Analys

Oil and gold ETPs remain in focus despite easing geopolitical tensions

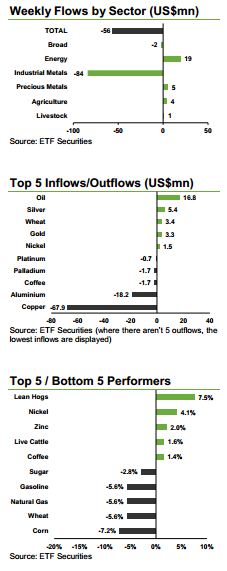

ETFS Daily Leveraged Silver (LSIL) sees the highest inflows since June as price drops to US$19oz. Inflows into LSIL totalled US$6.9mn last week. The silver price has been trending lower for the past 7 weeks and it is now getting close to attractive levels, in our opinion. While inventories remain elevated, signalling lacklustre industrial demand, silver price is trading closer to its marginal cost of production that currently stands at US$15oz. The Silver Institute expects demand for the metal to grow at around 5% per annum over the next two years thanks to a sharp turnaround in the global photovoltaic industry, led by China. In the medium term we expect the trend of destocking and price appreciation to resume as the global recovery gains pace.

Profit taking drives US$18.1mn of outflows from ETFS Aluminium (ALUM). Aluminium price is up 19% since the beginning of the year as production cuts have substantially improved the fundamentals of a market which has been plagued by oversupply for years. At the same time, copper ETPs saw US$68mn of outflows last week. Copper has lagged other industrial metals like aluminium, nickel and zinc this year, on aggressive production expectations and fears of a slowdown in China. However, we believe fears of copper oversupply are overblown and that copper remains attractive at current price levels given the underlying fundamentals.

Key events to watch this week. This week is relatively light in terms of economic releases, with industrial production figures for the UK, Japan, the Eurozone and India dominating the news flow. China’s new yuan loans, CPI and exports will also be monitored as investors try to assess the effectiveness of government policies on the real economy.