Analys

Orange juice: Declining supply meets weak demand

![]()

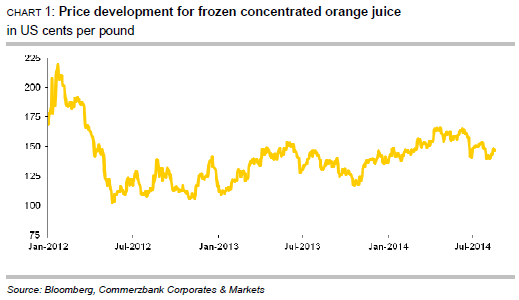

Prices for frozen concentrated orange juice on the New York exchange have not been able to sustain their month-long uptrend that was intact until June. Instead, they dropped by more than 15% between the middle of June and the first days of August. Only at the current margin could the quotations regain some ground, rising from 139 US cents to nearly 150 US cents per pound. Though the two-year high of mid-June at 167 US cents per pound is still some ways away (chart 1).

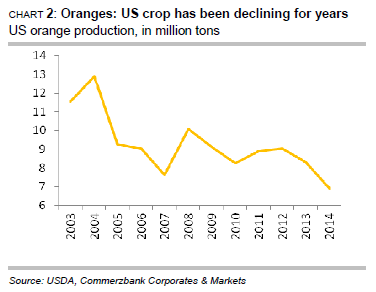

The focus was therefore very much on the supply side. The month-long price rise until June had been triggered by prospects of a lower US supply. In fact, the last harvest in the US was already unsatisfactory. In its July report the USDA once more reduced its estimate for the 2013/14 US harvest compared to its last forecast from January. It now envisages only 6.3 million tons of oranges, 16% less than in 2012/13 (chart 2). This is the second large consecutive decline. The plant disease citrus greening, which causes the fruit to drop prematurely, still maintains its grip on large parts of the growing regions. As a result of the lower harvest, US orange juice production should come in at 481,000 tons, 20% below 2012/13 levels, which were already lower than in the previous year.

Unlike global orange production itself, where growth not only in Brazil but also in China will probably more than offset the decline in the US, global orange juice production should stagnate in 2013/14 in the best case according to the USDA. Juice production had already declined in the two preceding years.

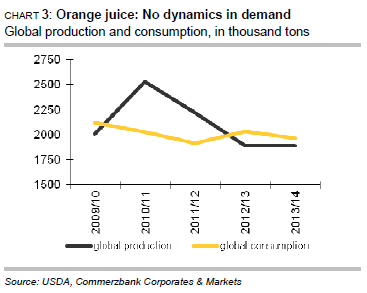

However, not only juice production but also the consumption of orange juice is lacking momentum. Global consumption has for years been fluctuating around the mark of 2 million tons (chart 3). Consumption is clearly declining in the US – the most important market alongside the EU. US per-capita consumption of orange juice has reportedly fallen from 46 litres ten years ago to only 35 litres in 2013. According to latest data, US retailers sold 9% less orange juice than one year before in the four weeks ending on 2 August 2014. A wide range of other juices and new developments in other beverages are now competing with orange juice. Also, many consumers prefer beverages with lower sugar content or lower prices. In other developed countries, too, the market for orange juice should be largely saturated. Double-digit growth rates in some other countries, such as China, for instance, cannot reverse this outlook, given the low absolute figures.

It remains to be seen whether in the present situation of weak demand the continuing decline in supply can contribute to noticeable price rises on a lasting basis. We only expect this to happen if supply shortfalls attributable to storms or diseases turn out even larger than currently expected. Fears of a marked hurricane season have driven up prices often already. This year has been relatively calm so far, but the hurricane season only ends in November. Hence, stormrelated crop losses in Florida are still a possibility.