Analys

More oil from OPEC+ is the base case

Bjarne Schieldrop, Chief analyst commodities

Price action: Ticking lower with more production from OPEC+ on the horizon

Brent crude fell back 0.8% to $75.88/bl with the longer dated contracts down almost as much as the Dec-2021 contract settled 0.6% lower at $65.94/bl. The WTI benchmark however gained 0.4% to $66.36/bl thus leading to a narrowing of the spread which blew out lately. The Brent to Midland (Permian) WTI spread narrowed to $17.9/bl having recently been trading as wide as $22.0/bl. This morning Brent pulls back another 0.3% to $75.64/bl as production revival by OPEC+ next week seems more and more like the most likely outcome.

OPEC’s MOMR report yesterday contains ammunition for those in OPEC+ who do not want a production revival

OPEC’s monthly oil market report yesterday was somewhat confusing. At the start of the report it highlighted significant uncertainty for Call-on-OPEC for 2H18. It set an uncertainty range of 1.8 m bl/d with a span from 31.5 m bl/d to 33.3 m bl/d and a mean expectation of 32.1 m bl/d. In its supply/demand balance later in the report it still set forecasted a call-on-OPEC at 33.3 m bl/d for 2H18, i.e. at the absolute high end of its uncertainty range highlighted at the start of its report. There must obviously have been some considerable disagreement between different writers participating in the writing of the report. As the report said in the Feature Article “World oil market prospects for the second half of 2018”: “Given the Secretariat’s forecast for 2H18, demand for OPEC crude is projected at 33.3 m bl/d..” Thus the Secretariat seems to have more or less dictated what the official Call-on-OPEC for 2H18 should be thus overruling the analysis that the mean expected call-on-OPEC for 2H18 was projected at 32.1 m bl/d. Or it is basically just two separate pieces of analysis.

OPEC produced 32.1 m bl/d on average from January to May. Thus according to the average forecasted sensitivity analysis in OPEC’s latest MOMR report in the Feature Article there is no room for any increase in production from OPEC in 2H18. Keeping production at current level of about 32.0 would actually keep the market at a neutral balance though OECD. The story in the MOMR Feature Article is thus strong ammunition for all those in the OPEC+ group who are arguing that production should not be lifted from the current production level. Production in Venezuela is of course declining by 50 k bl/d MoM and Iran’s production is likely going to decline a little as well. There is thus obviously some room to increase production by some of the other members in order to compensate for this. The caps set in Nov-2016 are however individual caps so increasing production by Saudi Arabia and Russia in order to compensate for lost supply in Venezuela and possibly Iran needs a vote.

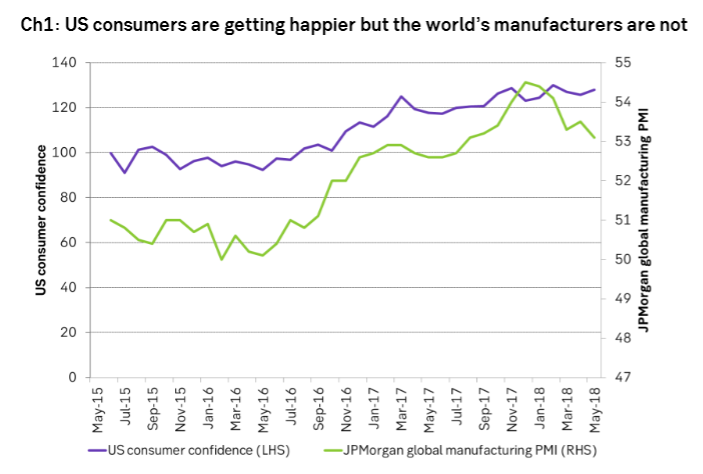

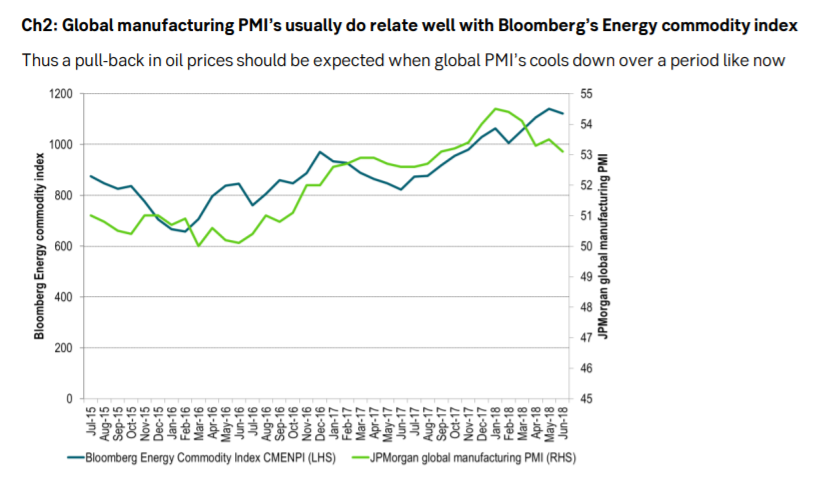

Uncertainty for Call-On-OPEC in 2H18 clearly warrants serious attention. While US consumer confidence is ticking higher the JPMorgan global PMI manufacturing index has ticked lower and lower since its peak in December last year even though it is still in positive territory of 53.1. Global growth has definitely cooled in 1H18. At the moment it does not seems as if a booming US economy is able to drag the rest of the world with it. Rather it seems like higher interest rates, a stronger USD and a higher oil price increasingly is creating a headwind for the global economy. The story in the FT today that 16 large global financial companies are down more than 20% from their peaks is highlighting the fact that the global economy is having a problem swallowing higher interest rates, stronger dollar and more expensive oil.

We expect OPEC+ to decide next week to increase production by 0.5 m bl/d in 2H18 at a gradual and measured pace.

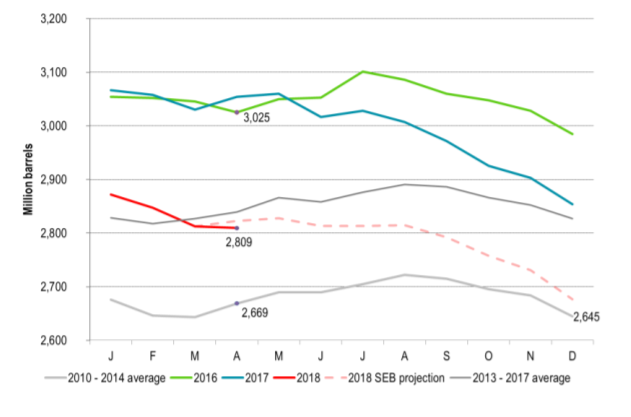

Ch3: Solid OECD inventory decline in April if adjusting for normal seasonal trendsThe OECD inventories declined

MoM by 3.1 million barrels in April. However, inventories normally rise by 26 million barrels in April. So versus seasonal trends the OECD inventories fell 28.6 million barrels in April which is equal to a seasonally adjusted deficit of 0.95 m bl/d.