Nyheter

David Hargreaves on Bulk Minerals, week 49 2013

Potash. There is more to this market than the collapse of the sales cartel. It is increasingly obvious it is over supplied and the pipeline is full. Thus, a buyers’ market. The major customers, Brazil, India, China, are wily birds. So the pressure on the supply side. It is two-fold: Those with it and have too much; those developing who are facing a potential surplus. To the former, Canada and Russia have a tight grip on a +50Mt/yr market for the essential fertilizer market worth, even at recently reduced prices, up to $20bn per year.

Effective marketing cartels have, until recently, ensured lucrative margins. They are no more, since the Russian arrangement between the world’s largest miner, OAO Uralkali and it partner Belarukali, fell apart. It resulted in the potash price collapsing from a transient $700/t to nearer $300/t. Even at this, they still talk of $150/t margin. In Canada, leader Potash Corporation is cutting back with over 1000 employees to get the axe in a combined efficiency and output reducing measure. Its local competitors Agrium and Mosaic Co. are likely to follow suit. WIM says: It takes 5-7 years to develop a deep potash mine and those who plunged in recently are feeling the pain. They include BHPB (Jansen, Canada), Sirius (UK) and Vale.

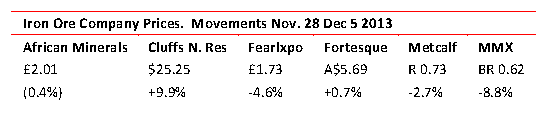

Iron Ore continues its steady recovery, although not cheering – much – share prices. We note:

This does not alter the picture for a potential long term ample supply, based on Australia and West Africa in particular.

We note:

London Mining (AIM 111.50p Hi-Lo 189.75p-86.00p) has shelved plans to bring in a partner to help expand its Marampa, Sierra Leone, Mine. Instead it will concentrate on reducing debt and returning cash to investors. In its efforts it says: refinanced existing debt will be upped by $20M to $200M to fund expansion to 6.5Mt/yr plus the extended maturity of a $110M convertible loan, from 2016 to 2019 at a coupon rising from 8% to 12%. That is hefty.

Chinese imports of iron ore, perhaps more correctly, Australia exports, are on the up. Port Headland, which handles up to a fifth of all seaborne trade, saw an increase in exports of 38%, year-on-year, in November 2013. 22.3Mt went out in the month. Japan to 2.2Mt (also up 38%) and Korea doubled to 2.9Mt. The port handles cargoes for BHPB, Fortesque and Atlas.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.