Analys

OPEC+ removes the downside price risk

While they may disagree on what is the right price to aim for they are all in agreement that they do not want global oil inventories to rising back up again.

Specific strategy and cuts will be communicated later this week when OPEC meets in Vienna on 6 December.

Bjarne Schieldrop, Chief analyst commodities

The key take away from all of this is that global oil inventories will not rise back up, the Brent crude oil price curve will not bend deeper and deeper into contango and the front month Brent crude oil will not dive yet lower to USD 55, 50, 45,…/bl.

Exactly in what price range above USD 60/bl we’ll end up depends on the final decision, strategy and communication from OPEC+ at the end of this week.

Canada, Alberta’s Premier Rachel Notley decided this weekend to cut Alberta’s oil production by 325 k bl/d from January onwards until local inventories are back down to normal. Alberta is the largest oil producer in Canada and the cut constitutes a reduction of 8.7% in Alberta. After that the production cuts will be reduced to 95 k bl/d until the end of 2019. Together with the agreement between Russia and Saudi Arabia this weekend this adds to the forward fundamental price support picture.

OPEC’s Advisory Committee last week estimated that OPEC needs to cut production by 1.3 m bl/d versus its October level of 33 m bl/d in order to balance the market next year. I.e. it estimated a call-on-OPEC for 2019 of 31.7 m bl/d. In comparison the IEA in November estimated a call-on-OPEC for 2019 of 31.3 m bl/d. OPEC has produced 32.2 m bl/d on average ytd.

A contracting call-on-OPEC is of course unsustainable over time. As such the estimated decline in call-on-OPEC in 2019 is fundamentally problematic. Internal dynamics within OPEC will however decide how problematic this is. For 2019 we expect production in Venezuela to decline further from an average of 1.4 m bl/d this year to only 1.0 m bl/d in 2019. In addition we expect Iran’s production to be roughly 0.4 m bl/d lower on average in 2019 than in 2018. So here already we have internal OPEC declines of some 0.8 m bl/d y/y to 2019 which reduces the needs for cuts by the other members. So with help also from Russia and the other 9 cooperating countries the magnitude of needed active cuts by those who have to cut will not amount to all that much. The amount of needed cuts by the active cutters within OPEC+ can of course change rapidly due to very unpredictable production in Libya, Nigeria and Angola just to mention a few.

Russia has been very reluctant to join in on further cuts and has stoically announced that it is fine with almost any oil price next year. In our view Russia seems to be concerned over the very strong US crude oil production growth. As such its position as we read it is twofold: 1) It does not want to see global inventories rising back up again and 2) It wants an oil price at a level which tempers US shale oil production growth. The challenge for Russia thus seems to be how to cut production without driving up the oil price too much.

The Brent crude oil price has rebounded close to 4% this morning to USD 61.7/bl but seems to have halted there waiting for the details and specifics to materialize. The Joint Ministerial Monitoring Committee which works on behalf of OPEC+ will meet in Vienna on 5 December and discuss needed action. Its recommendation will be the foundation for the OPEC ministerial meeting and the full meeting of OPEC+ the following day.

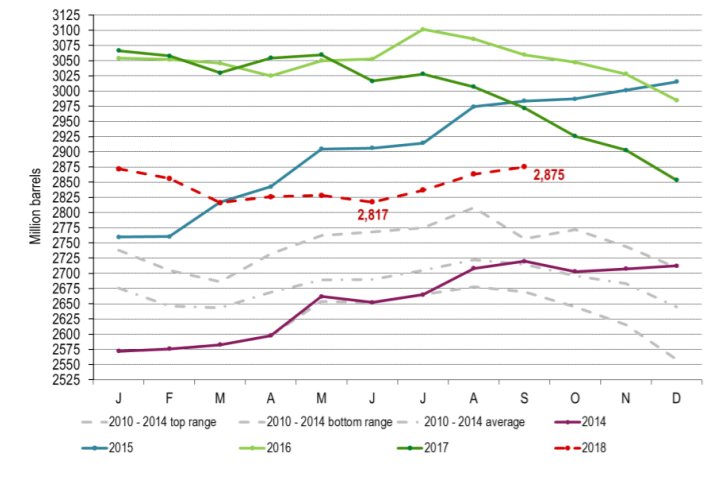

Ch1: OECD commercial inventories have increased 58 m bl from June to September. Inventories normally increase 25 m bl this period of year. Thus adjusting for seasonality the inventories rose only 33 m bl over these three months

