Analys

Oman leading the way as sanctions hits physical market

Bjarne Schieldrop, Chief analyst commodities

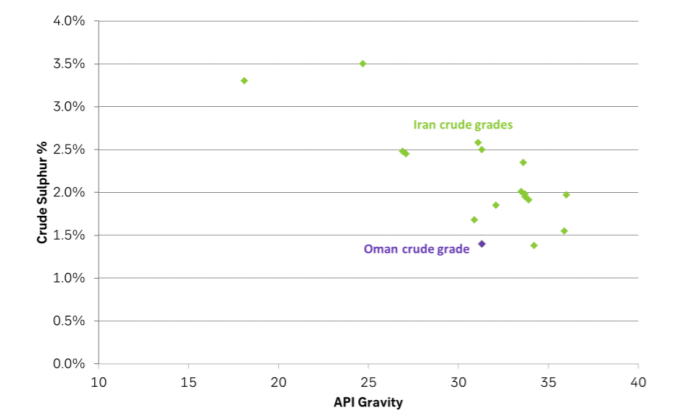

Iran’ crudes have an average gravity of API = 31 but has a higher sulphur content of 2.2%. It is nonetheless a medium-heavy, sour crude now being ripped out of the market. One could say that the actual implementation of the US sanctions towards Iran do not fully kick in before November 4. The fact is however that the real consumers of crude oil, the refineries, are doing their physical purchasing on a typical 1 to 3 months forward basis. November is now thus in the middle of this physical purchasing window.

Privately owned refineries around the world cannot afford to cross swords with Donald Trump’ Iran sanctions. They cannot afford to lose access to the global financial system (where US banks are tightly interwoven), to the international ship insurance market or to the US market in general. Thus they all do the natural thing: They do not contract physical oil from Iran for November onwards.

Thus all their physical crude purchases for the month of November and onwards are now hitting other crude oil producers instead thus doubling up the orders hitting these other producers. The sanctions are thus now fully hitting the physical market but on a two to three months forward horizon. Thus as of yet we do not see it reflected in the weekly inventory numbers. It is however still fully hitting the physical market.

Since the refineries currently using Iran crude are made to process medium-heavy, sour crude their purchases are now naturally re-directed towards other producers of this type of crude. That means Middle East producers. That means the Oman crude benchmark and not the Brent crude benchmark. This means that the Oman benchmark could continue to lead the way on this issue. So in order to look for direction of Brent crude one should keep a close eye on the Oman benchmark these days.

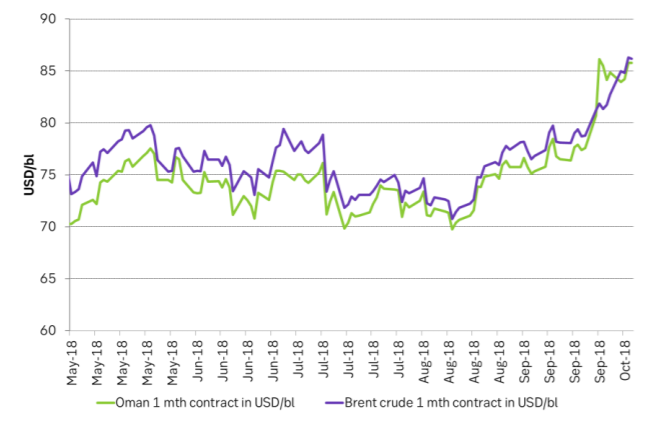

If we look at the Brent – Oman spread we see that Brent crude is only trading $0.4/bl above Oman. That is a very small margin versus the ytd average of $2.2/bl. This tighter spread may be the new norm now in this tighter medium sour crude market (due to Iran sanctions). However, if the Oman benchmark holds its stand at current level it does look like Brent is likely going to be pushed upwards. Overall it looks likely that Oman is going to be pushed yet higher and that Brent will be riding on the top of that wave higher.

When we look at the graphical development of the Oman crude price the impact from the Iran sanctions now hitting the forward physical purchasing window of the world’s refineries looks brutal. Oman has taken a pause in order to let Brent crude catch up with its upwards move but Brent needs to move another dollar or two upwards before normal spreads are re-established.

Unless the other Middle East producers offers sufficient medium sour crude on the market in this forward window in order to offset the loss of Iranian supply then Oman, your direction is up and Brent will follow or float higher on top.

Ch1: Oman 1mth and Brent 1mth. Oman led the way to break above $80/bl

Ch2: Oman crude grade versus Iran crude grades

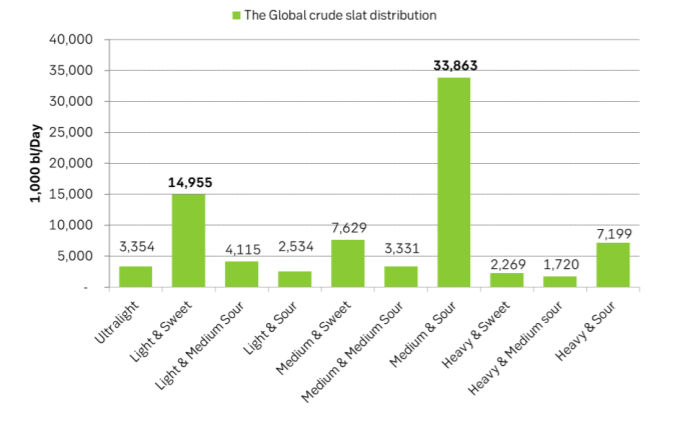

Ch3: Global crude volumes by grades according to ENI