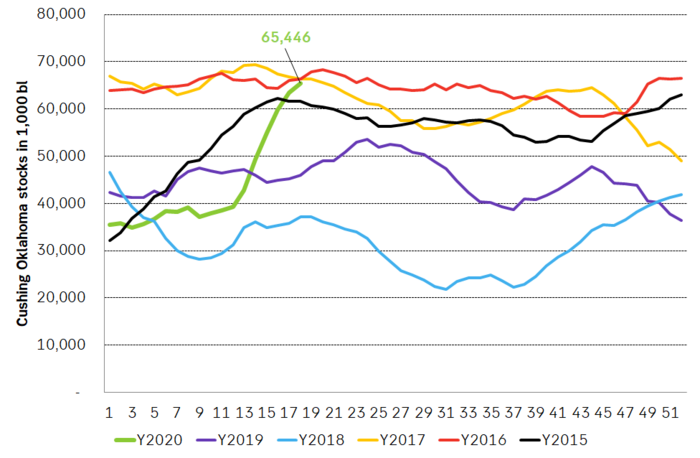

Inventories in Cushing Oklahoma have been on a continuous rise for 9 weeks. Inventories there have risen 28 m bl over this period and as of last week they stood at 65.5 m bl which is slightly below the total capacity of 76.1 m bl and on par with levels in 2016 and early 2017. Last week inventories rose by 2.1 m bl in the hub. In all practical terms the hub is now more or less full.

The number of open positions in the WTI June contract yesterday stood at 239 m bl with a comparable amount of long versus short positions. If the 239 m bl long-side of this equation decides to take these contracts to delivery in June the holders of these contracts will actually receive physical volumes in the Cushing Oklahoma physical location.

When the WTI May contract crashed to -$40/bl on April 20 there was an open position of 109 m bl at the start of the trading day. There were basically no buyers for the long positions who wanted and needed to exit since inventories were more or less fully booked for May with nowhere to take physical delivery.

At the moment we see that Cushing inventories are close to full and still rising though the growth rate in inventories is slowing since we are moving towards total capacity.

The WTI June contract however is about June and not about May. The question is thus what are the storage needs in June? How are the bookings in June? Will surplus oil just continue to flush into Cushing also in June with all pipes in and out of the hub clogged by surplus? Probably not.

Delivered oil products in the US last week stood at 25% below last year which is equal to a decline of close to 5 m bl/d. This is terribly bad, but still better than a YoY decline of 6 m bl/d in mid-April.

But demand in the US is on its way back and demand will by June most definitely be better than it is now. Maybe down only 2-3 m bl/d YoY (which is still exceptionally weak).

Supply in the US and Canada is however declining rapidly and is expected to be down by 3.5 to 4.5 m bl/d versus pre-Corona levels already in the Month of May. It turns out that shutting down a shale oil well is easy, quick and is not damaging to the overall production of the well when it is opened at a later stage.

So, if US demand is back up to within 2-3 m bl/d versus normal in June and supply in the US and Canada is down by 3.5 to 4.5 m bl/d already in May, then there shouldn’t be a massive wall of oil banging on the door of Cushing Oklahoma to get in in June as was the case in May. As such bookings for Cushing Oklahoma inventory in June should be much less strained in June than in May even if we still see rising inventories there right now.

This lowers the risk significantly for a price crash repetition on the 19th of May when the June contract rolls off comparable to what happened to the WTI May contract on the 20th of April.

US Cushing Oklahoma oil inventories rose another 2.1 m bl/d last week to 65.5 m bl which is on par with levels from 2016 and 2017 and only about 10 m bl below max storage capacity of 76.1 m bl. Inventories are in all practical terms full.