Analys

Repeated losses of supply in Libya in 2020 seems likely

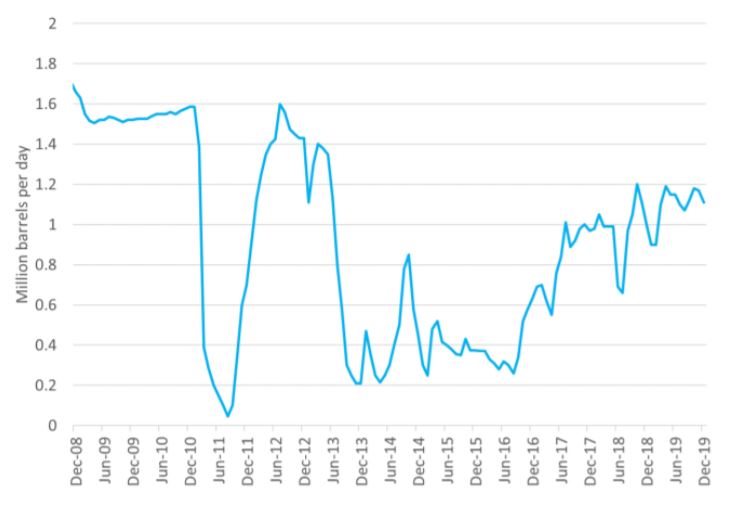

Libya’s oil production (1.1 m bl/d in December) is now estimated to have fallen to close to zero as General Haftar has closed ports and pipelines under his control. So far there are no damages to oil installations and production can thus ramp up just as quickly if/when a decision by Hafter is taken to revive it. The big question is how much oil will be lost for how long. The market most clearly expects this to be very short term. That is why the oil price is not moving up more than 0.4% to $65.1/bl at the time of writing.

General Haftar is in control of the eastern part of Libya and is supported by UAE, Egypt, Russia and France who have supported him with both arms and mercenaries. His goal has all along been to overtake all of Libya. He has pushed hard to conquer Tripoli where the internationally recognized government (backed by the U.N., Turkey and Qatar) is seated. He has been besieging the city now for close to a year without success.

General Haftar refused to sign a ceasefire agreement in Moscow one week ago and has now halted the flow of oil out of Libya in response to the ongoing peace negotiations. We don’t think that he will let go of his power grab ambitions in Libya. We don’t think that Russia will stop supplying him arms and funding. In our view it does not look like the ongoing peace negotiations will be successful. The result will then be further increased military and financial support of the two sides in the conflict with periods of lost supply from Libya a highly likely outcome in the year to come.

It is the National Oil Company (NOC) in Libya, seated in Tripoli, which is handling Libya’s crude oil sales. Libya’s NOC is the internationally recognized body to execute such sales. Haftar has earlier tried to circumvent the NOC but without any success.

It is the Central Bank in Tripoli which handles the income from the oil sales and then distribute it impolitically in Libya both to the east and the west. The halt in Libya’s oil exports is thus halting the financial funding of both General Haftar to in the eastern part of Libya as well as the western part. So, unless Haftar is getting more financial funding from Russia (and Egypt, UAE and France) he will have to revive oil exports again in order to fund himself.

The expert view is that Haftar does not have neither the financial nor the military power to overtake Tripoli (and thus the whole of Libya) and if he did overtake Libya it will likely end in bloodbath and chaos. The only real solution is a diplomatic solution.

The ongoing peace negotiations is an international diplomatic effort to halt the flow of money, arms and soldiers from the international backers of the two sides which is the main driver of the current escalation.

Turkey’s president Erdogan (supporting Tripoli and western Libya) stated last Thursday that he would send troops to Tripoli in order to support the internationally recognized government there until stability has been achieved. General Haftar’s shut-down of Libya’s oil exports this weekend was probably partially a response to this move by Turkey’s Erdogan.

All through 2019 the market experienced a string of serious events in the Persian Gulf and the Middle East with the most serious being the attack on Saudi Arabia’s oil installations (Khurais field and Abqaiq processing facility) in mid-September last year.

The reason why these events did not have more than a fleeting impact on the oil price last year was of course because not much oil was really lost in these events (except Venezuela and Iran). Even the severe attack on Saudi Arabia did not lead to much losses of supply in the market since Saudi could sell oil and products from substantial inventories.

Now we have a real outage. Expected to be short-lived for now. But to us it does not look like diplomacy will be easily achieved. Thus, periods of significant losses of supply in Libya seems likely in the year to come. This will lend support to oil prices which to start with are under pressure from strong non-OPEC production growth, high inventories and lukewarm oil demand growth.

Ch1: Libya’s crude oil production. Lately at 1.1 m bl/d in December. Now probably close to zero

Ch2: Iraqi oil production. If the market was to lose this supply for an extended period, then the price impact would be significant