Analys

OPEC and non-OPEC tighten their belts

![]()

One man show: Al Falih

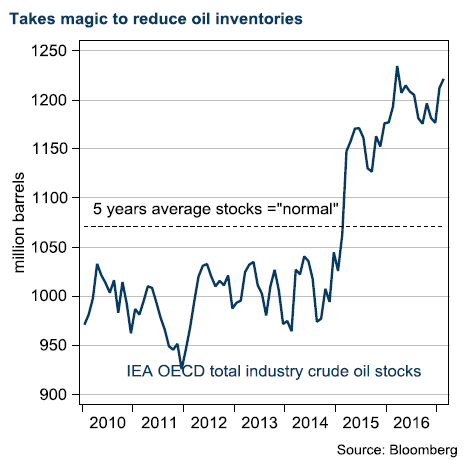

Mountain out of a molehill

“Too much talk, too little cutting production” is the reaction after the first round agreement on cutbacks. OPEC has failed to clear the market glut. However, we believe the curbs and conversations are working toward bulging the coffers of oil producing nations.

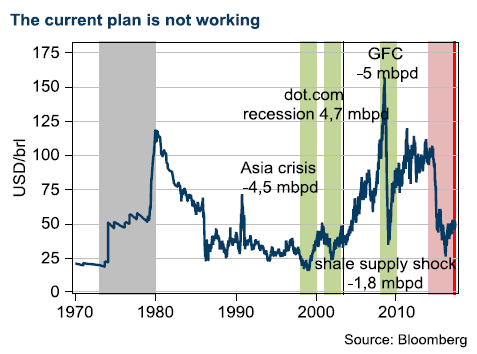

The size of the cut is only a fraction of the well planned/timed cutbacks of the Asian crisis in 1998, the dot com recession in 2001, and the global financial crisis in 2008. This time, weak oil prices stem from growing supply, rather than weaker demand, leaving the cartel toothless. If OPEC genuinely wants to drive oil prices, we believe it needs to make a deeper cut. At this stage, it appears it is not prepared to bare the cost.

In our view, shale oil is growing too fast and any OPEC change must be well balanced to further avoid accelerating growth in US crude oil production.

Same conditions

Weak outlook

In our view, a rollover without a promise of further extension does not correspond to the “whatever it takes” assertion from Al-Falih. If the deal unravels, we believe the cut of more than 1.2 million bbl/d will flood back into market, causing prices to crash, again. The nine-month extension should help to bring about a modest deficit in the oil market, supporting a floor prices. We estimate USD 50 as a reasonable price during that time. However, ultimately, we believe the market will start to test OPEC’s endurance. In our view, prices will start drifting toward USD 40 once more, if the stock overhang persists.

Research disclaimer

Risk warning

All investments involve risks and investors are encouraged to make their own decision as to the appropriateness of an investment in any securities referred to in this report, based on their specific investment objectives, financial status and risk tolerance. The historical return of a financial instrument is not a guarantee of future return. The value of financial instruments can rise or fall, and it is not certain that you will get back all the capital you have invested.

Research disclaimers

Handelsbanken Capital Markets, a division of Svenska Handelsbanken AB (publ) (collectively referred to herein as ‘SHB’), is responsible for the preparation of research reports. SHB is regulated in Sweden by the Swedish Financial Supervisory Authority, in Norway by the Financial Supervisory Authority of Norway, in Finland by the Financial Supervisory Authority and in Denmark by the Danish Financial Supervisory Authority. All research reports are prepared from trade and statistical services and other information that SHB considers to be reliable. SHB has not independently verified such information and does not represent that such information is true, accurate or complete. Accordingly, to the extent permitted by law, neither SHB, nor any of its directors, officers or employees, nor any other person, accept any liability whatsoever for any loss, however it arises, from any use of such research reports or its contents or otherwise arising in connection therewith.

In no event will SHB or any of its affiliates, their officers, directors or employees be liable to any person for any direct, indirect, special or consequential damages arising out of any use of the information contained in the research reports, including without limitation any lost profits even if SHB is expressly advised of the possibility or likelihood of such damages.

The views contained in SHB research reports are the opinions of employees of SHB and its affiliates and accurately reflect the personal views of the respective analysts at this date and are subject to change. There can be no assurance that future events will be consistent with any such opinions. Each analyst identified in this research report also certifies that the opinions expressed herein and attributed to such analyst accurately reflect his or her individual views about the companies or securities discussed in the research report.

Research reports are prepared by SHB for information purposes only. The information in the research reports does not constitute a personal recommendation or personalised investment advice and such reports or opinions should not be the basis for making investment or strategic decisions. This document does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any securities nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Past performance may not be repeated and should not be seen as an indication of future performance. The value of investments and the income from them may go down as well as up and investors may forfeit all principal originally invested. Investors are not guaranteed to make profits on investments and may lose money. Exchange rates may cause the value of overseas investments and the income arising from them to rise or fall. This research product will be updated on a regular basis.

No part of SHB research reports may be reproduced or distributed to any other person without the prior written consent of SHB. The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions.

The report does not cover any legal or tax-related aspects pertaining to any of the issuer’s planned or existing debt issuances.