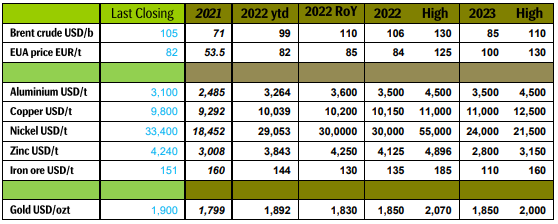

Analys

SEB Commodities price outlook

Macro: Hot US, cold China, expensive energy, and a looming food crisis. The US economy is super-hot like it is running on steroids following trillions of USD in stimulus during the pandemic. Naturally strong demand for everything. It is in urgent need for cool-down and the US Fed is on the case. It will not let a possible recession down the road stand in its way of killing off the current wild US inflation. The US Fed will now force the US economy to cool down, potentially to the point of recession. The temperature in Chinese economy on the other hand is close to zero due to Covid lock-downs.

The Chinese government is in what looks like a futile and losing battle versus the virulent Omicron virus. Lock-downs, lock-downs, lock-downs of large cities are the government’s response as the virus pops up in more and more places. Omicron infections are now present in regions constituting 75% of China’s GDP. It is difficult to see how China can escape the current vicious lock-downs without letting the virus free. Once China is on the other side of the Omicron virus the government will likely stimulate the economy significantly to counter the pain and weakness created from the ongoing lock-downs. But first it needs to move through the Omicron problem by letting it loose as it most likely cannot bypass it like previous, and less virulent virus variants.

In the middle of all this we have the war in Ukraine which has contributed to much higher energy prices and especially so in Europe where power and natural gas prices now are 5 times higher than normal. Ukraine is usually a large exporter of fertilizers as well as the 5th biggest grain exporter in the world. Its grain production could be down by 50% this year. Russia is the world’s biggest grain exporter and current sanctions are likely to hamper its production. Kansas, the biggest wheat producer in the US is experiencing severe drought. Bloomberg’s agri index is already at an all-time-high in nominal terms though it is still 18% below its previous real term high from 2011. The global food crisis from 2010 to 2013 let to riots, hording, export curbs and presumably set off the tragic ‘Arab spring’ which led to a lot of tragic bloodshed.

So, in total we have a situation where:

- The US economy is super-hot but set to cool down as fast as the US Fed possibly can cool it

- The Chinese economy will likely be chilled as long as the Chinese government tries to fight Omicron with lock-downs

- The EU economy will struggle under the burden of 5x normal power and nat gas prices due to the Russian invasion of Ukraine

- A looming food crisis could possibly destabilize lower income countries

The current macro situation is very challenging and global growth has been revised considerably lower by the IMF. Over the past 6 months it has adjusted its 2022 growth expectations from almost 5% to now just above 3.5% (April update). Since then, things have probably gotten worse. Many commodities are however still in short supply. 1) Due to capex cuts over the past two years as producers went into protective mode amid the first pandemic since 1918. 2) Due to muted commodity capex spending over the past decade as profits were low and investors looked in other directions. We thus maintain a robust outlook for commodity prices. There are clearly downside risks due to the current macro environment but there are also significant supply risks.

This report has been compiled by SEB´s Commodity Research, a division within Skandinaviska Enskilda Banken AB (publ) (”SEB”), to provide background information only.