Nyheter

David Hargreaves on Exchange Traded Metals, week 44 2013

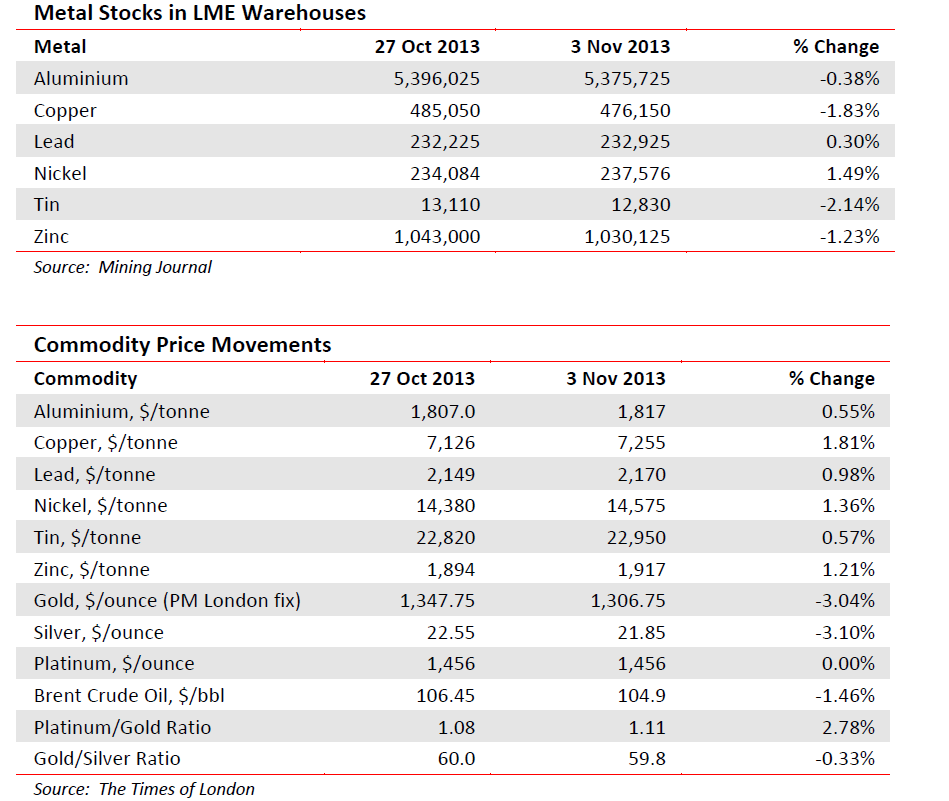

Nickel remains a troubled Metal. Its major discovery was in Sudbury, Canada during the driving of the trans-Canada railway in the mid-late 19th century (full history on request). Now the whole world produces it and Canada is but the No 5 miner at 5% of world total. In there are Vale SA and Xstrata, whose new step-parent, Glencore, is a major trader.

Such is the oversupply and the age and depth of the Sudbury mines, that lesser companies might have thrown-in the proverbial. But wait a minute, Out of those pits also comes about 4.0% of all the world’s platinum as a by-product, a sweetener. Given the state of the Pt market and the political wranglings in major producing countries RSA and Zimbabwe, it is worth a second look. Is this lost on major end users such as Johnson-Matthey and the motor manufacturers? Just a thought.

Aluminium. The desperate state of the market continues. Weighing on it is the complexity of its 3-stage process, from bauxite, to alumina, to smelted metal. The former can only be mined where you find it but the other two, energy intensive, tend to be converted where power is cheap. That largely means hydro. At the critical, refined sources, 35% is controlled by just four companies: Rio Tinto, Alcoa, UC Rusul and China’s Chalco. Quebec, where Alcoa has a major base, has always drawn relatively cheap power from the Hudson Bay plants. These plan a rate hike and Alcoa, naturally, is protesting. We speak of an annual capacity of almost 700,000/year. Only 2% of world capacity, but it would send a signal round the industry if Alcoa refused to bite. Could it afford to do so? The same company has also decided to sell its Italian plant to the Swiss group. Klesch. This ran from some years on preferential power tariffs, the name of the game in high-energy businesses. Now the Italian government wants them back.

WIM says: Where is Sig. Berlusconi now we need him?

Indonesia continues to play games with tin, that most indispensible metal where it is No 2 producer (30%) and major exporter (40%). The major importers include USA and Japan. So when Indonesia arbitrarily slapped an export ban on all-unrefined products (it does not have the smelter capacity), this upset the world trade balance. It goes someway to explaining why LME stocks of the refined metal are only 14 days’ supply. It compounded this by declaring that its relatively new exchange would be the only one authorised to do bargaining business. This one will run and short of the authorities wakening to reality (like squeezed spot – 3 month margins), it will intensify.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.