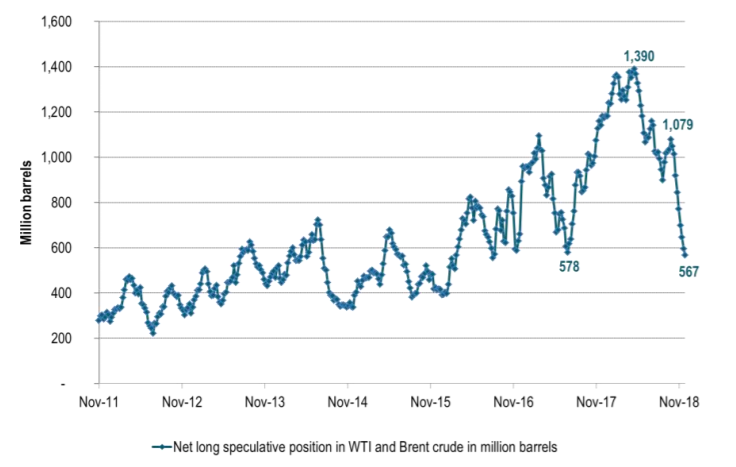

Ch2: Net long speculative positions in million barrels for Brent + WTI down to the previous lows since start of 2016

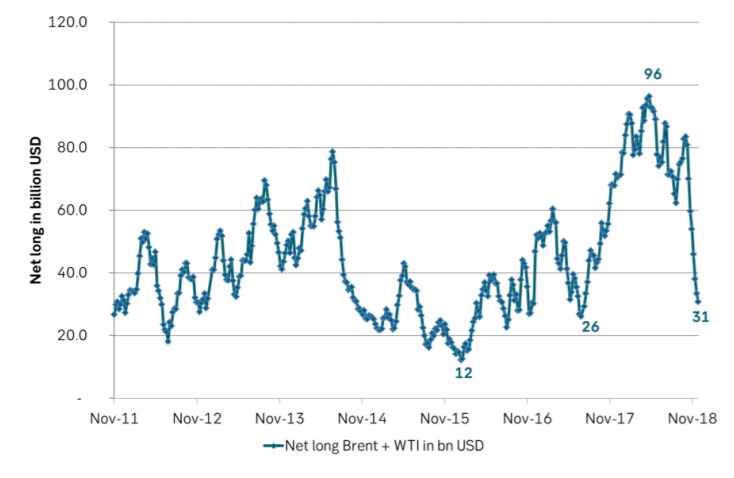

Ch3: Net long speculative positions in billion USD for Brent + WTI close to the low of mid-2017. Crude prices were even lower in mid-2017 and of course crude prices were much higher in 2011, 2012, 2013 and partially also 2014

