Nyheter

David Hargreaves on Exchange Traded Metals, week 12 2014

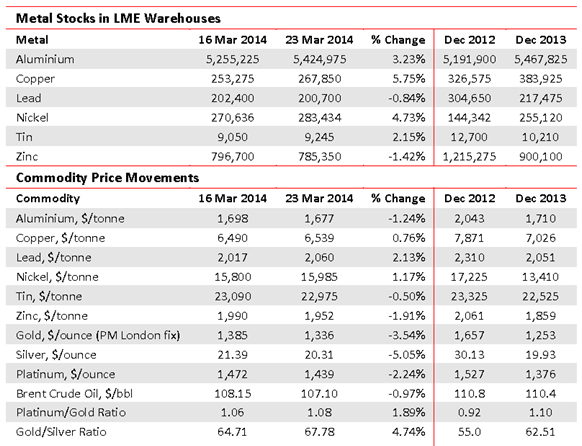

No earth-shaking movements on the week, whilst warehouse stocks nudged up for choice. Copper held its nerve after its recent and continued fall, but the news from China, which accounts for almost 50% of total demand, is still bearish.

There are doubts whether it will hit its 7.5% growth target this year, even as new copper mine projects worldwide motor on. Amongst these are Codelco’s Ministro Hales Mine (Chile, 160,000tpa) and Glencore’s Las Bambas (Peru, 450,000tpa). This latter is the subject of a potential takeover by China’s MMG Ltd. The fall in the copper price has been much more pronounced that that of its stablemates bar aluminium.

Fall in LME Metal Prices, December 2012-March 2014

Aluminium -18%, copper -17%, Lead -11%, nickel – 7%, tin -1.5%, zinc -5%

Conversely, the 15-month forward price shows that the two heaviest fallers are expected to stage the strongest recoveries. So:

LME Metal Prices: 15 months versus cash. March 2014

Aluminium +36%, copper +12%, lead =4%, nickel +17%, tin 0%, zinc 0%

Out of Commodities. Following Deutschebank’s exit from commodities, JP Morgan follows suit, selling its physical trading unit for a not-too-shabby $3.5bn to Geneva-based trading house Mercuria. Barclays, too, has joined the exodus. This puts Mercuria alongside Glencore, Vitol and Trafigura as global traders.

WIM says: So the banks are going back to basics, called money.

A rival for LME Aluminium contract. So the CME Group of the USA will launch a rival to the over 30-year-old LME contract in May. There are good pickings in a 40 million tonne physical market which some estimate to be worth $54bn of trading. The LME contract has not been without its problems, particularly with respect to warehousing. The new contract would appear to have good trade backing.

WIM says: Just a teensy suggestion: don’t quote the damn thing in cents per pound weight. The stuff is sold in dollars per tonne, worldwide, except in America. It is like quoting speed in furlongs per fortnight otherwise.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.