Nyheter

David Hargreaves on energy, week 4 2014

Unlike their base and precious metals cohorts, bulk even, energy minerals tend not to have violent daily or even weekly swings. But they do have trends. So:

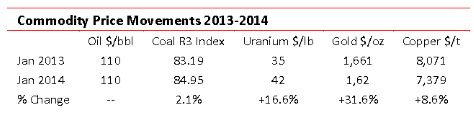

Reason: With energy there is a choice more so than metals. WIM has dealt with this at length so let us deal with the trends: Nuclear is fast losing friends which the price of its base fuel U3O8 shows. The cost, time to delivery and inherent dangers make it only for the uninformed or desperate. Germany and Switzerland are opting out. Japan will probably not come back. Neither will the USA. Of the hopefuls, Britain dithers as it does on most matters and now RSA is blowing cold. Which leaves China. Its energy demand is such that its decision could be indicative. It will still take up to 10 years in development. Yet it is sneaking into uranium supply sources, so let’s pay attention. China National Nuclear Corp has just bought a 25% stake in Paladin’s up and coming producer, Namibia mine, Langer Hendrich for $190M. Historically, this is cheap. It is China’s second foray into uranium in Namibia – world No 3 producer – following CGNC taking over the Husab project for $2.3bn in 2012.

WIM says: This is an over-supplied market, leave well alone.

Coal has its detractors, but if one of the world’s larger terminals, RBCT in South Africa feels the pulse, it is racing. The privately-owned facility, fed by state-controlled Transnet – plans to up its capacity by 19Mtpa to 110mtpa to accommodate junior miners.

WIM says: The two entities, state and private, must cooperate, but it will be fraught particularly since the country has a government-controlled entity, ESKOM, reliant on coal as the primary energy generator.

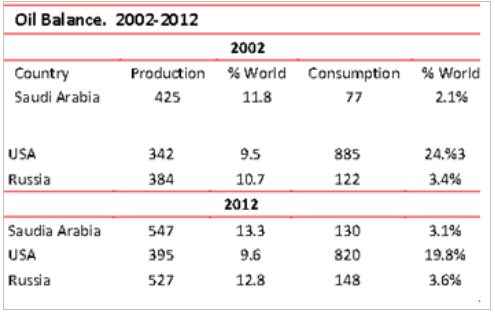

Saudi Arabia. Just pause for thought. The world’s largest oil producer says it is not concerned about the USA overtaking it. To keep its own output for export, the Kingdom is into renewables – it has lots of sun, but no wind or water – so it is game on. Of course it pivots around the US shale oil.

The changes are indicative, if not mould-breaking. The three majors in energy, together account for over 30% of supply and almost the same of demand. The shifts are that the USA is moving towards a balance whilst the other two increasingly rely upon exports. These features will influence the energy pattern in the years ahead. Maybe Saudi Arabia should not care about America’s oil shale boom. It has 63 years’ current supply, 16% of known world reserves and it comes out at about $10/bbl on the surface.

Met Coal Prices remain squeezed on the world markets at a $147/t fob Australian port. US exports are to blame, says Macquarie Bank, looking for a $10-15 fall to ring the warning bells. Survival of the fittest says Mining Journal.

South Africa may back out of nuclear. It currently has the one, ageing station, Kusile, but any additions will come at a perhaps untenable cost. They speak of a cap of $6500/kw (the UK’s Hinkley Point looks at $7500).

WIM says: We see them sticking with coal, which they know and love, plus shale?

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.