Analys

Oil and gold remain top trades as bargain hunting drives flows

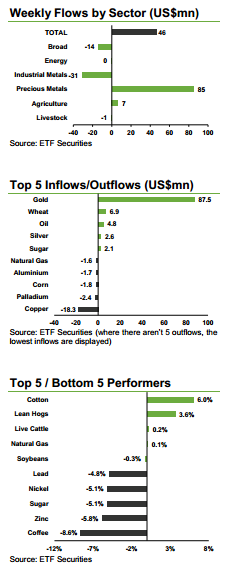

Long wheat ETPs saw their 17th consecutive week of inflows as investors mounted bets on a less bearish USDA report. After months of successive production and stock upgrades, some investors thought that last Thursday’s World Agricultural Demand and Supply Estimate report would show some stabilisation. It turns out that they were disappointed. The price of wheat fell 4.2% last week alone and is now trading at the lowest level since 2010. With wheat priced for perfect growing conditions, any small hiccup in weather in major producing countries or an escalation in trade restrictions could drive a price rally. More bargain hunting is likely with prices at multi-year low levels.

Concern over China and supply prompted another week of outflows in industrial metal ETPs, marking the largest cumulative four week outflow since May 2013. Last week, US$9.1mn was redeemed from ETFS Industrial Metals (AIGI) basket and most long industrial metal ETPs saw outflows. Long copper ETPs in particular saw US$18.6mn of outflows. Industrial metal prices declined as jitters over the health of Chinese demand troubled investors and the probability of the Philippines following Indonesia’s lead in banning ore exports has lessened. By the end of the week, however, China reported strong credit growth for the past month, which should go a long way to ease concerns about its ability to drive demand for commodity-intensive house building and infrastructure construction.

Key events to watch this week. The Federal Reserve’s FOMC meeting will be the focus of market attention. The US central bank is expected to continue to taper its bond-buying programme at the current rate, which will only leave another meeting (after this week’s) before it announces a stop to more purchases. After a disappointing US payrolls report, the market will watch out for any changes in forward guidance that could signal rate changes slower than current market expectations.