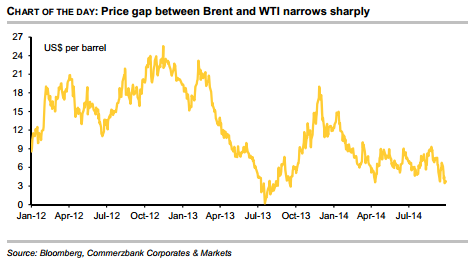

Brent is trading at $96.5 per barrel at the start of the new week and thus not far off the two-year low it reached last week. Iran has therefore called upon OPEC members to take action to prevent any further price slide. This is hardly surprising given that the IMF estimates that Iran needs an oil price of $130 per barrel in order to balance its national budget. This is the highest “break-even price” in any of the OPEC member countries and doubtless has to do not only with increased public spending but also with the lower volume sold because of the sanctions. By contrast, the Arab Gulf states, including Saudi Arabia, have much lower break-even prices which are still below the current oil price level. This also explains why they are reluctant to reduce production quantities. According to industry sources, no significant change in production volume in Saudi Arabia is likely to happen before the end of the year despite the main reason for the previous expansion of production – namely the production outages in Libya – having become less relevant. While Libya was producing less than 200,000 barrels per day for some of the time back in the spring, the production volume has recently climbed to a good 900,000 barrels per day. At the same time, demand is growing more slowly than anticipated. The Brent price is therefore likely to remain under pressure. WTI has been faring somewhat better of late, thanks in part to continued high crude oil processing rates in the US. As a result, the price differential between the two oil types narrowed on Friday to $3.5 per barrel on a closing price basis – the last time this was the case was a year ago.