Analys

Solid demand growth and strained supply to push Brent above USD 100/b

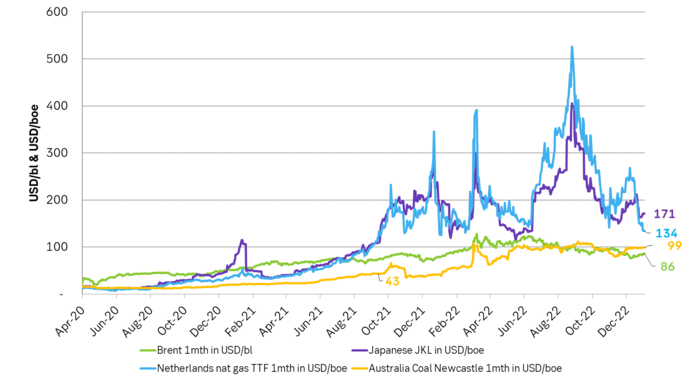

Brent crude had a strong end of the year as it traded at the highest level since 1 December. It is a slow start to the new year due to bank holidays and Dated Brent trades close to USD 85/b. It averaged USD 99.9/b in 2022. We expect it to average more than USD 100/b on average for the coming year amid strained supply and rebounding demand. Chinese oil demand is set to recover strongly along with re-openings while non-OECD will continue to move higher. At the moment oil looks absurdly cheap as it is cheaper than natural gas in both EU and Japan and also cheaper than coal in Australia.

Some price strength at the end of the year. The Dated Brent crude oil price index gained 2.3% on Friday with a close at USD 84.97/b. It was the highest close since 1 December. This morning it is trading slightly lower at USD 84.8/b but the market is basically void of action due to bank holidays.

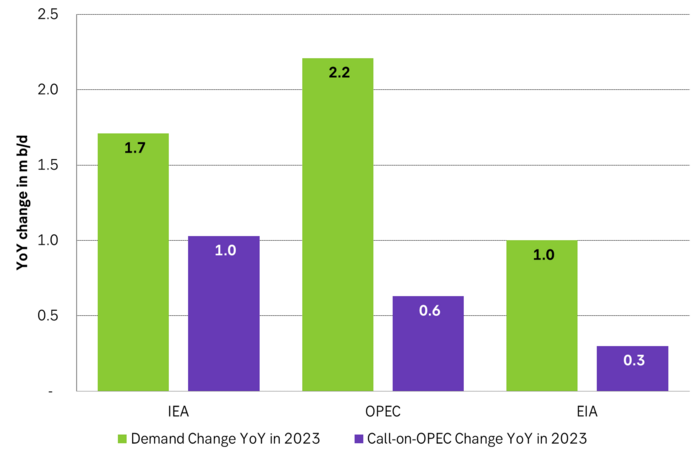

Gloom and doom but IEA, OPEC and US EIA project global crude oil demand to rise between 1 m b/d and 2.2 m b/d YoY in 2023. They also expect call-on-OPEC to rise between 0.3 m b/d and 1.0 m b/d. The US EIA projects demand to increase 1 m b/d in 2023 on the back of a growth of 1.3 m b/d in non-OECD where demand in India rises by 0.2 m b/d and China by 0.6 m b/d. In China this is of course to a large degree due to re-opening after Covid-19 lock-downs. But it is still a good reminder of the low base of oil demand in non-OECD versus OECD. India last year consumed 5 m b/d which only amounts to 1.3 b/capita/year versus a world average of 4.5 b/capita/year and European demand of 10 b/capita/year. Even China is still below the world average as its demand in 2022 stood at 15.2 m b/d or 4.0 b/capita/yr. Non-OECD oil demand thus still has a long way to go in terms of oil demand and that is probably one of the things we’ll be reminded of in 2023 as Covid-19 lock-downs disappear entirely.

