Nyheter

Faster than a speeding (silver) bullet

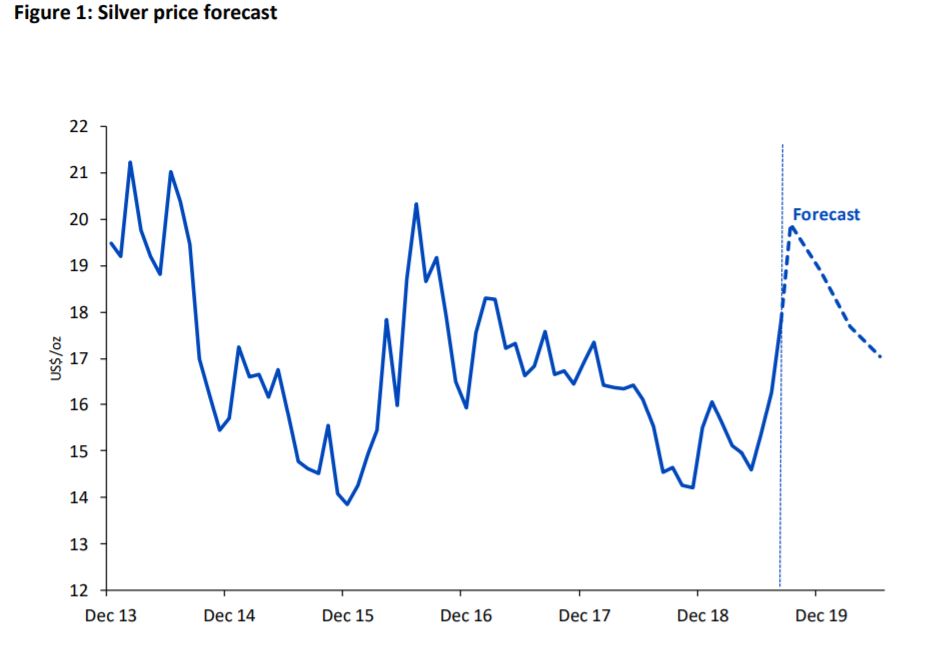

Silver has followed gold’s coattails higher, surpassing our forecasts and snapping out of a pessimistic period that had besieged the metal in the first five months of 2019. Following the upward revision to our gold forecast, we are also revising our Q2 2020 silver price forecast higher to US$17.05/oz from US$16.5/oz previously. However, silver could peak much higher at US$19.90/oz at the end of Q3 2019. So, we view a strong tactical opportunity in silver in the near term.

Using the approach we described in Silver outlook: Searching for a silver lining, we translate our new base case gold forecasts to a base case silver forecast. This incorporates silver’s strong correlation to gold. We maintain the same assumptions for other aspects of the model as we published in the Q2 2020 Silver Outlook. Namely that industrial demand for silver could suffer if trade wars continue to linger, rising capital investment in mining is likely to boost future mine supply of silver and futures exchange inventory is likely to remain plentiful. So outside of silver’s shared traits with gold, namely its role as a hard asset with defensive qualities, there are several headwinds that silver is likely to face. That in part describes why silver could lose some of the short-term gains by the end of the forecast period.

Silver has been recently playing catchup with gold. Gold had rallied earlier and initially faster than silver. The growing demand for these “anti-fragile” or “defensive” assets is rooted in the deterioration in the global economic outlook stemming from the escalation of a trade war and the possible policy responses we could see as a result. Gold was clearly seen as the first port of call for investors looking for shelter from worst-case outcomes. Of the precious metals, gold is the least industrial and the most defensive. But as speculative gold futures positioning has risen to an all-time high, some investors are rotating to silver, where positioning is less stretched.

