Analys

Shale oil reaction function is changing and OPEC is happy

Brent crude had a strong week last week with four out of five closes at the highest level since late September. Recession fears eased (US 10yr moved from 1.71% to 1.94%) and optimism for a US-China trade deal improved. A 1.1% gain in the USD index was not able to hold Brent crude back from gaining 1.3% over the week with a close of $62.51/bl. Brent crude oil is selling off 1% this morning trading at $61.9/bl weighted down by the equity sell-off in Hong Kong / China

OPEC+ has signalled that its members are not overly eager to make deeper cuts at their upcoming meeting (5 December). This has given the oil price some temporary set-backs but it was not at all enough to hold back the oil price last week.

OPEC must be thrilled to see that US shale oil production is slowing and slowing and it is all happening at a Brent crude oil price of about $60-65/bl (WTI $57/bl ytd av). The fear has of course been that you would need to push the WTI price down below $45/bl in order to slow down US shale oil production growth. That was the last price inflection point back in May 2016 at which US shale oil activity accelerated again following the 2014/15 sell-off. The “shale oil reaction function” (activity as a function of the oil price) has clearly changed.

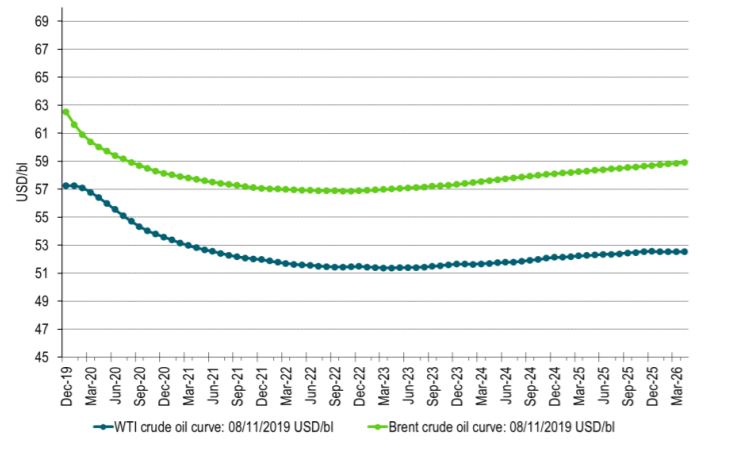

This change has not at all been incorporated into spot and forward prices yet. The longer dated WTI prices are typically between $50-53/bl from 2021 and all out to 2030. These prices are nominal. If we look at the forward WTI price for 2030 it is currently $52.3/bl in nominal terms. If we adjust for the US 10yr inflation swap of 1.92% this converts to a real forward price of $43.1/bl.

There is no doubt that the US has plenty of shale oil resources left. It is also clear that the US shale oil players have the technology to extract at a strong growth pace. This is also what OPEC has reflected in its latest World Oil Outlook where it projects US shale oil production to grow by another 5.3 m bl/d from 2019 to 2030.

The big question is of course at what price will this happen? Will it happen at a real forward WTI price of $45-50/bl? The current US shale oil slow-down basically says no. Market action so far this year is instead saying that at WTI $55/bl activity and production is slowing rapidly.

We have asked US shale oil players what they would do if the WTI price moved to $65-70/bl in 2020. The response was quite clear: Pay down debt, pay dividends and engage in share buy-backs if possible. So no expansion again even with a WTI price moving to $65-70/bl. This is in stark contrast to forward WTI prices currently saying that US shale oil will deliver strong volume growth at a real forward price of $45-50/bl. Yes, the US has lots of shale oil resources and it can deliver lots of growth but at what price? That’s the question. The current market assumption that this will happen year after year at a real oil price of $45-50/bl is in our view wrong. That is also what this year’s shale oil activity is showing.

Getting back again to Occidental Petroleum, the biggest US shale oil player in the Permian basin, and its recent announcement that it will slash capex spending in shale oil by 50% in 2020. What does this mean? The shale oil well completion rate in the US is now typically running at around 1400 wells/month. If this completion rate declines by only 10% then US shale oil production will experience zero growth.

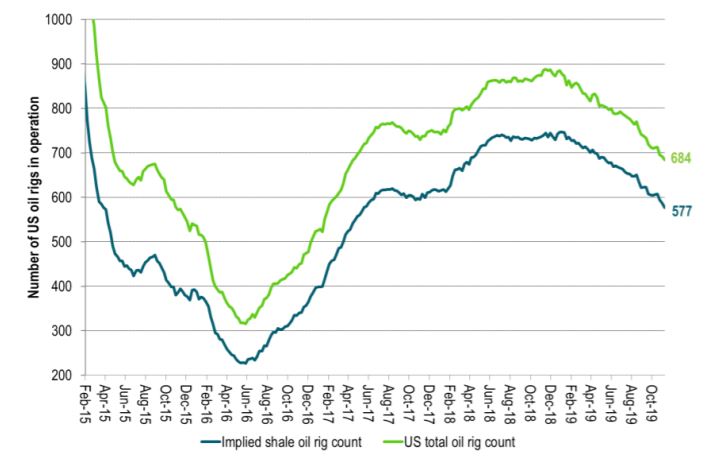

US shale oil players have been kicking out drilling rigs all of 2019. Last week 7 more oil rigs were kicked out. That’s a monthly decline rate of about 30 drilling rigs per month. The average decline rate so far this year is about 20 rigs per month. I.e. the rig decline is speeding up and the latest message from Occidental says that this is not at all the end of it with more rig declines to come.

So OPEC should be highly content. The market is punishing US shale oil players at WTI $55/bl and Brent at $60/bl. Puh, what a relief. You don’t need to go all the way down to $45/bl and below before US shale oil production growth tapers.

OPEC is totally happy with an oil price (Brent) of $60-65/bl and especially so because they see that at this price US shale oil activity is actually cooling down. We should see a very confident OPEC when they meet in December.

At some point in time here there is likely going to be a repricing of the longer dated WTI prices as the understanding sinks in that US shale oil production is not going to provide booming production growth for another 10 years at a real WTI price of $45-50/bl.

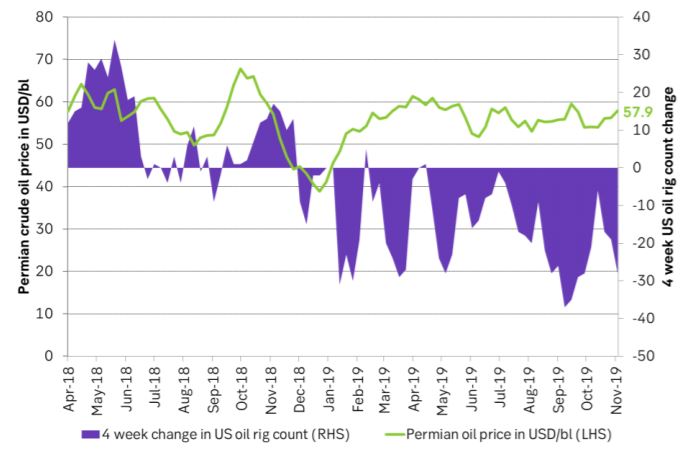

Ch1: Local US Permian crude oil price in USD/bl vs the 4 week change in US oil drilling rig count.

Ch2: US drilling rig count falling and falling

Ch3: Brent and WTI forward price curves. The Brent crude oil curve is in backwardation as a reflection of current crude oil tightness. Still midterm depression on concerns for 2020