Analys

A remarkable rebound after an early summer lull

![]()

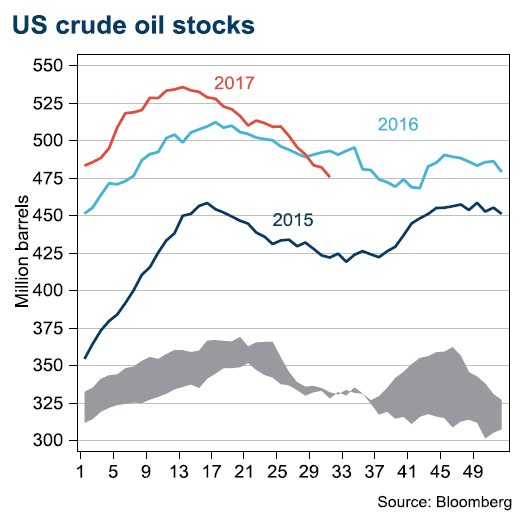

Oil stuck in loop

The price of crude oil has not been this uneventful in a long time. Over the past 12 months, the oil price has traded within a tight range, spanning just USD 13/bbl. However, in terms of short-term swings, the summer recovery has been relatively strong, up 15% since the low point in June.

The summer driving season in the US has been surprisingly strong given weaker consumption data during the spring. Consumables used to be a good leading indicator for fuel demand during summer. Yet, this year’s driving season has drawn on stocks, which are now lower than in 2016. However, that does not lead us to change our view of the oil price (USD 40/bbl at the end of 2017), as US oil production continues to increase and driving season demand is of course seasonal.

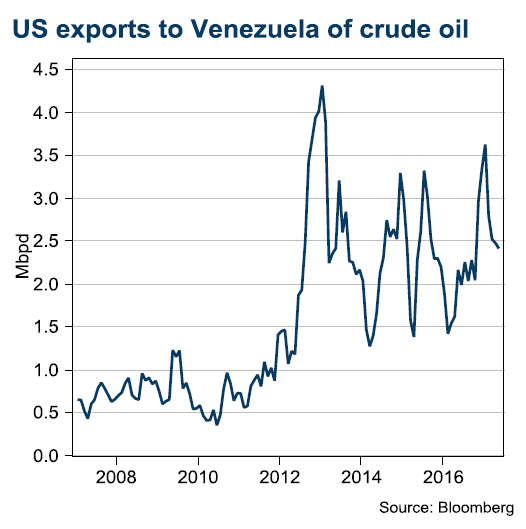

Venezuela has been the most relevant risk premium for commodity markets during summer. None of the remaining OPEC members are able to compensate for a full-scale breakdown of the Venezuelan oil tap.

The heavy crude nature of Venezuela’s oil presents a suitable weak point for the Trump administration to exploit. Venezuela needs to import light crude oil to blend with its domestic production to create a saleable product. Hence, there are two main risks for oil prices in Venezuela, with the first being full-scale export sanctions from the US (in our view, imports elsewhere will come at a higher cost, but this problem could be solved). There is plenty of available light crude oil in Western Africa after the US lowered imports in the wake of the shale revolution. The second risk is a default in Venezuela. In such a scenario, we struggle to see oil workers continuing to work if salaries are frozen.

On the other hand, OPEC faces new challenges. Ecuador was the first member to leave the production accord officially and start to increase production and exports to meet its fiscal needs. Iraq followed shortly after, but now regrets this decision after an OPEC summit focusing on fading compliance within the group.