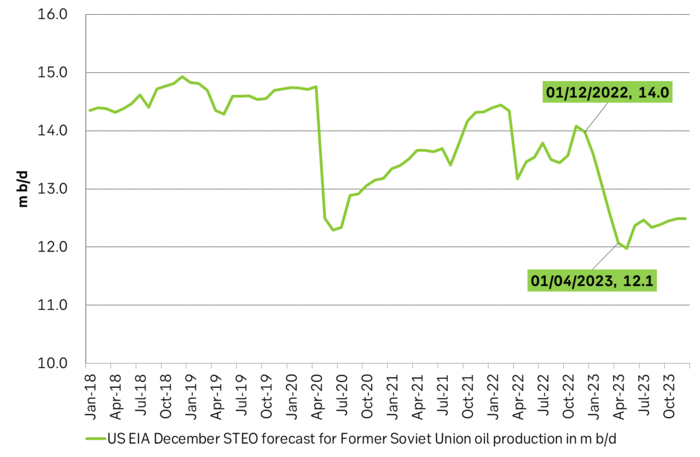

Solid demand growth in the face of strained supply. Important to remember is that the world has lost a huge amount of fossil supply from Russia due to the war in Ukraine. First in terms of natural gas where supply to the EU and thus to the world has declined by some 2.5 m boe/d versus pre-war levels. Secondly in terms of crude and products. The latter is of course a constant guessing game in terms of how much Russian crude and product exports has declined. The US EIA however projects that crude oil production in the Former Soviet Union will be down 2 m b/d in 2023 versus pre-Covid levels and down 1.3 m b/d YoY from 2022 to 2023. We are thus talking up to 4.5 m boe/d of lost supply from Russia/FSU. That is a huge loss. It is the reason why coal prices are still trading at USD 200 – 400/ton versus normal USD 85/ton as coal is an alternative to very expensive natural gas.

Overall for 2023 we are looking at a market where we’ll have huge losses in supply of fossil energy supply from Russia while demand for oil is set to rebound solidly (+1.0 – 2.2 m b/d) along with steady demand growth in non-OECD plus a jump in demand from China due to Covid-19 reopening. Need for oil from OPEC is set to rise by up to 1.0 m b/d YoY while the group’s spare capacity is close to exhausted.

We expect Brent crude to average more than USD 100/b in 2023. Despite all the macro economic gloom and doom due to inflation and rising interest rates we cannot help having a positive view for crude oil prices for the year to come due to the above reasons. The Dated Brent crude oil price index averaged USD 99.9/b in 2022. We think Brent crude will average more than USD 100/b in 2023. Oil is today absurdly cheap at USD 85/b. It is cheaper than both coal in Australia and natural gas both in Japan and the EU. This is something you hardly ever see. The energy market will work hard to consume more what is cheap (oil) and less of what is expensive (nat gas and coal).

Latest forecasts by IEA, OPEC and US EIA for oil demand growth and call-on-OPEC YoY for 2023. Solid demand growth and rising need for oil from OPEC.

Oil demand projections from the main agencies and estimated call-on-OPEC. More demand and higher need for oil from OPEC

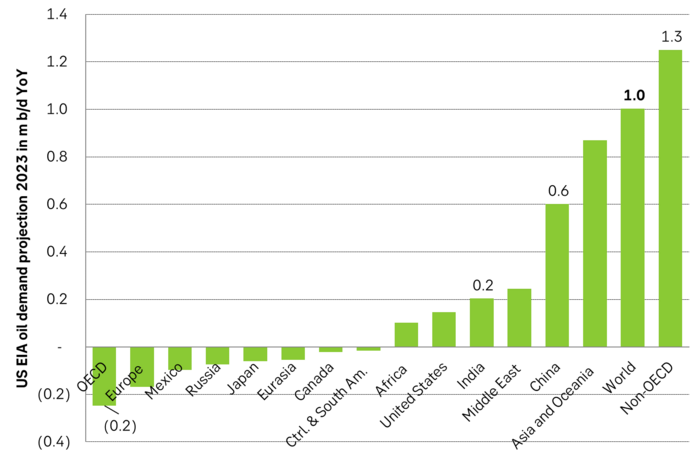

EIA STEO projected change in oil demand for different countries and regions YoY to 2023

US EIA Dec STEO forecast for FSU oil production. Solid decline projected for 2023.

