Nyheter

Gaining on China stimulus, but planned production hike by OPEC+ is hanging over the market as a dark cloud

A 1% gain from China stimulus. Brent crude troughed out at USD 68.68/b on 10 September and has recovered nicely since then. Yesterday it traded to an intraday high of USD 75.17/b before settling down at USD 73.90/b. This morning it has bounced up 1.1% to USD 74.7/b on the back of China stimulus with comparable industrial metal gains. The stimulus is no big bazooka setting commodity prices on fire but rather aimed at carrying the Chinese economy to its target growth of 5%.

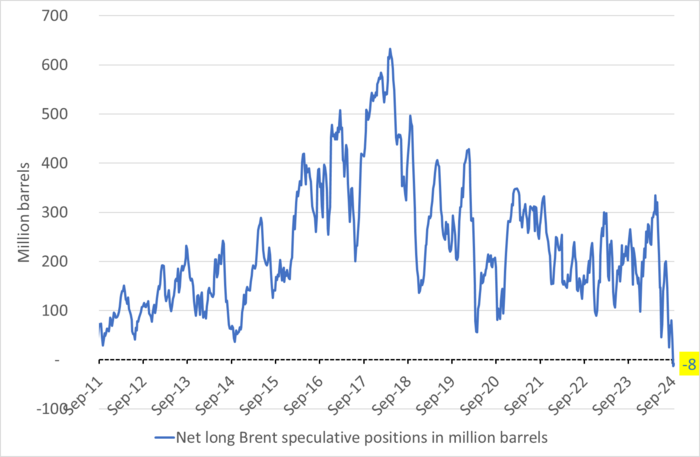

Speculators are super-short Brent crude. Speculators were net short Brent crude for a second week in a row as of Tuesday last week. Since data started in 2011 they have never been net short before. It’s an ultra-bearish positioning with investors convinced that there is more downside ahead. The oil market isn’t in surplus here and now. More like balanced. Bets are that the market will be in surplus towards the end of Q4-24 and yet more in 2025 with weak demand growth and robust non-OPEC+ supply growth.

OPEC+ was quick to modify its planned 2.2 m b/d production increase when Brent crude passed USD 75/b on its way down to USD 68.68/b. The implied information in that modification is that the group was ready to defend the oil price around USD 75/b through modifications to its planned increase in supply. But the modifications were minor. Rather than starting to lift production from October, the group will start lifting its production in December. Still by 2.2 m b/d and gradually over 12 months. That is way too much in our view. It needs to modify it further. Reduced further.

The bet of the speculators is either that a) OPEC+ will fall apart by internal struggles with supply from the group rising as a result. Or b) That OPEC+ altogether will loose the ”war” with US shale oil and non-OPEC+ producers with supply from these growing to the point where OPEC+ will have to switch from ”price” to ”volume”. Or c) That Brent crude will have to move down to the point where OPEC+ modifies its planned 2.2 m b/d production increase yet more. The last outcome seems likely in our view.

The planned increase by OPEC+ is hanging over the market as a dark cloud. The current planned increase of 2.2 m b/d by OPEC+ starting December this year is way too much. If the group sticks to that plan then we’ll have a much lower oil price than USD 75/b in 2025. It probably shouldn’t increase its production by more than 0.7 m b/d over the 12 months from Dec-24. But the way forward to make the group modify its current plan is probably through price-pain. I.e. first the oil price moves down. Then OPEC+ modifies its plans. Then the oil price moves back up to USD 75/b. What is for sure is that the group’s current planned production increase is hanging over the oil market as a dark cloud.

Net long speculative positions in Brent crude in million barrels

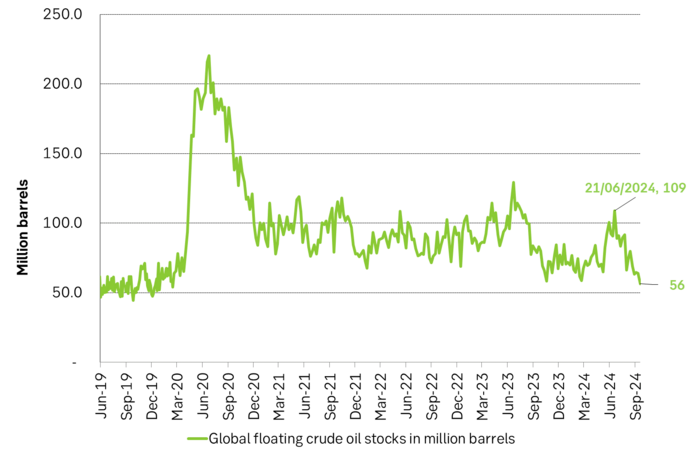

Global floating storage of crude oil has fallen to the lowest levels since early 2020. This is a strong indication that the global oil market is not in any large surplus here and now. Rather that it is in slight deficit. So bearish speculative positioning in Brent crude is about expectations for future surplus.