Analys

SEB Metals Weekly: China Covid exit is bullish for metals

China Covid exit is bullish for metals

Softer inflation, slight macro-optimism, and China taking a rapid exit from Covid restrictions. Markets have become more optimistic. Inflation indices have eased and that has created some hopes that central banks won’t lift interest to a level that will kill the economy in 2023. Natural gas prices in Europe have fallen sharply. This has suddenly reduced energy-inflationary pressure and removed the direst downside economic risks for the region. But general market optimism is far from super-strong yet. The S&P 500 index has only gained 1.9% since our previous forecast on 1 Nov 2021, and oil prices are down nearly 10% in a reflection of concerns for global growth. China has however removed all Covid-restrictions almost overnight. It is now set to move out of its three years of Covid-19 isolation and lockdowns at record speed. Industrial metals are up 20% and the Hong Kong equity index is up 40% as a result (since 1 Nov-22). China’s sudden and rapid Covid-19 exit is plain and simply bullish for the Chinese economy to the point that mobility indices are already rebounding quickly. SEB’s general view is that inflation impulses will fade quickly. No need then for central banks across the world to kill the global economy with further extreme rate hikes. These developments have removed much of the downside price risks for metals in 2023 and we have to a large degree shifted our 2024 forecast to 2023.

Lower transparency, more geopolitics, more borders, and higher prices and exponential spikes. The first decade of this century was about emerging markets, the BRICs, the commodity price boom, the commodity investment boom, and free markets with free flow of commodities and labor with China and Russia hand in hand with western countries walking towards the future. High capex spending in the first decade led to plentiful supply and low prices for commodities from 2011 to 2020. A world of plenty, friends everywhere, free flow of everything, and no need to worry. The coming decade will likely be very different. Supply growth will struggle due to mediocre capex spending over the past 10 years. Prices will on average be significantly higher. There will be frequent exponential price spikes whenever demand hits supply barriers. Price transparency will be significantly reduced due to borders, taxes, sanctions, geopolitical alignments, and carbon intensities. Prices will be much less homogenous. Aluminium will no longer be just one price and one quality. Who made it, where was it made, where will it be consumed and what the carbon content will create a range of prices. Same for most other metals.

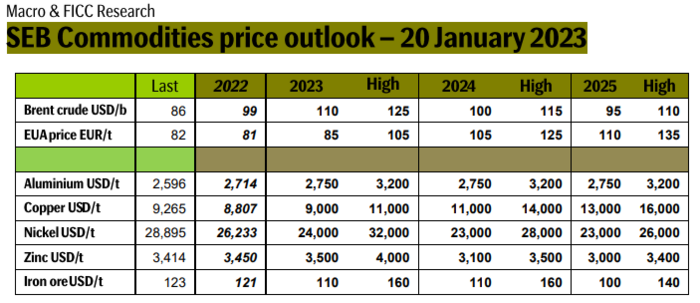

Copper: Struggling supply and China revival propel copper prices higher. Unrest in Peru is creating significant supply risks for copper as the country accounts for 10% of the global supply. Chile accounts for 27% of global production. Production there is disappointing with Codelco, the Chilean state-owned copper mining company, struggling to hit production targets. The Cobre Panama mine in Panama is at risk of being closed over a tax dispute between Quantum and the government. Cobre Panama is one of the biggest new mines globally over the past 10 years. The rapid exit from Covid restrictions in China is bullish for the Chinese economy and thus for copper demand and it has helped to propel prices higher along with the mentioned supply issues. The Chinese property market will continue to struggle, and it normally accounts for 20% of global copper demand while China accounted for 55% of global copper demand in 2021. While China is no longer prioritizing the housing market it is full speed ahead for solar, wind, EVs, and electrification in general. So, weakening Chinese copper demand from housing will likely be replaced by the new prioritized growth sectors. Global supply growth is likely going to be muted in the decade to come while demand growth will be somewhere between a normal 3% pa. to a strong 4% pa. to a very strong 5% pa. Copper prices will be high, and demand will hit the supply barrier repeatedly with exponential spikes as the world is working hard to accelerate the energy transition. Copper prices could easily spike to USD 15-16,000/ton nearest years.

Nickel: Tight high-quality nickel market but a surplus for a low-quality nickel. Nickel production is growing aggressively in Indonesia. The country is projected to account for 60-70% of global supply in 2030. This will become a huge and extremely concentrated geopolitical risk for the world’s consumers of nickel. Indonesia has an abundance of low-grade C2 nickel. The challenge is to convert low-quality C2 nickel to high-quality C1. We are set for a surplus of C2 nickel but the market for C1 nickel will depend strongly on the conversion capacity for C2 to C1. Low price transparency will also help to send prices flying between USD 20,000/ton and USD 30,000/ton. Strong growth in nickel production in Indonesia should initially call for prices down to USD 20,000/ton. But Indonesia is a price setter. It will account for 50% of global supply in 2023. It doesn’t make sense for Indonesia to kill the nickel price. If the nickel price drops, then Indonesia could quickly regulate supply. There should be a premium to nickel due to this. As a result, we expect the nickel price to average USD 24,000/ton in 2023. C2 to C1 conversion capacity may be strained and there should also be a monopoly premium due to the size of Indonesia. Converting C2 to C1 is however extremely carbon intensive and that could be an increasing issue in the years to come.

Zinc: Super-tight global market. European LME inventories are ZERO and zinc smelters there are still closed. European zinc smelters account for 16% of global zinc smelter capacity. Most of this was closed over the past year due to extremely high energy prices. European LME zinc stockpiles are now down to a stunning zero! The global zinc market is extremely tight. Reopening of European zinc smelting seems unlikely in H1-23 with a continued super-tight market as a result both in Europe and globally.

Aluminium: Price likely to be in the range of USD 2400 – 3200/ton and line with coal prices in China. Aluminium prices have historically been tightly tied to the price of coal. But coal prices have been all over the place since the start of 2021 with huge price differences between Amsterdam, Australia, and domestic Chinese coal prices which are now largely state-controlled. China banning imports of Australian coal, the Chinese energy crisis in 2021, and Russia’s invasion of Ukraine in 2022 are ingredients here. This sent aluminium prices flying high and low. Coal prices in China today imply a price of aluminium between USD 2400/ton and 3150/ton with the LME 3mth aluminium price nicely in between at USD 2590/ton. The global coal market should now become more orderly as China now again is accepting Australian coal. Energy costs have fallen sharply in Europe and some producers in the Netherlands have talked about possible restarts of production. China is likely to reduce its exports of primary aluminium. Energy security of supply is high on the agenda in China, and it makes no sense to emit lots of CO2 in China and indirectly export energy in the form of primary aluminium. Growth in non-China aluminium demand in the years to come will have to be covered by non-China producers which have the potential to force prices higher and away from coal as the price driver. While LME has one price for the 3mth aluminium price we’ll likely get larger and larger price differences across the world in the form of possibly extreme price premiums for example in the EU and the US.