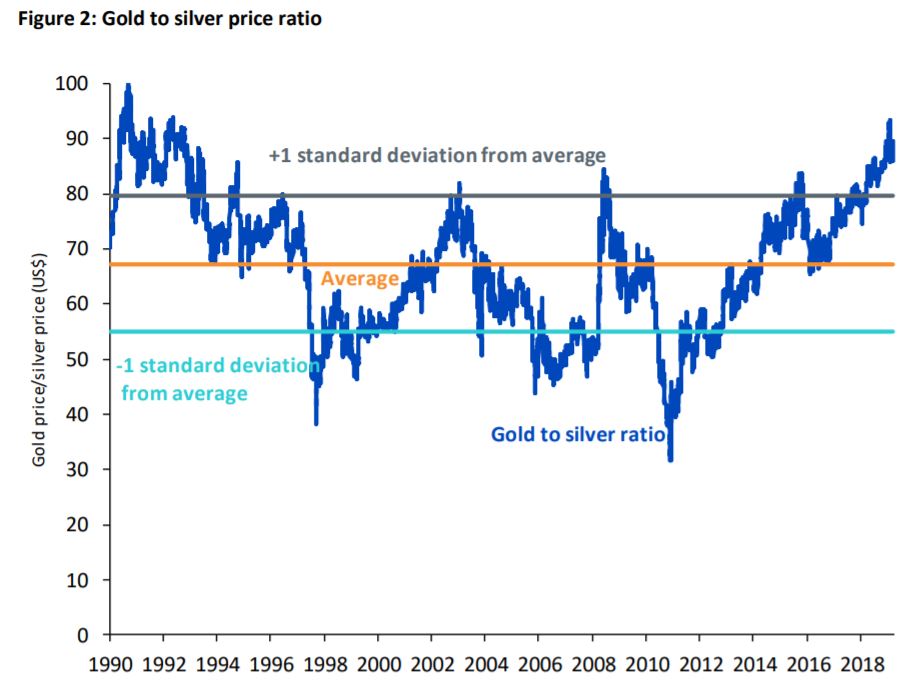

The gold to silver ratio had hit the highest levels since 1993 in July 2019, indicating that silver was very cheap relative to gold. The ratio has declined marginally in recent weeks as silver has started to rally. While we don’t think that that the ratio will fall back to its historic average, it is reasonable to assume that it could fall to within a standard deviation of the average. That would be consistent with our Q3 2019 silver forecast of US$19.90/oz and gold forecast of US$1525/oz. Toward the end of the forecast horizon, the ratio is likely to rise as the headwinds on silver bite.

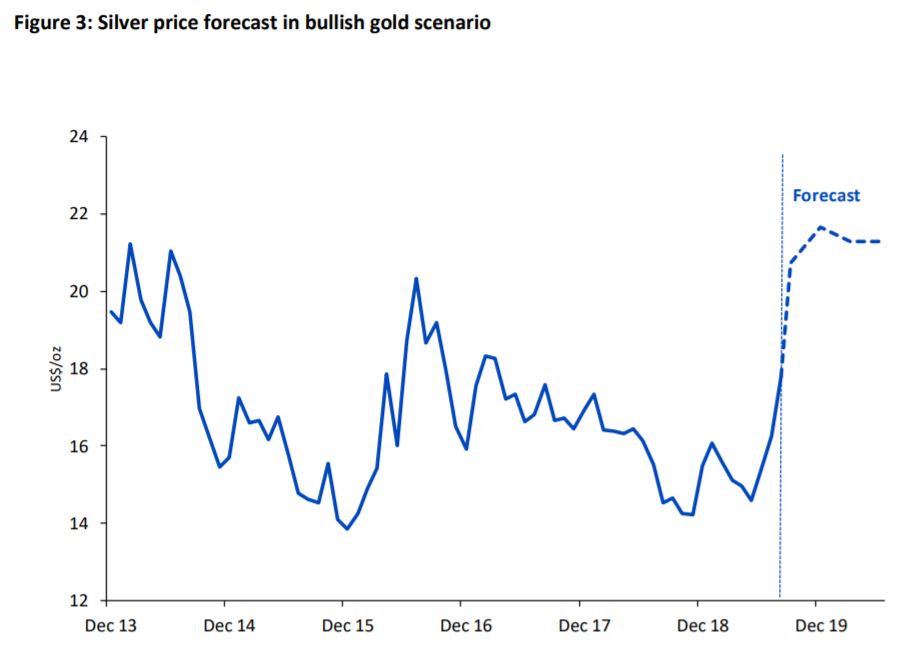

In Gold could rise to over US$1800/oz if geopolitical risks remain elevated, we presented some reasons why sentiment towards gold (measured using speculative positioning in gold futures) could remain as high as they are today. Under such circumstances, gold prices could rise to over US$1800/oz in Q2 2020. The silver price that would be consistent with that scenario (holding other assumptions in the model the same) would be around US$21/oz.

In conclusion, our forecasts point to gold remaining the best hedge for longer-term geopolitical concerns (and associated policy responses), but there is likely to be a short-term tactical opportunity in silver. Silver has already begun to rally strongly, and the momentum could continue in the nearterm.

Nitesh Shah, Director, Research, WisdomTree