Analys

Shale: Profits over volume. Saudi: IMO-2020 is coming

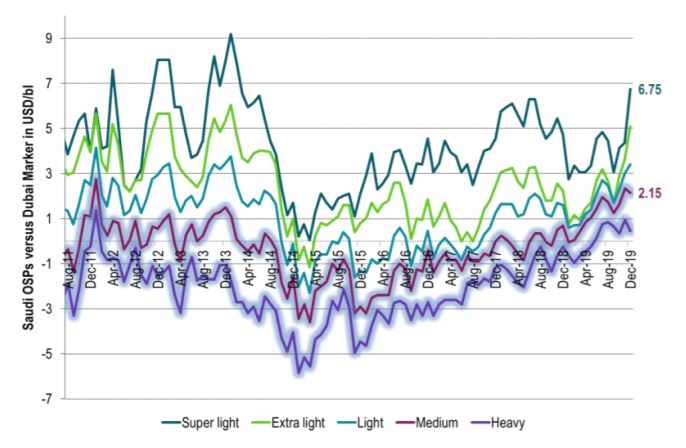

Saudi Arabia has lifted its Official Selling Price (OSP) for its Arab Super Light grade for December delivery to the highest premium versus the Dubai benchmark since early 2014. This is reflecting an increasing demand pressure towards light sweet grades in the run-up to the new low sulphur shipping fuel regulations (IMO-2020) taking effect January 1. Brent crude is one of the leading oil benchmarks in the world and it is light and sweet. Crude oil price rallies have historically typically been driven by tightness in light sweet grades as supplies of medium to heavy sour crudes normally has been quite plentiful. The strong rise in the Arab Super Light OSP is bullish for Brent crude.

The biggest shale oil producer in the Permian basin in the US, Occidental Petroleum, yesterday announced that it will cut its capital spending by close to 50% in 2020 vs. 2019 (FT article). In the Permian basin it will cut capex spending from $4.4bn in 2019 to $2.2bn in 2020. For almost a decade now shale oil investors have screamed ”volume, volume, volume”! They got a flood of oil, surplus market, low prices, no profits and just losses, losses, losses. They have been shooting themselves (or each other) in the foot. The mantra is now finally changing to profits over volume. US shale is now taking the same stand as OPEC: profit, not volume is what matters.

The shift from volume to profits in US shale oil has been going on since the start of the year with a continuous decline in the US shale oil drilling rig count as a reflection of this. The message from Occidental is that they will spend even less (50%) in 2020. So rig count will continue lower and well completions per month will probably also tick lower and US shale oil production growth will move from booming growth in 2018 to a likely trickle in 2020.

The Brent crude oil market has been tight since February this year. The continuous front-end backwardation has been a reflection of this. The whole Brent crude oil curve has however been severely depressed since June due to recession concerns/trade war/Brexit/inverted yield curves. Back-end contango in the Brent crude oil curve has been a reflection of this. The macro view for 2020 now seems to lighten a little with increasing hopes for some kind of US-China trade agreement and some improvements in PMI’s. If this continues then the prompt tightness in the crude oil market will start to matter more as the bears on the 2020 horizon retreats.

Ch1: Saudi Arabia OSPs versus the Dubai marker. The Arab Super Light premium is now at the highest level since early 2014. IMO is coming