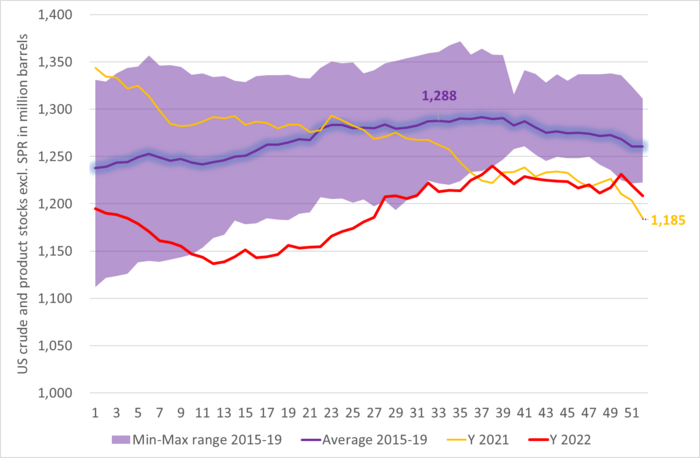

US commercial crude and product stocks still below normal

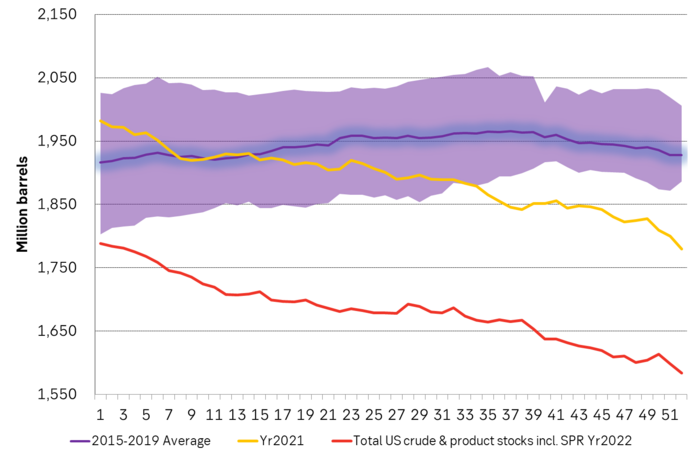

Total US crude and product stocks including SPR. Declining, declining, declining.

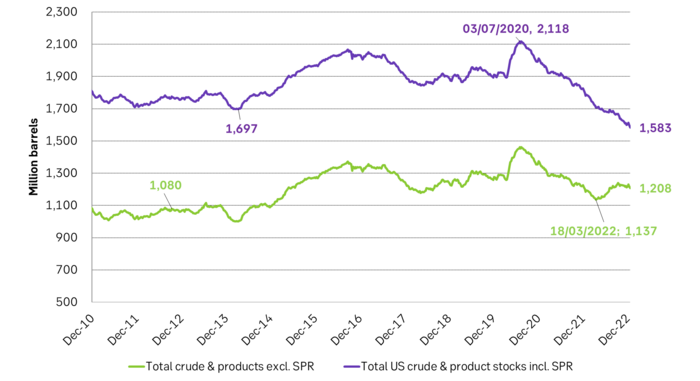

US crude and product inventories both excluding and including Strategic Petroleum Reserves

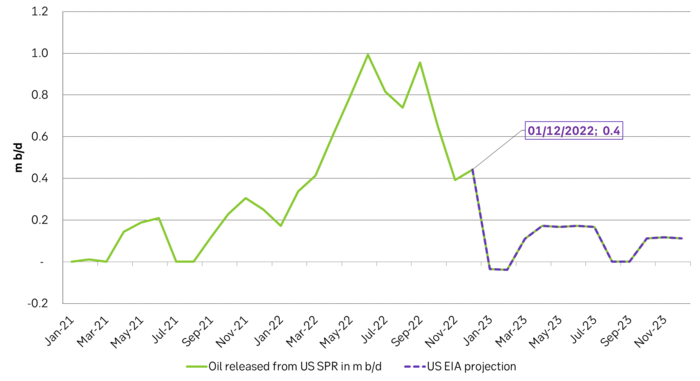

US oil sales from US SPR is now coming to an end. Will make the market feel much tighter as it really is.

Brent crude oil is absurdly cheap as it today trades below both Australian coal and natural gas in both Japan and the EU. Coal and natural gas prices should trade lower while oil should trade higher.

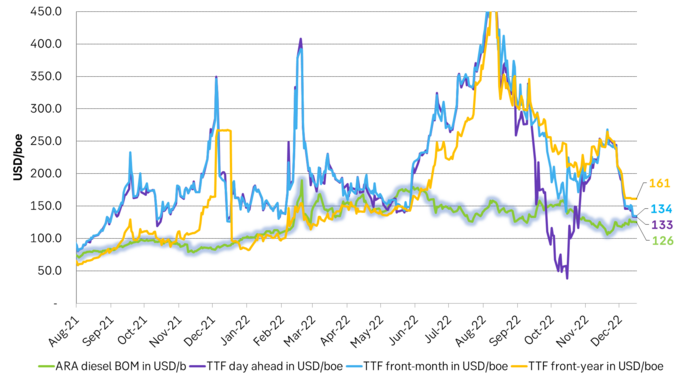

EU diesel prices versus natural gas prices. Could start to move towards a more natural price-balance in terms of substitution.