Analys

OPEC+ is holding good cards and a steady course

OPEC+ is to meet virtually in Vienna today for its official half-yearly meeting. The bull-recipe is still intact: ”Reviving demand, muted US shale oil response and controlled/restrained supply from OPEC+”. This will drive inventories yet lower and prices yet higher. There are no signs of division within the group and we expect it to hold on to a steady course with very good control of the market. We stick to our forecast of a Brent crude oil price averaging USD 75/bl in Q3-21 with Brent at times trading to USD 80 – 85/bl. Come Q4-21 however we think that the group increasingly will have to consider reviving US shale oil production.

Brent crude jumped above USD 70/bl for the first time since May 2019 on signals from OPEC+ of continued reviving demand and a tightening market with plenty of room for more oil from the group in H2-2021.

Today OPEC+ will meet virtually in Vienna for their official half yearly meeting to discuss and decide on production strategies for the second half of this year. Yesterday its Joint Technical Committee (JTC) presented its outlook for the supply/demand balance for the rest of the year. It depicted continued reviving demand and a tightening balance with an expected inventory draw of 2 – 2.5 m bl/d from August to December.

What it shows is that it is most likely plenty of room (and need) for a further increase of supply from the group beyond the planned increase of 2.1 m bl/d from May to July. It also makes it much easier for the group to accommodate the return of Iranian supplies to the market.

There are still very few signs of internal strife within the group. The group is thus likely to keep on going on a steady course. The bull-recipe for the oil market is still intact: “Reviving demand, muted US shale oil response together with controlled and restrictive supply from OPEC+” thus resulting in further declines in inventories and thus yet higher oil prices.

Given that the group now meets on a monthly basis it is less of a challenge to lay out a production strategy for H2-2021 since it can adjust and revise its plan on a monthly basis. I.e. it doesn’t need to have a full crystal ball view of how H2-2021 will play out.

The natural thing for the group to do now that global oil inventories are close to the 2015-19 average is to signal an additional increase of 2 m bl/d from August to December thus leading to an anticipated inventory draw of 0.5 m bl/d during that period if the JTC is correct in its projections on Monday.

The group signalled yesterday that the return of Iranian supplies will be gradual and managed and won’t create any supply shock into the market. Between 1-1.5 m bl/d of Iranian oil exports are probably already in the market. Thus a return of Iranian supplies probably implies an added supply of about 1 – 1.5 m bl/d of crude and condensates.

The likely continued strong oil demand revival in H2-2021 is handing OPEC+ with a good hand of cards to play from and there is no indication that they won’t play it wisely and for what it’s worth.

Looking into 2022 and beyond is however much more difficult. Supply is then likely to increase from Canada, Brazil, Russia, Kazakhstan, Iran, Iraq, Libya and of course also the US. Eventually also of course in Venezuela.

With respect to US shale oil. It is not so that nothing is happening. From January to April the number of completed shale oil wells increased by 8% on average every month and 10% in April. Losses in underlying production is currently running at 424 k bl/d per month. New production from the 754 completed wells in April however yielded close to 400 k bl/d that month. Another 10% increase in completed wells in May will leave US shale oil production at a steady state production level. Yet another 10% increase in completions in June would then place US shale oil production on an annualized production growth pace of 500 k bl/d without any further increase in the number of completed wells beyond June. Add in production growth of NGLs and you have a solid production growth rate in the US. And with respect to drilling rigs. That number is increasing as well even though not at the wild pace seen from June 2019 onwards it is still rising at a rate of about 15 – 20 rigs per month thus placing US shale oil into expanding territory as the number of drilling rigs surpasses the 450 mark needed for expansion sometime in July/August this year. Expansion for 2022 that is.

Thus OPEC+ will need to keep a close eye on US shale oil players. If it looks like they aim to eat into the market share of OPEC+ by expanding too much then they are bound to be taught yet another lesson of low prices.

Our standing forecast for quite some time now is for Brent crude to average USD 75/bl in Q3-2021. That means that Brent crude at times is likely to trade to USD 80/bl to USD 85/bl. This will help to drag 2022/23 forward prices up towards USD 70/bl. Producers should bid their time well and look closely at securing forward hedges at such levels.

As the autumn progresses we expect US shale oil producers to show more vigour with reviving activity and rising production leading to a more cautious oil market and likely softer oil prices in Q4-21.

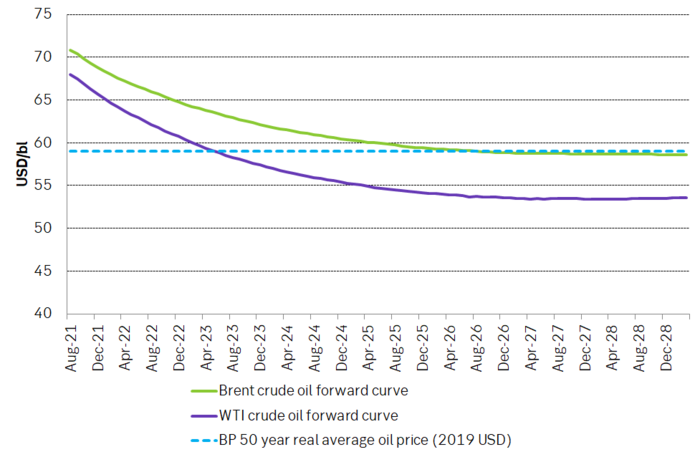

Current crude oil forward prices curves versus the 50 year real average crude oil price in 2019 USD according to BP. One should not expect oil prices to deliver at USD 70-80-90/bl in the years to come.