Analys

Oil prices finding strength in rapidly declining mid-dist stocks

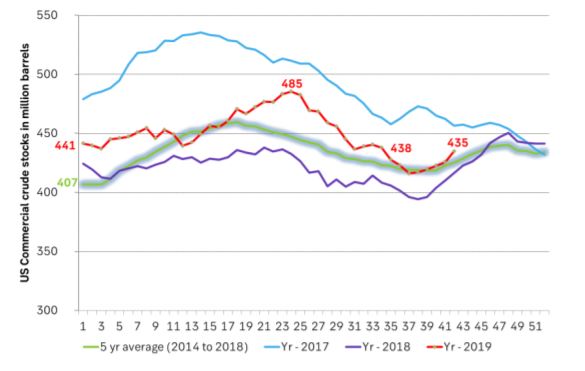

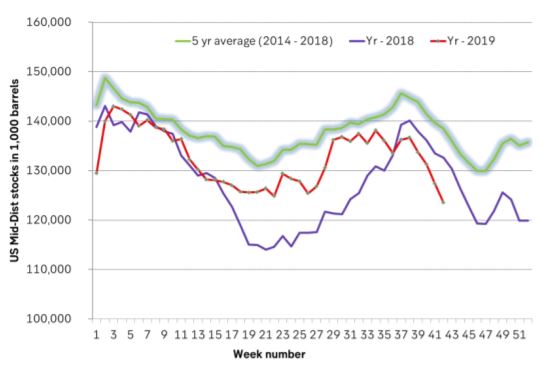

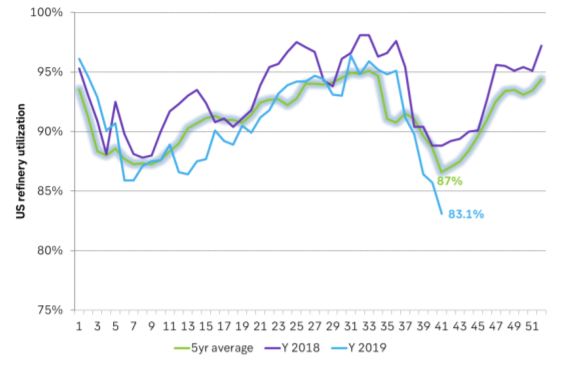

US crude stocks data ydy showed a build of 9.3 m bl last week which was almost as high as the 10.5 m bl indicated by API the day before. US refineries are running well below normal (83.1% versus normal 87%) thus processing much less crude than normal. US refineries actually processed 5.1 m bl less crude than what they normally do this time of year. The consequence is a solid drop in the volumes of oil products they crank out. This led to a continued solid draw in gasoline (-2.6 m bl) and middle distillates (-3.8 m bl) which was lower than expected and indicated by API.

Oil prices wavered to the downside for a while following the data release before ticking to the upside at the end of the session with Brent gaining 0.8% on the day with a close of $59.9/bl. This morning it is losing a little steam again trading down 0.4% to $59.7/bl as the market holds its breath for this weekend’s UK Brexit vote.

Saudi Arabia has decided to postpone its Aramco IPO at the last minute. Unfavourable market conditions with muted oil prices are probably the reason for the delay. It is probably a good decision. US shale oil production is has been kicking out drilling rigs all year (new data late today) and as a result US shale oil production growth is set to slow sharply next year. Though OPEC+ might need to cut a little more (though we don’t think so) it will no matter what be much easier for the group to control the balance in the oil market next year with US shale oil production growth slowing down sharply.

Since the start of October the USD index has declined 1.5%, global equities have gone up 2.1% and commodities have gained 1.1%. Markets are of course rocked from day to day by US-China trade agreement and Brexit being on-off-on-off. But the trend since the start of October has been a declining USD index with gains in equities and commodities.

Central banks are now kicking in with stimulus. The Fed has lowered rates twice and revived bond purchases with USD60 bn/mth. So maybe the current gloomy 2020 outlook is more about current gloom being projected into 2020 rather than what 2020 actually will be.

Monetary stimulus to counter problematic and deteriorating conditions is definitely here and now also definitely starting to ramp up in the US. The global manufacturing PMI has been in decline almost continuously since Jan 2018 and in July it had declined 18 out of 19 consecutive months in a row. For the last two months however it has been ticking higher. That’s the first two up-tick months in a row since late 2017. The latest data point shows that global manufacturing is still in contracting mode at 49.7 but ticking higher. It might be a temporary two months uptick but it could also be the start of a reviving trend backed by global monetary stimulus and a weakening USD.

Middle distillate stocks continued to fall sharply increasing the risk for a jump in mid-dist cracks in Q4-19 and Q1-20. We are now well below the 5 year average inventory level and also well below last year’s level for US, EU and Sing (weekly data time series). As a result the middle distillate cracks (refinery margins for diesel products) continues to tick higher as we relentlessly moves towards the Nordic hemisphere heating season as well as the IMO-2020 switchover in January. It is significant risk here that mid-dist cracks will continue to tick gradually higher before suddenly jumping higher. We’ll see.

Ch1: US crude oil stocks rose a strong 9.3 m bl last week

Ch2: US mid-dist stocks continued to fall sharply with a draw of 3.8 m bl

Ch3: US refineries are running well below normal and thus processed some 5 m bl of crude less than normal

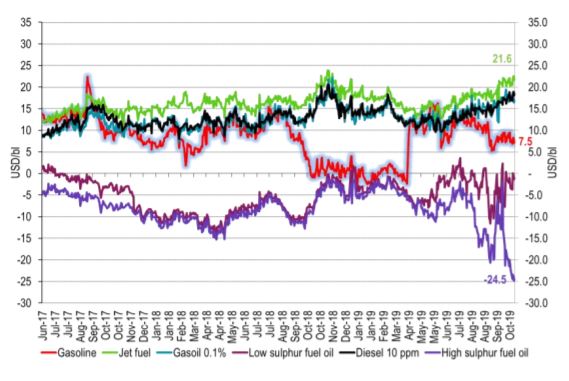

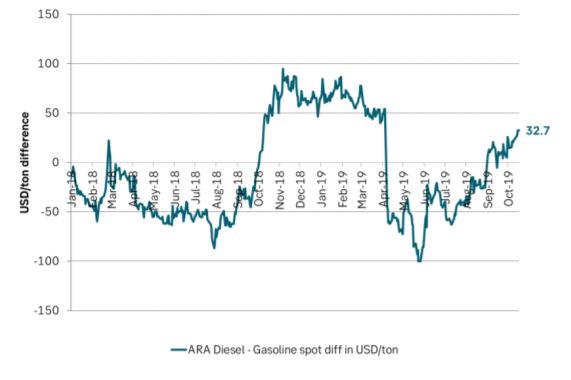

Ch4: ARA Diesel prices are becoming more and more expensive versus gasoline

Ch5: Mid-dist cracks are ticking higher and higher while HFO 3.5% bunker oil cracks have crashed and are falling further. It is clearly a risk here that mid-dist cracks are moving closer and closer towards a jump some time in Q4-19 and Q1-20.