Analys

LME Week in three minutes

![]()

It is amazing to see what a Chinese liquidity boost can do to base metal markets. We were expecting increased bullish sentiment, but the magnitude of optimism surprised us. We think we found this year’s theme at LME Week: the discrepancy between physical and financial traders. Physical players felt it is the best market for years and parked all wider concerns, while the financial community was more cautious, believing that the current stimulus-driven rally was living on at borrowed time.

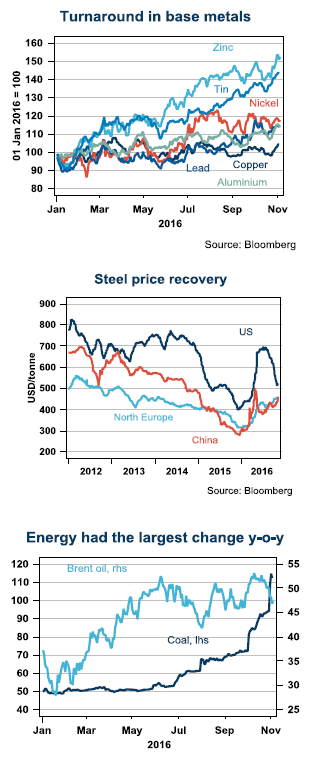

Nickel is clearly the favoured metal and offers the greatest potential, according to both our and the consensus view. Recent scepticism over policies in South-East Asian has not changed people’s minds. Zinc is still among metals with an anticipated deficit, despite this year’s remarkable price gains. Views are more bearish on copper and aluminium. Expectations for a greater divergence between metals are rock solid.

Small changes make big differences

Not much has happened to the real economy since last year. Global growth was rock steady at 2.8%, but a rising USD/falling RMD indicated a hard landing in China and the market feared the first Fed rate increase in more than a decade. Markets are now confident that the Fed will raise rates cautiously and that Chinese policymakers will launch stimulus as a backstop.

But it means that macro has become the new micro— this year’s second theme. No one is safe from a change in the big picture, as the big picture also sets fundamentals for local markets.

From a macro perspective, there is no lack of challenges ahead. Energy has been this year’s largest mover among commodities, but energy prices will probably not drive metal prices up any further. There is now less pressure on the supply side after price gains, implying much less production cuts ahead. Mining companies have seen their equity explode after undertaking simple housekeeping measures and cautiously dealing with asset temptations, but those tailwinds are now in the past.

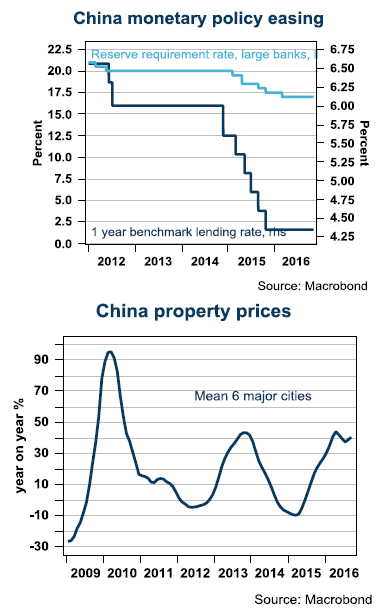

The mini-cycles in China have become more frequent but shorter in duration. After launching the infrastructure spending stimulus programme, policymakers appear to act more like fire-fighters than reformers. Credit growth has accelerated again after multiple interest rate cuts in 2015 have revived loan demand. China’s monetary policy has not been as accommodating since 2011.

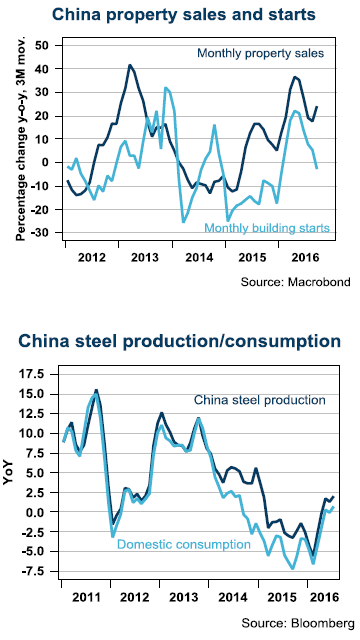

Property boom momentum fading

Policymakers spent much of 2015 directing stimulus toward the stalled property sector. Property construction is the single most important sector in the Chinese economy. The huge inventory of built but unsold property dried up after the removal of controls on speculators and cuts to mortgage/down-payment rates triggered a sales revival. The drawback of such aggressive stimulus is excessive price increases, especially in first-tier cities. Property prices in Shenzhen rose by 60% y-o-y in mid-2016. As a consequence, policymakers were forced to curb property prices once again. Increasing down-payments and halting sales to non-locals in some cities are two examples of recent steps taken to curb overheating.

Steel market rebalancing

Through a detailed plan for each province, policymakers appear to be taking a stronger stance on cutting back oversupply. Supply cuts occurred at the same time as demand received a boost from a pick-up in property markets. Both supply and demand contributed to a much better balance in the Chinese steel industry during the first half of 2016.