Nyheter

David Hargreaves on Exchange Traded Metals and Minerals, week 52 2013

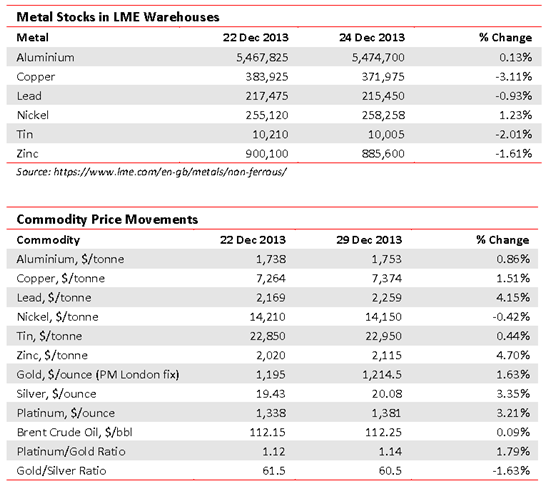

The mild recovery of 2011-12 only saw prices return to 2009 levels or below whilst this year they slipped again, albeit at a lower speed. The biggest losers have been aluminium and nickel, each the victim of current and potential oversupply. Rio Tinto has lived to regret its expansion in aluminium via its purchase of Alcan and likewise Vale SA, picking up INCO and the Sudbury, Canada nickel field. Of the survivors, lead did so on a surge in the electric battery market and tin on the technicality of Indonesia’s restriction of exports (see Countries).

Summary. To repair their balance sheets, the producers have continued to pump out metals, thus adding to the surplus. Some have delayed major new developments, but these are on hold, not cold storage. Thus the expected recovery in the world economy, led by the USA will not lead to extreme shortages nor runaway price increases. The best we can expect is consolidation.

The International Copper Study Group (ICSG) tells us 2013 copper usage was flat at 20.5Mt, demand will rise 4.5% in 2014, but refined output will rise to around 22.1Mt with the surplus at 632,000t, up from 387,000t. Barclays Bank is bullish on nickel, looking for an average $14,750/t next year, from $14,150/t now (that’s a bit precise and leaning on Indonesia’s export ban). Like WIM, it is bearish on gold and oil.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.