Analys

Increased OPEC power in 2021 requires demand revival

Brent crude rebounded almost 1% yesterday to $64.62/bl and continues to tick a little higher this morning but still below the $65/bl mark. The signing of the US – China trade deal has given optimism for a revival in global manufacturing and thus stronger oil demand growth and this is what gives the oil price some vigour. It is very hard for OPEC to fight a war on two fronts with both rising non-OPEC supply and weakening global oil demand growth at the same time. A potential revival in global manufacturing (and oil demand growth) would thus be a great relief for OPEC and remove a lot of downside price risk for the oil price. The oil price is at its current level at the mercy of OPEC and OPEC’s current strategy of “price over volume”. If global oil demand continues at last year’s weaker than normal 1% growth rate also in 2020 and 2021 then OPEC and its allies might be forced to switch strategy to “volume over price” once again.

The monthly oil market report from EIA on Tuesday projected a lukewarm but stable outlook for the global oil market in 2020 and 2021 with Brent crude oil prices projected to average $64.8/bl in 2020 rising to $67.5/bl in 2021. It lifted its US shale oil production projection a tad for 2020 (+0.15 m bl/d) and extended the projection to 2021 with an average YoY growth of 0.4 m bl/d in 2021. That is a far cry from latest years booming US shale oil production growth. A shale oil production growth of +0.4 m bl/d per year is still a lot of new oil though.

Key assumptions in the US EIA forecast is that global demand will grow by 1.3% p.a. for the coming two years and that OPEC will stick to its current “price over volume” strategy and continue to hold back supply. EIA’s supply/demand balance “allows” OPEC to produce 29.2 m bl/d on average through the forecast horizon. The sharp decline in the need for OPEC oil over the latest couple of years is projected to halt and stabilize at around that level and then rise marginally in 2021. I.e. it projects that OPEC will be handed back a little bit of volume and market power and thus room to manoeuvre towards the end of 2021. But not a lot.

If EIA’s forecast materializes with no major disruptions in middle east supply, then we are looking at a very stable oil market with low oil price volatility for the coming two years: US shale oil production growth is slowing down and OPEC’s challenged position over the latest years is stabilizing while global oil inventories are projected to stay elevated and plentiful.

The oil price is now getting some vigour on the back of the US – China trade deal with hopes for global manufacturing revival and stronger oil demand growth. If this materializes it will put OPEC on a more stable footing and thus increase the probability that they will be able to stick with “price over volume” throughout the forecast horizon to end of 2021.

But even with a historically normal oil demand growth of 1.3% per year the oil price will still be at the mercy of OPEC’s choice of market strategy even in 2021. The US EIA is projecting non-OPEC production to grow by 0.9 m bl/d in 2021. If global oil demand grows at 1.3% that year it will hand some volume back to OPEC. Global inventories will still be high at that point, but it could be the gradual start of some lost volume starting to return back to OPEC.

True oil market strength won’t come before non-OPEC production starts to grow more slowly than global oil demand growth. This would mean increased call-on-OPEC crude oil and would hand some of the lost volume over the past years back to OPEC again. It would place OPEC in proper control of the market again with significantly reduced risk for a switch to back to “volume over price” (which would lead to a collapse in the oil price).

The US EIA projects that non-OPEC production will grow at +0.9 m bl/d YoY in 2021. This is below the historical oil demand growth rate of about 1.3% YoY (about 1.3 m bl/d) and thus projects a possible return of volume back to OPEC. That’s the turning point OPEC is looking for. However, the increase in call-on-OPEC in 2021 cannot all that easily be realized as increased production because inventories will still be high. If OPEC wants to draw down inventories at that time, they will still need to hold back production at unchanged level. EIA’s outlook is positive for OPEC, but it is at the very end of the two-year forecast period and highly vulnerable if global oil demand growth is weak. Global manufacturing revival will thus be key.

Ch1: US EIA Supply/demand balance. Fairly stable with plenty of oil in the market. Could imply low price volatility if OPEC sticks to its “price over volume” strategy all through the period. Some deficit in 2021 hands some volume back to OPEC as non-OPEC production is projected to grow at only 0.9 m bl/d YoY that year versus normal oil demand growth of 1.3 m bl/d.

Ch2: EIA projects OECD inventories to rise in 2020 and then a marginal decline in 2021. Plenty of oil in the market next two years unless we get a considerable supply outage in the middle east.

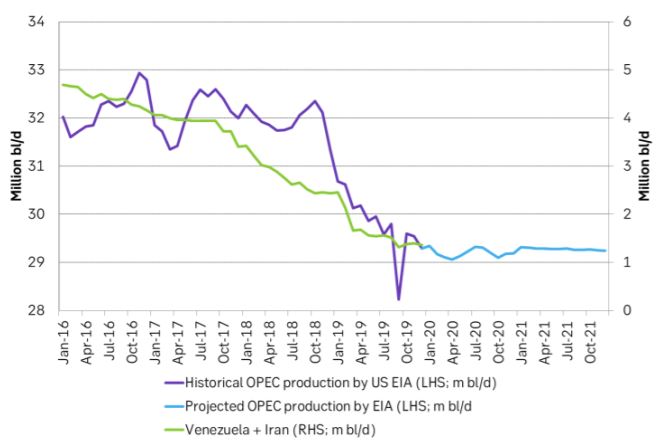

Ch3: EIA’s historical and projected OPEC production. Stabilizing next two years after a steep decline past two years. I.e. OPEC’s position looks set to stabilize at around 29.2 m bl/d versus a production of 29.6 m bl/d in December. What the outlook shows is that oil prices forecasted by the US EIA are totally reliant on OPEC sticking with “price over volume” for the coming two years and only produce about 29.2 m bl/d. No more

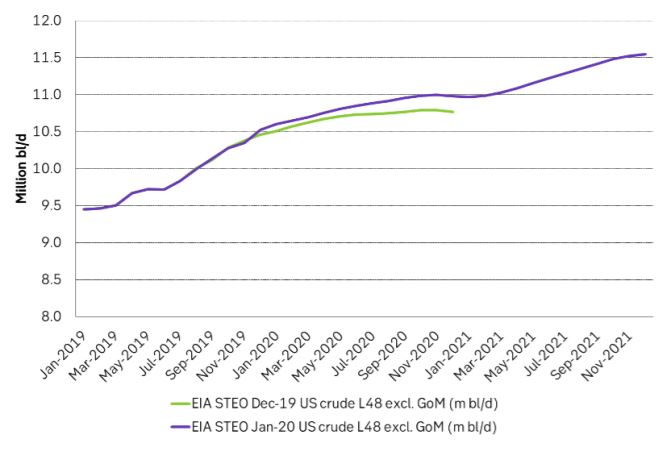

Ch4: The US EIA lifted its projection for US shale oil production by 150 k bl/d in 2020 and extended its forecast to 2021. Steady growth rate of 0.4 m bl/d in 2021. No flat-lining from 2020 to 2021