Analys

OPEC+ tightens the front. Producers lean on the back

Investors and producers however fear a tsunami of additional US shale oil supply in late 2019 and 2020 as new pipelines are installed from the Permian to the US Gulf.

Bjarne Schieldrop, Chief analyst commodities

As a consequence Brent crude oil prices are likely to be supported at the front by OPEC+ while investors and producers will be active sellers of oil for late 2019 and 2020. This will likely push the Brent crude curve into proper backwardation again with the front a little higher but with bearish pressure on the medium term contracts. Backwardation will attract more speculators, again adding upwards push in the front.

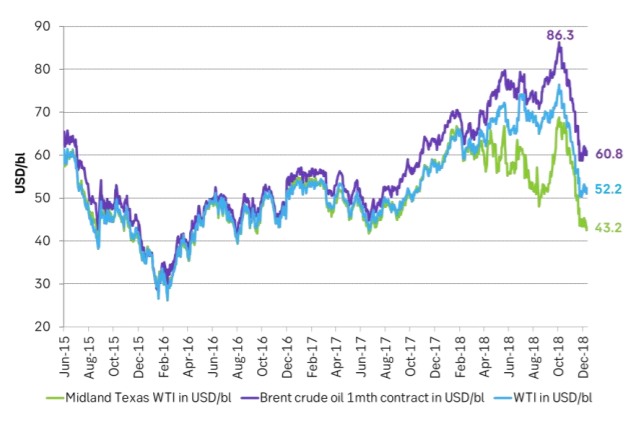

US shale production continues to grow in the Permian basin, but pipeline capacity is full and new pipelines will not be there until late 2019. As such we expect the local Permian crude price to sink yet lower in order to tame production growth and match it to current installed pipeline capacity. Local Permian crude is already down at $43/bl.

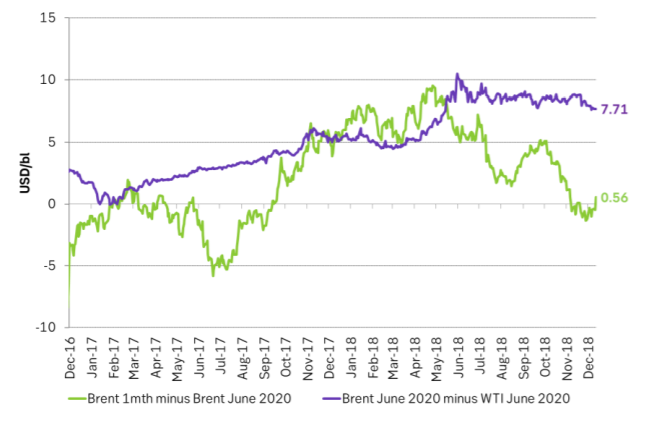

As a consequence the Brent crude to WTI Cushing and to local Permian crude price spreads should continue to widen for a while yet. These spreads could however be pushed tighter for late 2019 and 2020 durations. This will add to the picture above: Support for front end Brent but weakness for medium term 2020/2021 Brent prices.

Conclusion:

- Stay long front month Brent versus short June 2020 Brent crude.

- Stay short the Brent versus long WTI for June 2020

It is important to remember that the sharp decline in oil prices during October and November to a very large degree was driven by a strong increase in production by OPEC/OPEC+. Partially as a tactically lead-up to the recent OPEC+ meeting. As such we believe they are fully capable of tightening up the front end of the oil market again as well. Saudi Arabia produced 11.1 m bl/d in November and delivered an additional 0.2 m bl/d from inventory. In January they’ll produce 10.2 m bl/d. That’s a strong physical tightening. Yes production was (and still is) also growing strongly in the US, but that was really not a surprise at all. The following is the likely mix sinking the oil price dramatically since early October:

- Softer global growth outlook (and thus softer oil demand growth outlook for 2019)

- A sharp sell-off in the S&P 500 index

- A strong rise in production by OPEC+

- Unexpected US Iran-waivers which enabled continued significant volumes of exports from Iran.

- A huge exodus of net long speculative positions in Brent crude and WTI crude

Of course booming US shale oil production was an important factor, but it was not a surprise this autumn. Strong US shale oil production growth has not been a problem over the past two years because: 1) Global oil demand has been strong adding 3 m bl/d in two years and 2) Losses in other supply of more than 2 m bl/d in two years has made additional room for growing US production. Strongly growing US shale oil production became a problem this autumn because demand growth was expected to slow with slower global economic growth while further steep losses from Iran were avoided due to allowance for waivers.

Brent is jumping 1.9% today to $61.4/bl as API expects US crude stocks to show a 10.2 m bl/d draw in today’s numbers at 16:30 CET. Lost supply in Libya this week also adds to the bullish sentiment.

Ch1: Market has moved from a situation where the oil price needed to slow down global demand to balance the market with global benchmark Brent crude at $86.3/bl in early October to instead a market state where the oil price needs to do the job of slowing down US shale oil production growth. I.e. the local US crude benchmarks have moved to low $40-50/bl.

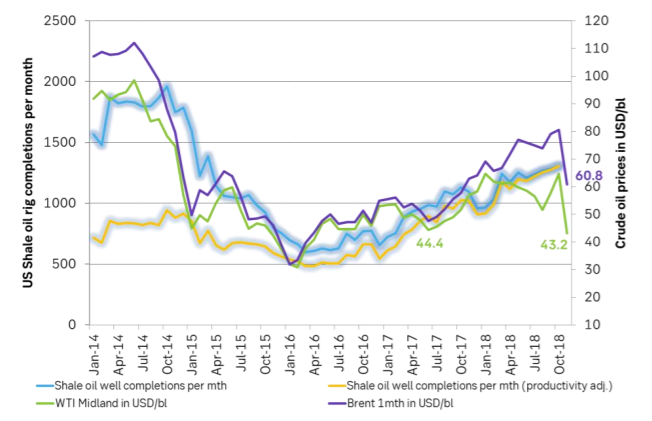

Ch2: US shale oil well completions per month is what matters for US shale oil supply growth. The local Permian crude oil price is now working hard to slow down well completions per month in order to balance local Permian supply to pipeline capacity

Ch3: OPEC+ will tighten up the front Brent market while producers will sell 2020 Brent contracts fearing a wave of additional US shale oil supply in 2020 as new pipelines from Permian to US Gulf comes online. June 2020 Brent – JuneWTI 2020 likely erode going forward in expectation that oil flows to the US Gulf will be uncloged with new pipelines. Green graph to move higher. Lilac to move lower