Analys

Not a single drop of US blood or mid-east oil

After having spiked to almost $72/bl at the start of the year the Brent crude oil price has now fallen back to $65.3/bl. Left, right and centre analysts are stating that we have probably now already seen the oil-price-high of 2020. That could of course turn out to be true, but it goes without saying that it is way, way too early to make such a conclusion as we after all still has 357 days left of the year to go. We are also seeing long lists of why the oil price spike could not last and why it is impossible for the oil price to move higher. The simple reason for why the oil price has fallen back and did not lift higher is of course that we have not lost a single drop of US blood or a single drop of mid-east oil yet. What is clear though is that the risk of loosing supplies in the middle east in 2020 is now higher than it was before the killing of Qassem Soleimani.

Also, through the second half of 2019 there was an almost endless gloom and doom with respect to the oil market outlook for 2020. This may of course turn out to be true, but the fact is that only after a few days into the new year we already have had the Brent crude oil price trading close to $72/bl. What OPEC+ knows very well is that what matters for the oil price is first and foremost how much oil there is above ground and not how big the resources are in the ground (because they are in principle almost endless). If OPEC+ sticks to its strategy of “price over volume” and the global economy does not fall off a cliff then the endless numbers of bearish scenarios for 2020 oil will most likely not come through.

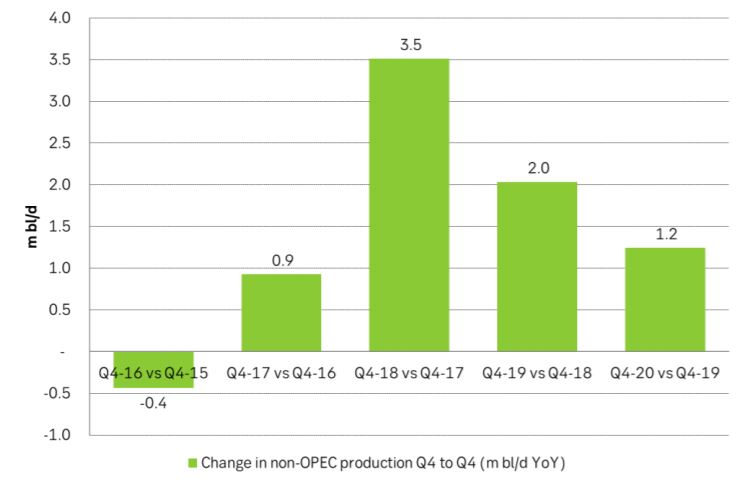

What helps OPEC+ out in 2020 is the projection that non-OPEC production growth from Q4-19 to Q4-20 is projected to grow at the slowest pace in three years due to a projected sharp deceleration of U.S. shale oil production. This makes it much easier for OPEC+ to manage the situation. Looking at the balance for 2020 it should be well within the capability of OPEC+ to manage the oil market through the year with a “price over volume” all the way through. They clearly can, the key question is more whether they want to or not.

In this respect the latest statement from Russia at the end of December is worrisome. Russia’s Energy Minister Aleksander Novak on 27 December: “Oil-production cuts can’t be eternal; we will gradually need to make a decision on exiting. Russia needs to defend its market share and let its oil companies develop new projects”.

Russia (Putin) has however spent a lot of time and effort to nurture and develop a fruitful relationship with Saudi Arabia over the latest years. What stands out looking at the oil market balance projected for 2020 by the US EIA, IEA and OPEC is that oil market surplus is mostly about the first six months of the year with mostly a balanced market for the second half. So even if the current OPEC+ deal only is agreed to the end of Q1-20 it would be a big surprise to us if Russia decides to throw away a good relationship with Saudi Arabia when all that is needed is to carry the cuts also through Q2-20.

In our view it thus looks like a fair assumption/bet that OPEC+ will carry on with its “price over volume” strategy also in Q2-20 and then the second half of 2020 should not be all that much of a problem.

Short term though the global growth revival optimism and weakening USD we witnessed in Q4-19 which helped to carry the Brent crude oil price from $57/bl at the end of September to $68/bl in late December has started to wither a little. Net long speculative positions in crude oil also built up considerably through Q4-19. So, an oil price pull-back due to a net long speculative unwind is not unlikely in the shorter term.

So far this year we have had some serious middle east jitters but with no losses of US blood or middle east oil. Further serious events in 2020 are highly likely in our view and the risk for losses of US blood and middle east oil is significant.

Ch1: US EIA projection and historical values of non-OPEC oil production change from Q4 to Q4 in m bl/d. From Q4-19 to Q4-20 non-OPEC production is projected to grow at the slowest pace in three years.