Nyheter

David Hargreaves on Exchange Traded Metals and Minerals, week 2 2014

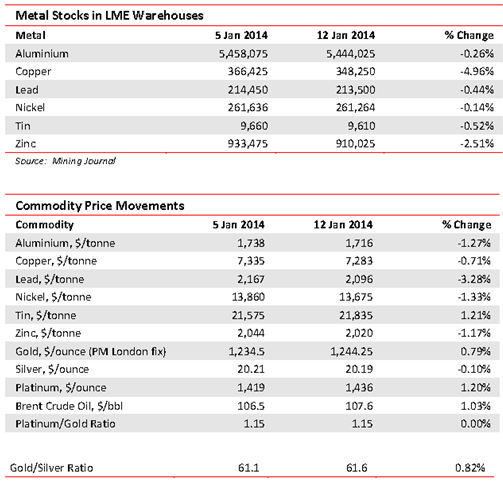

The major miners continue to stress that they are postponing or cancelling new projects, which could lead to shortages as early as 2015-16. To fill the gap and to repair their balance sheets, they are high-grading and expanding at existing operations. Classic examples include Freeport (FCX.N $36.17; Hi-Lo $38.09-26.38) which would, subject to the Indonesia government seeing reason, up its copper output by as much as 12% to make 500,000t and gold by a whopping 47% to about 55t. Chile’s copper mines are also stepping-up to the plate as is Rio Tinto’s Bingham Canyon and new producer Oyu Tolgoi in Mongolia. Nickel and aluminium show little sign of tackling their oversupplies, leaving zinc the possible exception on mine exhaustion grounds in Canada and tin on Indonesia’s intransigence regarding the export of refined metal only, despite a lack of smelter capacity.

Glencore is reported to be restarting its 150,000tpy rated Pasar smelter in the Philippines, following the typhoon there. Output losses are estimated at 15,000t-30,000t.

Aluminium may be in oversupply, but premiums to recover metals from warehouse are increasing. The blame is laid on smelter closures and low interest rates encouraging traders and investors to pick up metal which they keep in storage. Over-capacity casualties include Dutch smelters Al Delfzijil, 110,000tpa which has filed for bankruptcy and US Ormet Corp closing its 270,000tpa Hannibal, Ohio smelter. The total market for newly produced metal exceeds 50mtpa.

Zinc presents a somewhat different picture in that not only exhaustion of orebodies, but strong end uses persist, particularly in the construction and automobile galvanizing sectors. A hot location for expansion is Namibia whilst Anglo American decided zinc was non-core, even as Glencore embraced it.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.