Analys

Gold and oil back in favour as geopolitical risks rise

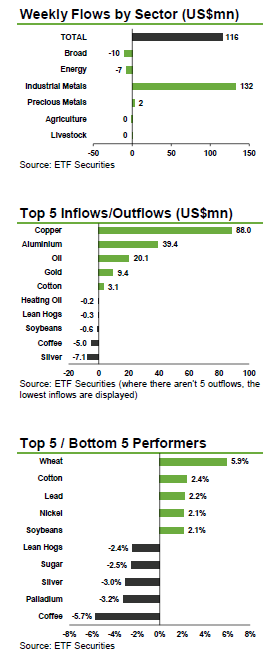

Copper and aluminium receive combined inflows of US$127mn as investors buy into China’s growth story. While weak China’s import data and heightened geopolitical risks weighed on most industrial metal prices last week, growth in the world’s second largest economy remains robust and with strong government support the industrial metal rally looks set to continue. Stronger US growth combined with a rebound in Chinese manufacturing data and more decisive monetary stimulus in the euro area should continue to be supportive of commodity prices, metals in particular, in the coming months.

Long wheat ETPs receive US$2.7mn of inflows as abundant rainfall in Europe decreased the availability of high quality wheat. Wheat prices reacting strongly to the news and were up 5.9% last week, after having lost over 7% since the beginning of the year. Long cotton ETPs also saw inflows last week, totalling US$2.6mn, on expectations of a drought in Australia, the world’s cotton 3rd largest cotton exporter. At the same time, investors reduced their coffee exposure, with long and leveraged coffee ETPs seeing over US$5mn of outflows, as price plummeted 5.7% last week.

Key events to watch this week. Industrial production statistics for a number of countries will be coming out this week, with China, the US and the Eurozone’s likely to be watched closely. Bank of England Inflation Report will also be looked at by investors, as inflationary pressure might prompt an earlier-than-expected rate hike.