Analys

One year after USD -37.63/bl

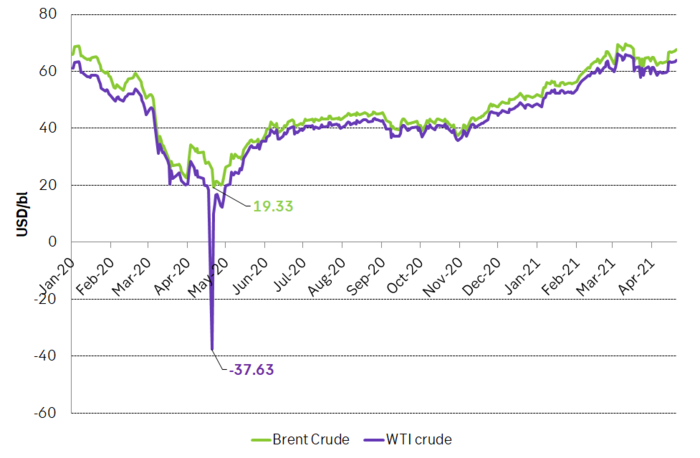

It is exactly one year since WTI crashed to USD -37.63/bl. Yes, it was probably trading games involved. Yes, it was highly specific to storage and pipeline constraints at the pricing point of WTI in Cushing Oklahoma as Brent crude only fell to USD 19.33/bl. Yes, it was a price war between Russia and Saudi Arabia which broke out after the 6 March meeting. Yes, it was Covid-19 lock-downs which killed demand. But what really stands out looking back was that you don’t steal from the King. You don’t steal from OPEC. You don’t steal market shares from the world’ lowest cost producers. Try that again and you’ll get punished again.

The price war between Russia and Saudi Arabia which broke out after the 6 March meeting last year looked like an ill considered tantrum from a hot tempered Muhammed bin Salman in Saudi Arabia lashing out against Russia which did not want to play the ”hold back production, loose market share, get higher prices” game any more. And maybe such a tantrum was really what happen. Who knows.

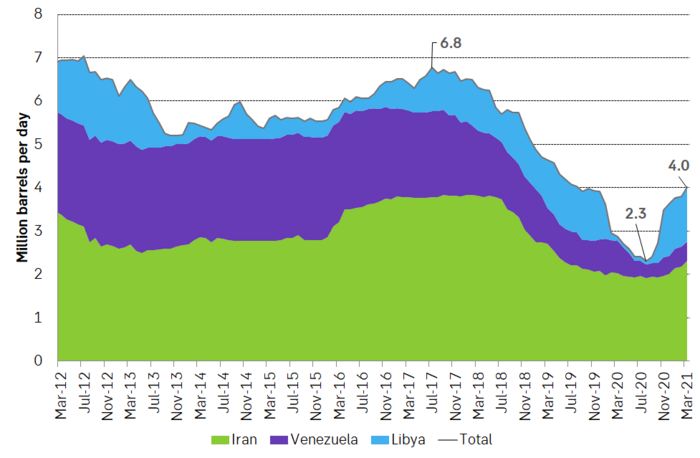

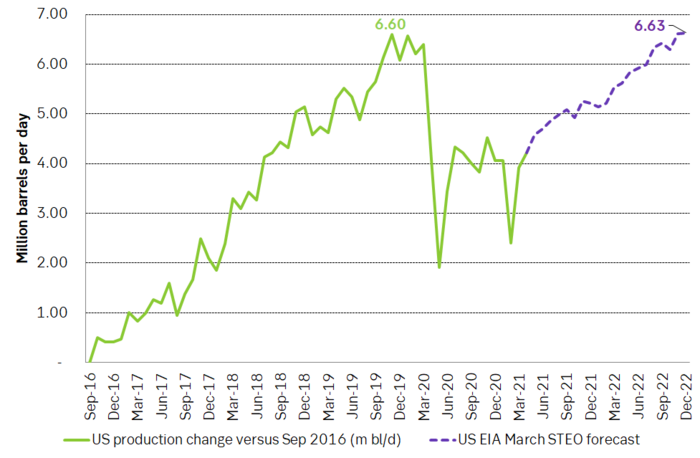

But the underlying fundamentals story here was that US liquids production was growing like crazy. From Sep 2016 to Jan 2020 it grew by 6.6 m bl/d. And Russia was sick of holding back production forever while seeing US taking more and more market share. The only reason for why this could go on as long as it did was because there was an almost comparable large decline in supply from the key OPEC producers being Venezuela, Iran and Libya which lost 4.5 m bl/d from mid-2017 to mid-2020. Thus yielding room for the incredible US production growth.

