Analys

OPEC+ in comfortable position as U.S. shale oil slows down

This week is the week of monthly oil market reports from the three main energy organisations IEA, EIA and OPEC. The US EIA is first out with its monthly update today at 18:00 CET. Then OPEC on Wednesday and the IEA on Thursday at 10:00 CET.

We expect to see a further downward revision today of U.S. shale oil production growth for 2020 today by the U.S. EIA. In its data tables it does not specify shale oil production specifically but its projection for “Lower 48 States (excl. GOM)” is pretty much shale oil production. In its December report it projected U.S. shale oil production to grow by only 0.3 m bl/d from Dec-19 to Dec-20. That’s a far cry from the booming production growth of 1.74 m bl/d from Dec-17 to Dec-18. It also projected basically flat U.S. shale oil production in H2-20 with a contraction at the very end of the year. We expect these projections to be reduced further in its report today.

Schlumberger yesterday commented that most U.S. production projections are probably too high with peak production now reached in both Bakken and Eagle Ford. Further that at a WTI price of $55/bl there would be no production growth in the years to come and that at a WTI price of $70/bl U.S. production will probably grow at a yearly rate of 0.5 m bl/d per year. The WTI forward 5-year price strip is currently trading at $53/bl ($50.5/bl real-term).

We fully agree with Schlumberger’s comment yesterday. We have frequently seen statements from Rystad Energy about the waste reserves of U.S. shale oil deposits. We agree with that too and that U.S. shale oil production can grow robustly and even at a stunning pace also in the years to come. The big question is at what price will/can this happen while at the same time keeping investors satisfied with their returns on investments. Schlumberger’s comment yesterday is basically that there will be no further growth at the current forward WTI price level and that the forward WTI price needs to be lifted to $70/bl in order to get a 0.5 m bl/d US shale oil production growth in the years to come.

Add to this that non-OPEC, non-US crude oil production is increasingly projected to be in contraction from 2021 onwards as a result of the deep slump in off-shore investments since the oil price took a dive in 2014. Investments were booming in the five years running up to 2014. That led to a stream of new supply coming online during the following five years of 2015/16/17/18/19. Over the past five years the world has been feeding off legacy off-shore investments from 2014 and before as well as a hugely debt-driven U.S. shale oil production growth.

The year 2020 is probably going to be the last year of new non-OPEC, non-US production coming online in a magnitude that offsets production declines. I.e. non-OPEC, non-US production is likely to be in sideways to lower from 2021 onwards due to the slump in investments in this sector since 2014.

This should leave OPEC(+) in a very good position already by the middle of this year and for quite a few years after that. Why on earth should OPEC(+) throw in the towel on its “price over volume” strategy when the forward horizon looks like this? We don’t think they will. And that is of course hugely important for the oil price outlook for 2020. By and large the more significant oil price moves since mid-2014 (when Saudi Arabia stopped defending the oil price) has plain and simply been decided by shifts in OPEC(+)’s strategy between “price over volume” and “volume over price”. So if OPEC(+) sticks to “price over volume” as we think they will (we see increasing compliance to pledges) then Brent is unlikely to average sub-$60/bl in 2020.

Our Brent crude oil 2020 price forecast of $70/bl was largely viewed as close to outrageously high just a few months ago. Now we see that forecasts are gradually lifted higher and calls for $65-75/bl Brent crude oil price range in 2020 are starting to emerge as US shale oil production growth continues to slow and OPEC(+) sticks to its “price over volume” strategy. Add some improvements in global manufacturing and this will likely be the view of many.

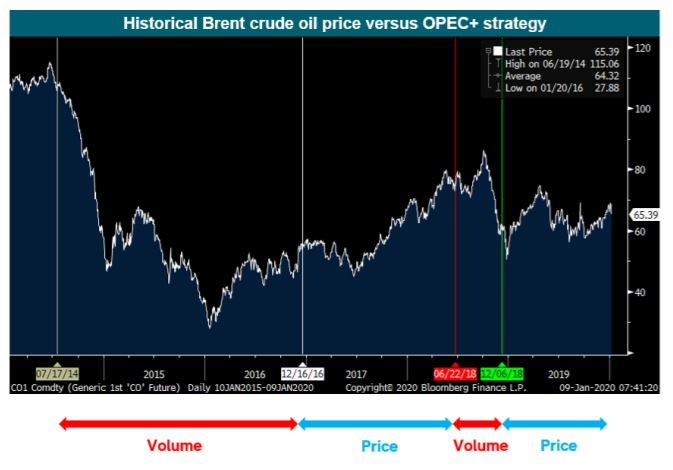

Ch1: Strategy by OPEC(+). “Price over volume” or “Volume over price”.

Saudi Arabia did not increase production from mid-2014 but it started to lower its official selling prices and stopped defending the oil price. It could have lowered its production and defended the price, but it didn’t. So basically, it shifted to “volume over price” already in mid-2014 even if it did not become official before the OPEC meeting at the end of 2014.

The strategy shifted to “price over volume” at the OPEC meeting on November 30 in 2016 with additional help from 10 non-OPEC countries. The strategy then shifted back to “volume over price” for a brief period from June 2018 to Dec 2018 before cuts were implemented again. The strategy is currently “price over volume” and we think OPEC(+) will stick comfortably with this strategy in 2020.