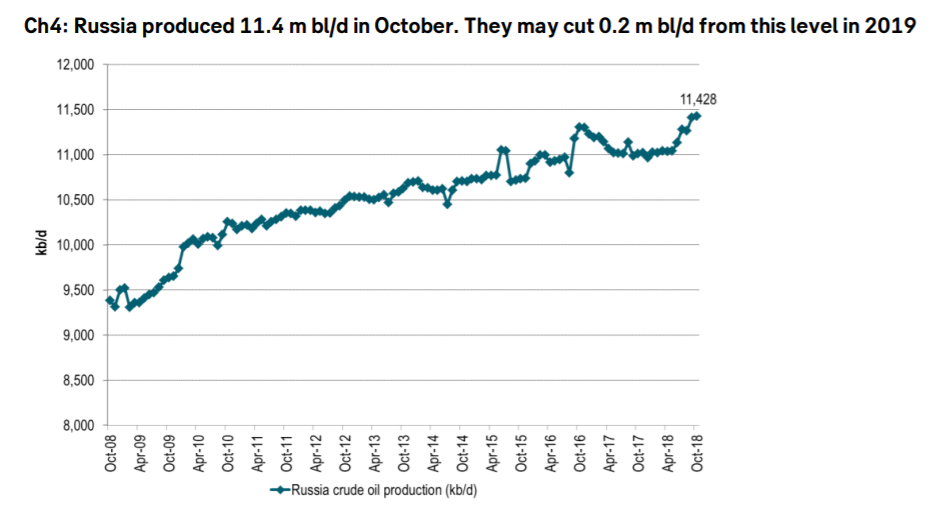

Ch4: Russia produced 11.4 m bl/d in October. They may cut 0.2 m bl/d from this level in 2019

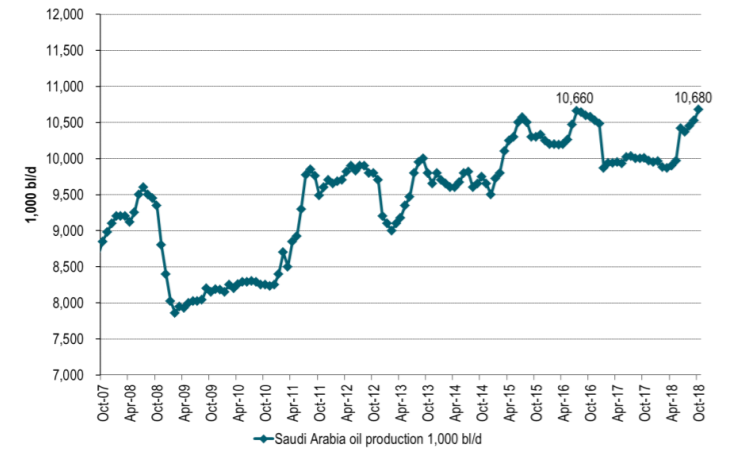

Ch5: Saudi Arabia produced 10.7 m bl/d and can easily cut production by 0.2 to 0.4 m bl/d in 2019

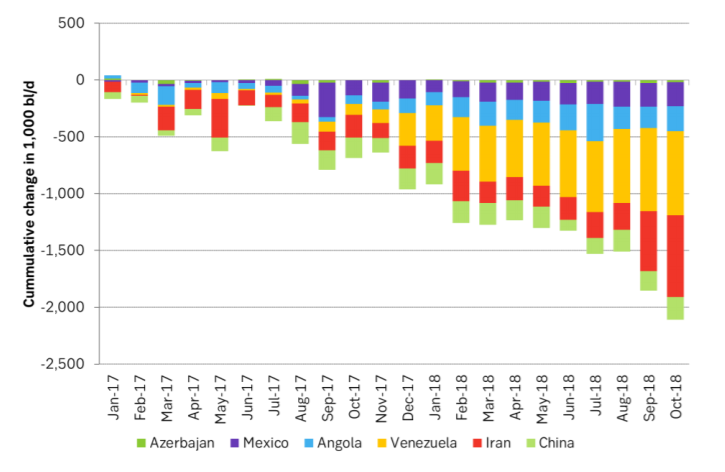

Ch6: Production losses from selected countries have led to losses of more than 2 m bl/d since early 2017. We expect further losses also in 2019. How much will of course strongly impact the supply/demand balance in the oil market and thus the need for active production cuts by OPEC+ or those who can cut in OPEC+. As Aleksander Novak said: ”we don’t know yet if there will be a surplus in 2019 or not”. Putin’s statement this weekend “…we will monitor the market and react to it quickly” is thus a natural continuation of this.