It was like the business strategy of US shale oil players was: ”Let’s steel market share from the lowest cost producers in the world being OPEC/OPEC+. Fundamentally that is a no-go strategy to start. Though it can go on for a little while before it falls apart. And it did go on for a little while but largely because of the very large decline from Venezuela, Libya and Iran. But looking back it is obvious that it had to end.

OPEC knows very well that the oil price is all about controlling supply. There is an infinite amount of oil under ground. Make sure it is not too much above ground and you’ll get rich. I.e. control your capex spending. US shale oil players obviously have been nowhere near thinking along such lines.

Looking forward is not all such a great picture if we base it on 1) The ongoing return of production from Iran and Libya. I.e. the reversal of the losses within OPEC from mid-2017 which enabled the US shale oil boom to go on as long as it did and 2) The projected non-OPEC production growth from the US EIA in its March STEO pointing to a very strong rebound in both US shale oil and total non-OPEC production towards the end of 2022.

The key message from 20 April 2020 is: Do not steal from the King. Do not try to steal market shares from the worlds lowest cost producers (it is stupid). If you do you will get punished again. In a world where oil demand is growing at around 1% over the coming years you should not lay plans for growing your production at 2% or 5% or 10% per year. Because if you do it fundamentally means that you must steel market share from someone. It for sure won’t be the lowest cost producers.

The end-game though could be that there is only one way to tame the production from non-OPEC and that is a lower price.

Brent and WTI crude prices and the crazy WTI crash to USD -37.63/bl. The recovery since then is all due to deep cuts in production by OPEC+ and still is. If OPEC+ hadn’t still been holding back significant volumes then we would have had no more than USD 30-40/bl today.

Crazy US hydrocarbon liquids growth. From a low in Sep-2016 it grew by 6.6 m bl/d before the collapse in Q1-2020. According to the EIA’s STEO from March it is set to revive and reach the same gain at the end of 2022 though the EIA STEO from April has modified that a bit lower again.

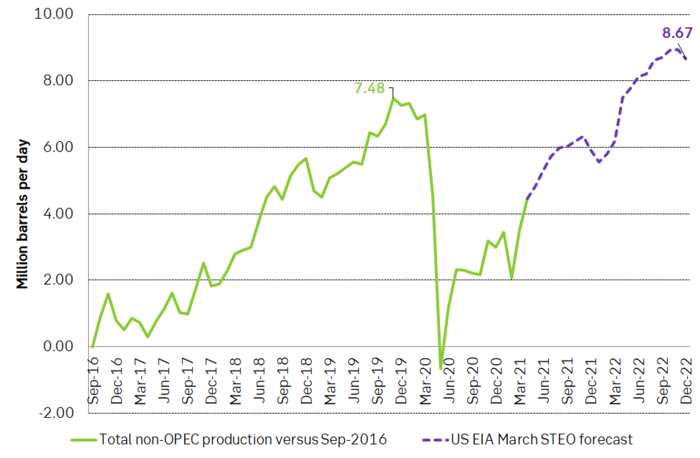

The same chart for changes in total non-OPEC production since Sep-2016 gives much the same picture. What we see is that it is not only US production which increased but also other non-OPEC producers lifted increased production in this period. But mostly it is US.

And the maga-growth in non-OPEC production did of course take their market share from OPEC. Massive decline in production by three OPEC members Iran, Venezuela and Iran. Libya has now kicked back with more to come and Iran is just about to move into the market again as signals from the ongoing Vienna talks on the revival of JCPOA (Iran nuclear deal) are positive with all sides at the table wanting the same thing. Saudi Arabia, Israel and the Iranian Revolutionary Guard may not want success but they are not sitting at the negotiation table in Vienna. A strong rebound in non-OPEC production as envisioned by the EIA March STEO forecast will be outright impossible with a production revival from these three countries.