Analys

Short term recovery due for platinum and palladium

The green industrialised precious metals – platinum and palladium have started 2020 on a weak footing owing to the spread of the COVID–19 pandemic globally. The price decline for platinum, down-21.0%, has been more severe than palladium -6.83% since the start of 2020. Palladium and platinum are known to derive a large portion of their usage (accounting for nearly 34% and 84% respectively) from the auto industry.

Owing to their extensive use in vehicle auto catalysts, demand for platinum and palladium remains particularly sensitive to economic, industrial and market conditions. Falling demand from the global auto industry due to automotive shutdowns being imposed globally are denting sentiment towards both platinum and palladium. Platinum has a more diverse demand base compared to palladium. In addition to auto demand – jewellery, industrial and investment demand account for about 25%, 28% and 13% of platinum’s total usage, respectively.

However, amidst the COVID-19 crisis, both jewellery and industrial demand are expected to fall further but investment demand is likely to strength amidst the uncertainty. While the weakness on the demand side remains a key focus, we expect attention to increasingly start to shift to the supply side aiding a short-term price recovery.

The slump in auto industry should start to recover in H2 as stringent lockdowns ease

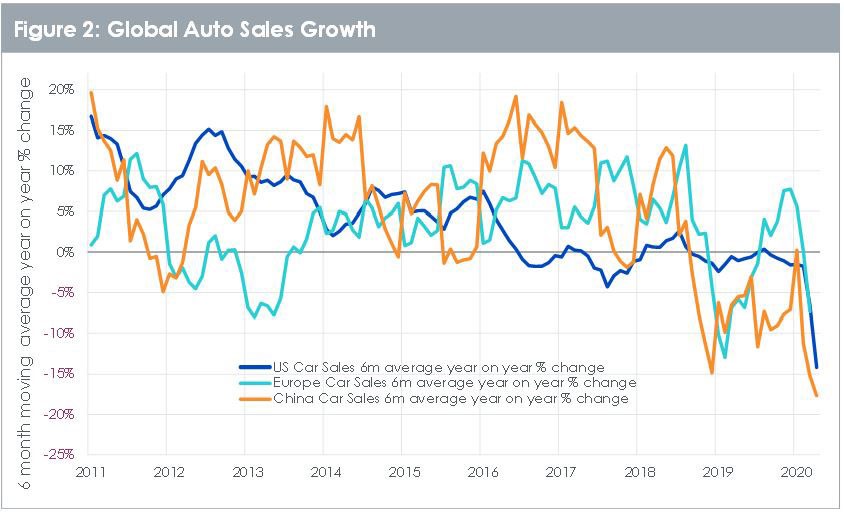

The impact of the COVID-19 crisis on the global automobile industry has been severe as production and sales of motor vehicles have come to a sudden halt globally. In the first quarter of 2020, the EU commercial vehicle market contracted by 23.2% as a direct consequence of March’s substantial slowdown. In March 2020, demand for new commercial vehicles fell by 47.3% across the EU, as measures to prevent the spread of the coronavirus led to the suspension of production at auto manufacturers.

Meanwhile in China, where the epidemic peaked in February, the market is slowly returning to normality. The Chinese automotive market recovered significantly from its prior slump in March. As the China Association of Automobile Manufacturers (CAAM) reported on 10 April 2020, car sales increased more than fourfold (compared to February) to 1.04mn units. According to reports from the CAAM, the Chinese auto industry regained around 75% of its normal operating level in March. The CAAM expects the vehicle market to continue its recovery in the second quarter although full capacity is only likely to be reached again in the second half of the year. In Europe, assembly lines are now restarting production and the same is expected in North America around mid-May.

As lockdown measures start to ease gradually across the rest of the globe, we expect to see a gradual recovery in demand for the green metals from the auto industry in the second half of the year. However, we remain cautious of end-consumer demand which is anticipated to stay weak as consumer’s propensity to purchase cars will be lower due to the economic impact of the COVID-19 crisis on their purchasing power.

Supply side destruction is likely to have a bigger impact on platinum vs palladium

South Africa’s Platinum Group Metal (PGM) producers have been hit by severe disruptions since the lockdowns have been imposed in April. South Africa produces around 38% of palladium and 75% of platinum globally. In the past, the South African mining industry faced a range of health issues, including HIV infections, and such concerns have always posed a risk to supply. The five-week lockdown in South Africa ordered by President Ramaphosa is expected to come to an end in the coming days.

