Analys

Metals price forecast: Lower Before Higher

Lower before higher

The world is slowing down along with fiscal and monetary tightening. The rapid rise in interest rates this year will work with a lag so the slowdown in the real economy is likely to continue. We expect metals prices to ease along with that. The continued deterioration in the Chinese property market is likely structural with growth shifting towards higher value sectors including green energy and EVs. Chinese credit expansion has started. Stronger demand for metals like copper, nickel and aluminium is likely to emerge in H2-23. Strong prices for metals over the coming decade due to sub-par capex spending over the past decade is likely.

Weakening macro and weakening demand. The world is now in the grip of a tightening craze amid inflation panic which was the result of the stimulus boom ignited by Covid-19 panic. The US expanded its M2 monetary base by 30% of GDP during the stimulus boom. Donald Trump earlier clamped down on immigration from Mexico/Latin America. Rampant consumer spending on capital goods together with an ultra-tight labor market then led to intense inflation pressure in the US. But also, in many other countries which also stimulated too much. The US is ahead of the curve with respect to interest rate hikes. The USD has rallied, forcing many central banks around the world to lift rates to defend their currencies as well as fighting their own inflationary pressures. The Japanese central bank has refrained from doing so and has instead intervened in the yen currency market for the first time since 1998. The year 2022 will likely be the worst selloff in global government bonds since 1949 as interest rates rise rapidly from very low levels. This is taking place following a decade where the world has been gorging on ultra-cheap debt. There is clearly a risk that something will break apart somewhere in the financial system as the world gallops through this extreme roller coaster ride of stimulus and tightening. On top of this we have and energy crisis in Europe where natural gas prices for year 2023 currently is priced at 700% of normal levels. War in Ukraine, risk for the use of nuclear weapons, an enduring cool-down of the Chinese property market and continued lock-downs in China due to Covid-19 is adding plenty of uncertain elements.

Downside price risks for metals over the coming 6-9 months. The significant rise in rates around the world will work with a lag. There can be up to a 12-month lag from rates starts to rise to when they take real effect. Continued economic cool-down in the economy is thus likely. Chinese politicians seem unlikely to run yet another round of property market-based stimulus. As such there are clearly downside risks to global economic growth and industrial metals prices over the coming 6 months.

China may be a “White Swan Event” in H2-23 onward. LME’s China seminar in London on Monday 24 October this year was very interesting. The brightest spot in our view was Jinny Yang, the Chief China economist at ICBC Standard Bank. She stated that China may turn out to be a “white swan event” in H2-2023. Further that the Chinese economy now is on a decade long type of transition period. Away from property focused growth. With a shift instead to technology and innovation, telecoms and energy transition, consumer demand side economy and higher value and more advanced sectors. The property market will be a fading sector with respect to growth. Chinese politicians are fully committed to the energy transition. No slowdown in there. Credit expansion has already started. The real effect of that will emerge in H2-23. The new growth focus will be different from before. But it will still imply lots of metals like aluminium, copper, nickel, zinc, cobalt, manganese, and other special metals. There will be less copper for pipes and wiring for housing but there will be more copper for EVs, Solar power, Wind power and power networks etc.

Copper: Struggling supply from Chile, rising supply from Africa while Russian exports keeps flowing to market. The Chinese housing market normally accounts for 20% of global copper demand. So, slowing Chinese housing market is bad for copper. Russian exports keep flowing to SE Asia where it is re-exported. Good supply growth is expected from Africa in 2023. Supply from Chile is struggling with falling ore grades, political headwinds, and mining strikes. Demand is projected to boom over the coming decades while investments in new mines have been sub-par over the past decade. So strong prices in the medium to longer term. But in the short-term the negative demand forces will likely have the upper hand.

Nickel: Tight high-quality nickel market but surplus for low-quality nickel. There is currently a plentiful supply of low-grade nickel with weak stainless-steel demand and strong demand for high quality nickel for EV batteries. The result is a current USD 5-6000/ton price premium for high-quality vs. low-quality nickel. High-quality LME grade nickel now only accounts for 25% of the global nickel market. Over the coming decade there will be strong demand growth for high-quality nickel for EV batteries, but high-quality NiSO4 will take center stage. The price of high-quality nickel over the coming decade will depend on how quickly the world can ramp up low-grade to high-grade conversion capacity.

Aluminium: Russian production and exports keeps flowing at normal pace to the market through different routes. Supply from the western world set to expand by 1.3 m ton pa in 2023, the biggest expansion in a decade. Demand is projected to grow strongly over the decade to come with energy transition and EVs being strong sources of demand. Western premiums likely to stay elevated versus Asian premiums to attract metal. Increasing focus on low carbon aluminium. But weakness before strength.

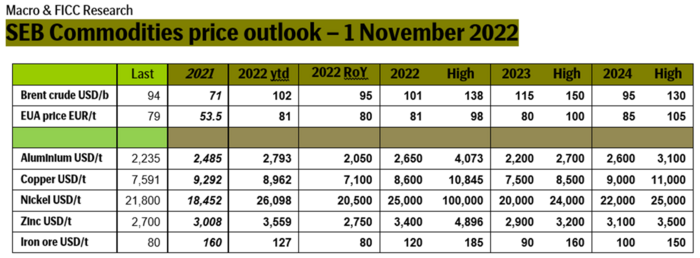

SEB commodities price forecast:

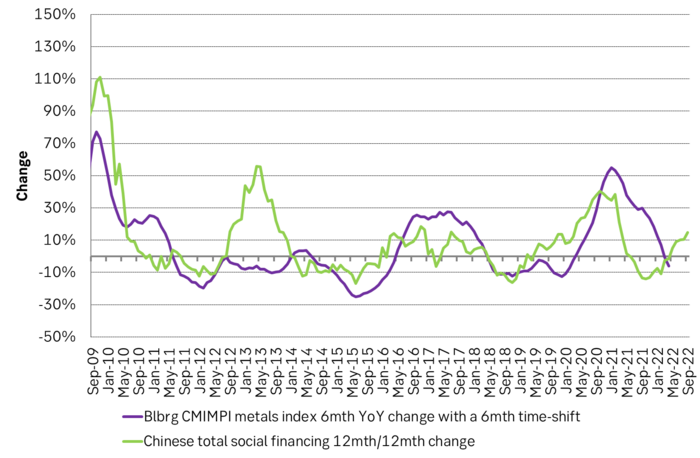

Chinese credit cycle vs industrial metals. Chinese credit expansion has already started.

This report has been compiled by SEB´s Commodity Research, a division within Skandinaviska Enskilda Banken AB (publ) (”SEB”), to provide background information only.