Analys

OPEC meeting: Holding back is easy as Iran and Venezuela takes all the pain

Brent crude jumps 2.8% this morning to $66.6/bl following news that Saudi Arabia and Russia are in agreement of an extension of current cuts for another 6 to 9 months and that this plan is also endorsed by Iran’s oil minister Zanganeh. A trade truce between US and China also adds strength to the oil price this morning.

OPEC being “between a rock and a hard place” has been the description of OPEC’s situation in the run-up to this OPEC meeting. Losing market share to booming US shale oil production on the one hand while facing weakening oil demand growth along with slowing global growth on the other hand. It is true that OPEC as a whole is losing market share. But this burden is not evenly distributed as it is Venezuela and Iran who are taking almost all the pain. The other OPEC members (and OPEC+ members) are basically not taking any heat at all.

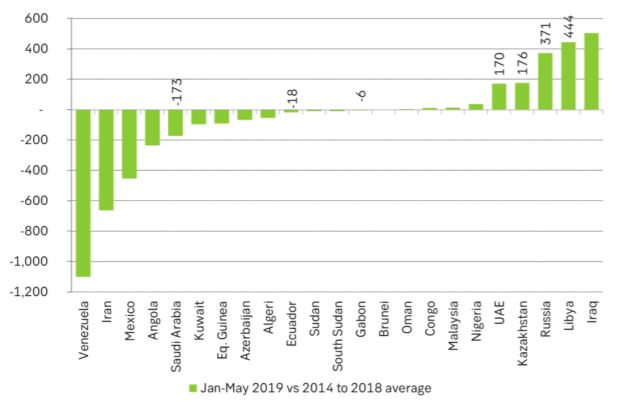

From Jan to May Saudi Arabia produced only 173 k bl/d below its 2014-2018 average while Russia produced 371 k bl/d above that average.

It is thus easy for the main producers to decide to roll cuts forward as they do not really cost them anything, or very little to do so. The only price they have to pay is to hold back supply slightly and refrain from growing their production along with global oil demand growth while harvesting an oil price of $60-70/bl.

It will of course be problematic when Iran and Venezuela eventually returns to the market. And that could indeed be a very bearish moment in the oil market. Given the large range of uncertainties in the oil market OPEC has learned to act reactively rather than trying to act pre-emptively. Thus OPEC will have to deal with the return of Venezuela and Iran at some point in the future but then it will deal with that rainy day when it comes. Right now things are as they are and it is easy for OPEC’s key members and Russia to roll the cuts forward into H2-19 and also likely into Q1-20.

It is clear that the global economy is still in a slow-down mode and so is global oil demand growth. Global oil demand growth is however rarely below +1% y/y unless the global economy is in a recession and as far as we can see we are not there yet at all.

Global oil demand seasonally jumps roughly 1 m bl/d from Q2 to H2. US shale oil production is currently growing at a marginal annualized rate of about 0.8 m bl/d YoY and in addition comes US NGL growth. US crude production will thus probably be 0.4 m bl/d higher at year end but on average just 0.2 m bl/d higher in H2 than in June. So OPEC+ will probably have to produce more in H2 than they did in H1 in order to satisfy seasonally higher demand unless the global economy tanks completely. Thus if Russia, Saudi Arabia and the other key OPEC members keeps production at the levels they produced in H1-19 they will ensure that the global oil market is not flowing over. They will only have to pay a small restraint while reaping a nice oil price of $60-70/bl

Two factors are coming into play in H2-19 in addition to global oil demand growth. The first is a large ramp-up of oil pipelines coming online from the Permian basin and out to the US Gulf. Cactus, EPIC and Grey Oak will add a total capacity of between 2.2 and 2.5 m bl/d from Permian to the USGC which effectively (80%) will amount to 1.7 to 2.0 m bl/d. This will help to release surplus oil inventories in the US into the global market place, tighten up the US market while easing the global situation. It will help to tighten up the WTI crude price curve while helping to ease the Brent crude price curve in relative terms. The oil market has a tendency to trade the global oil price on the back of US oil data due to lacking availability of high quality global data. Thus a draining of US oil inventories could be interpreted bullishly even though it is only shifting inventories from the US to non-US.

The other factor is the IMO – 2020 shift of fuel quality in global shipping from maximum 3.5% sulphur to only 0.5% sulphur in January 2020. In general this will add a lot of Marine Gasoil (MGO) demand from global shipping and especially so in Q4-19 and H1-2020. Global refineries will need to run hard to satisfy elevated stock building and demand already in Q4-19. This will be bullish for global crude oil demand already in H2-19. Ballpark figures are that shipping will need an additional 2 m bl/d of MGO in this period. Global refineries will probably have to process another 4-5 m bl/d of crude in order to satisfy this added MGO demand.

Ch1: Supply from OPEC+ declined 3.0 m bl/d from a peak in November last year. It looks like a decisive cut. To a large degree it is the misfortune of Iran and Venezuela. OPEC+ also boosted production from May to Nov last year and then cut from a peak.

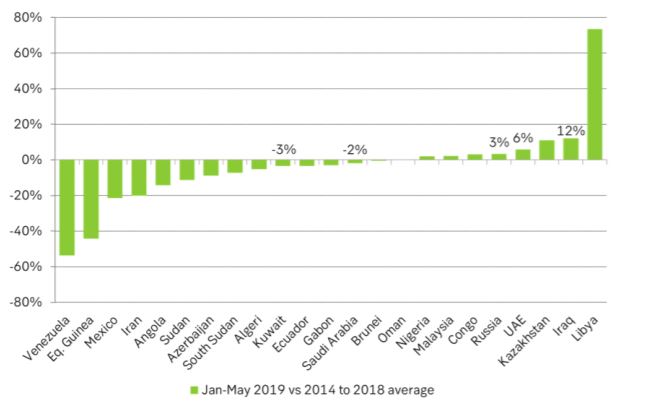

Ch2: Production in OPEC+ during Jan to May this year versus average levels from 2014 to 2018 in %. Russia, Iraq and UAE are well above while Saudi Arabia and Kuwait are just marginally below. Not a high price for these countries to hold production unchanged through H2-19 and Q1-20. Venezuela and Iran are taking the pain

Ch3: Production in OPEC+ during Jan to May this year versus average levels from 2014 to 2018 in k bl/d. Saudi Arabia produced only 173 k bl/d below the 5 year average while Russia produced 371 k bl/d above that level. They are producing at very good volumes and not really paying a high price.