While producers are attempting to prepare themselves to restart production at the mines again, the police are preventing them due to the spread of COVID-19. This implies that the current market tightness will only last for short duration. However, the process of ramping operations back to normal is likely to take time even after the shutdown period. It is also hard to determine at this stage if a second wave of infections might trigger another round of shutdowns causing supply disruptions to linger for longer. Initially the mines are expected to be allowed to operate at 50% capacity.

Palladium normally occurs as a by-product of platinum mining (South Africa) or nickel mining (Russia). About 40% of palladium’s supply comes from Russia. Supply of palladium appears to be at less of a risk as the world’s largest palladium producer Nornickel from Russia expects the global palladium market to show a small supply surplus this year for the first time in eight years.

This is because demand for palladium has been impacted severely by the COVID-19 led crisis. Nornickel reduced its 2020 estimate of palladium consumption owing to weaker global car sales. Reflecting on 2011, Gokran, the Russian state reserve fund unexpectedly supplied about 750,000 ounces out of its own stockpile which was followed by three years of palladium’s price decline. The caveat is no one knows how big Gokran’s stockpile or whether they would use this current period of weak demand for palladium to build up stockpile.

No substitution so far, despite palladium’s price premium over platinum

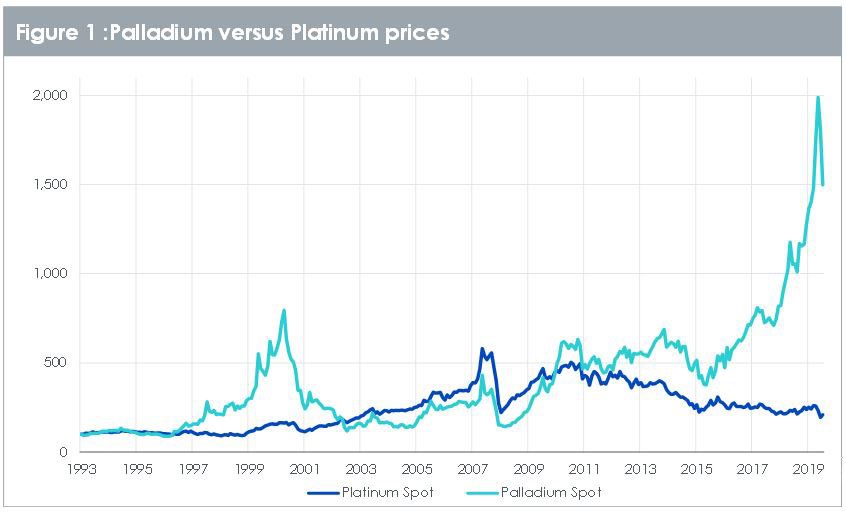

The recent price correction has driven the palladium to platinum ratio down from its peak of 3.1x to 2.4x. Despite palladium’s price premium to platinum it is less likely for platinum to be substituted for palladium in auto catalysts. The chief reason for this is platinum’s lower thermal durability which curtails its use in the widespread adoption of three-way catalysts.

The implementation of Real-Driving Emissions (RDE) testing involves stricter test cycles with faster driving speeds and higher engine temperatures which poses technical hurdles to platinum’s adoption in the three-way catalysts. At high operating temperatures experienced in a gasoline car, platinum particles may sinter, resulting in loss of surface area and hence of catalytic activity according to Johnson Matthey. Compared to palladium-rhodium formulations, the effectiveness of platinum-containing catalysts tends to deteriorate more rapidly as they age. While there might be some near-term potential for platinum to substitute some of the palladium used in diesel catalyst, we do not see a substitution effect in gasoline catalysts this year.

Platinum and palladium have witnessed a sharp downward price correction in 2020 owing to weak sentiment emanating from dwindling demand in the auto industry. Intermediate supply disruptions should aid a short-term price recovery for the green metals. The roll out of more stringent emissions standards globally are also likely to require higher content of platinum and palladium per unit of vehicle which should help offset the impact of weaker demand from the auto industry. Platinum’s supply is more concentrated in South Africa due to which platinum appears more exposed to supply disruptions versus palladium. In addition, palladium derives most of its use from the auto industry in comparison to platinum has a more diversified demand base. Platinum stands to benefit more than palladium owing to the prospect of having a more diversified demand base coupled with the exposure to higher supply risks.