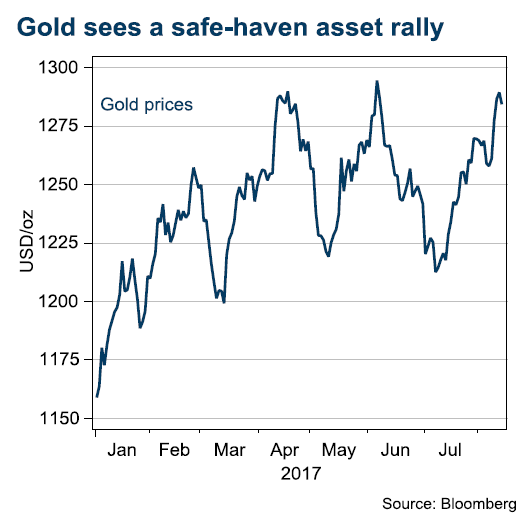

North Korea boosts bullion demand

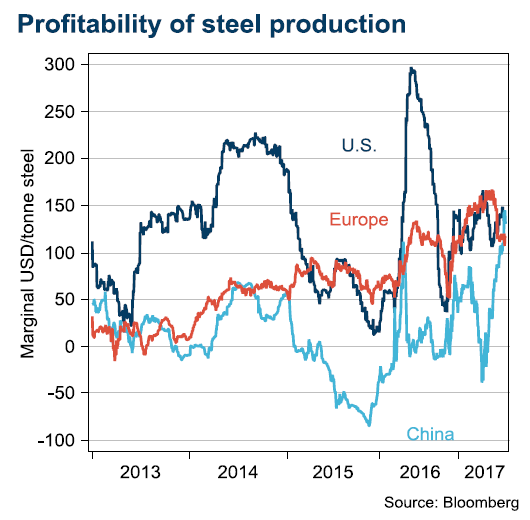

China forces cutbacks

Beijing has escalated the cutback campaign of unprofitable commodity production. Coal mining is now halfway to the 2020 target. Other bulk commodities are affected as well, particularly iron ore, which had the greatest price gain of all commodities during the summer, up 40% since June compared to coal’s 20%.

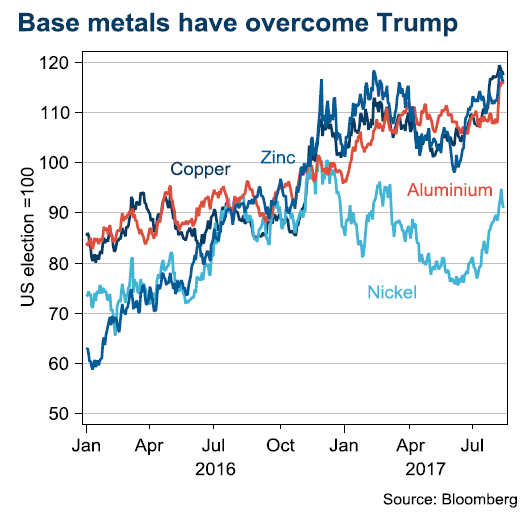

Base metals on solid ground

Of the summer gains, we believe base metals stand on the safest ground. However, aluminium has gained from announced cutbacks in China. Yet, in our view, that trend is vaguer than those for steel, iron ore and coal.

Research disclaimer

Risk warning

All investments involve risks and investors are encouraged to make their own decision as to the appropriateness of an investment in any securities referred to in this report, based on their specific investment objectives, financial status and risk tolerance. The historical return of a financial instrument is not a guarantee of future return. The value of financial instruments can rise or fall, and it is not certain that you will get back all the capital you have invested.

Research disclaimers

Handelsbanken Capital Markets, a division of Svenska Handelsbanken AB (publ) (collectively referred to herein as ‘SHB’), is responsible for the preparation of research reports. SHB is regulated in Sweden by the Swedish Financial Supervisory Authority, in Norway by the Financial Supervisory Authority of Norway, in Finland by the Financial Supervisory Authority and in Denmark by the Danish Financial Supervisory Authority. All research reports are prepared from trade and statistical services and other information that SHB considers to be reliable. SHB has not independently verified such information and does not represent that such information is true, accurate or complete. Accordingly, to the extent permitted by law, neither SHB, nor any of its directors, officers or employees, nor any other person, accept any liability whatsoever for any loss, however it arises, from any use of such research reports or its contents or otherwise arising in connection therewith.

In no event will SHB or any of its affiliates, their officers, directors or employees be liable to any person for any direct, indirect, special or consequential damages arising out of any use of the information contained in the research reports, including without limitation any lost profits even if SHB is expressly advised of the possibility or likelihood of such damages.

The views contained in SHB research reports are the opinions of employees of SHB and its affiliates and accurately reflect the personal views of the respective analysts at this date and are subject to change. There can be no assurance that future events will be consistent with any such opinions. Each analyst identified in this research report also certifies that the opinions expressed herein and attributed to such analyst accurately reflect his or her individual views about the companies or securities discussed in the research report.

Research reports are prepared by SHB for information purposes only. The information in the research reports does not constitute a personal recommendation or personalised investment advice and such reports or opinions should not be the basis for making investment or strategic decisions. This document does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any securities nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Past performance may not be repeated and should not be seen as an indication of future performance. The value of investments and the income from them may go down as well as up and investors may forfeit all principal originally invested. Investors are not guaranteed to make profits on investments and may lose money. Exchange rates may cause the value of overseas investments and the income arising from them to rise or fall. This research product will be updated on a regular basis.

No part of SHB research reports may be reproduced or distributed to any other person without the prior written consent of SHB. The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions.

The report does not cover any legal or tax-related aspects pertaining to any of the issuer’s planned or existing debt issuances.