Analys

Cutting supply of “black crude” will feel like more

When OPEC+ now is cutting supply of at least 1.2 m bl/d of crude they are primarily cutting supply of medium sour crude or “black crude”. In exchange the market is left to consume more light to ultralight US shale oil crude and NGLs.

Bjarne Schieldrop, Chief analyst commodities, SEB

US shale oil typically contains about 60% medium to heavy molecules. But if we also factor in the added supply of US liquids which is NGLs etc. which contains 0% such molecules then the total comes down to only 40%. I.e. average new liquids supply in the US only contains a 40% cut on average of medium to heavy molecules.

“Black crude” (medium sour) in comparison contains close to 80% medium to heavy molecules. I.e. twice as much as the new US liquids supply. So when OPEC+ now cuts 1.2 m bl/d of “black crude” it reduces supply of medium to heavy molecules by 0.93 m bl. To make up for this the US has to lift total liquids supply by 2.3 m bl/d.

You can always break apart longer hydrocarbon molecules to medium length molecules (mid-dist. and lighter). Yes, it is an expensive process but the equipment for splitting longer hydrocarbons is still widespread in the global refining system today. All from splitting VGO (Vacuum Gas Oil) to either Gasoline (by Fluid Catalytic Crackers (FCCs) or to middle distillates (by Hydrocrackers) to breaking apart vacuum residue in Cokers to mid and light products. But merging shorter molecules and converting them to middle distillates is way more difficult and expensive and is in general not done. The exception of this is Shell’s Perl, Gas To Liquids (GTL) plant in Qatar where natural gas is converted to diesel. But that is more one of a kind.

From end 2016 to end 2018 the US has increased its hydrocarbon liquids supply by 4.2 m bl/d consisting of 2.9 m bl/d of crude and 1.3 m bl/d non-crude (typically NGL’s). The later typically contains no medium to heavy molecules while the prior contains 59% such molecules or less. In total the 4.2 m bl/d of new liquids supply in the US has added 1.7 m bl/d of medium to heavy molecules or 0.4 m bl/d per m bl/d of additional US liquids. “Black crude” however typically contains close to 78% medium to heavy molecules.

The huge change in the oil market due to the arrival of booming US shale oil is many faceted and complex. The new molecule composition in US liquids supply growth is one of many. Of this aspect we have probably only seen the start. Most new refineries are in general geared towards Middle East medium sour crude or “black crude” and the new ultralight liquids supply from the US does not match these all that well. The new Chinese INE crude contract is typically defined as medium sour crude if we look at the crude streams going into the physical delivery of this contract. That is to match the Chinese refineries.

Again, when OPEC+ now is cutting 1.2 m bl/d of black crude it is more than meets the eye. The feel of this cut will be deeper than its headline number of 1.2 m bl/d and it may not lead to all that much of a blessing for US ultralight liquids supply as producers there hope for once the cut starts to bite.

Today at 16:30 CET we’ll have the US EIA oil inventory data. They are likely to be quite bearish. Given the US EIA’s drilling productivity report this Monday we are likely going to see that the EIA lifts US crude production by 100 to 200 k bl/d versus last week. The API yesterday indicated stock changes of US crude: +3.5 m bl, Gasoline: +1.8 and Distillates: -3.4 m bl. In total a rise and also bearish for crude if that is the outcome.

Positive note: Dimondback is cutting activity in the Permian basin in 2019 in response to lower crude prices and higher costs.

Ch1: US ultralight crude versus Brent crude and Oman crude. The difference is much larger if one also includes US supply growth in NGLs

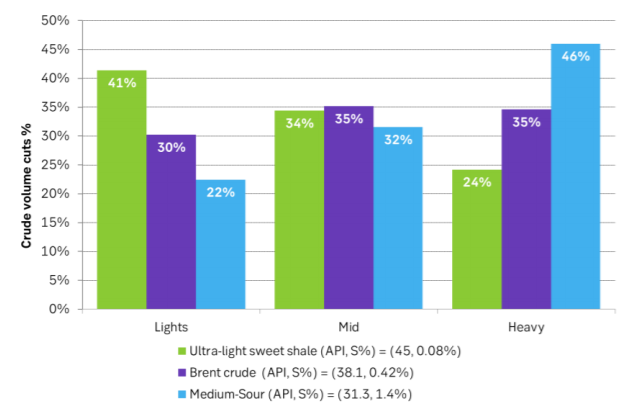

Table 1: Ultralight US shale oil contains much less medium to heavy molecules

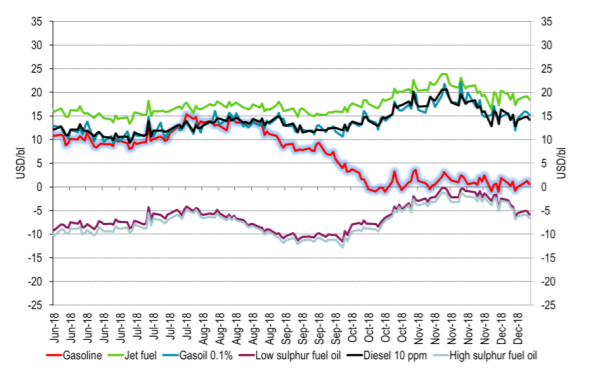

Ch2: Mid-dist and heavy ends; much more fun than gasoline lately versus what is usually the case. Probably just the beginning.

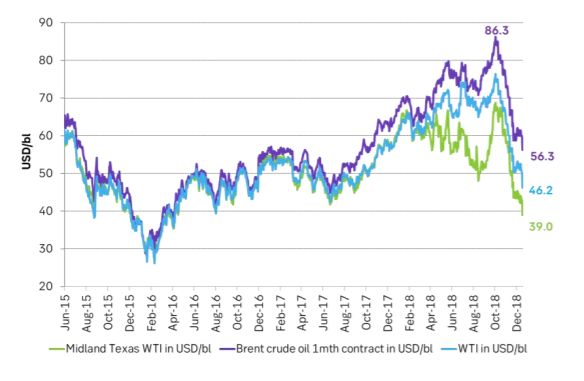

Ch3: Crude prices falling like a rock

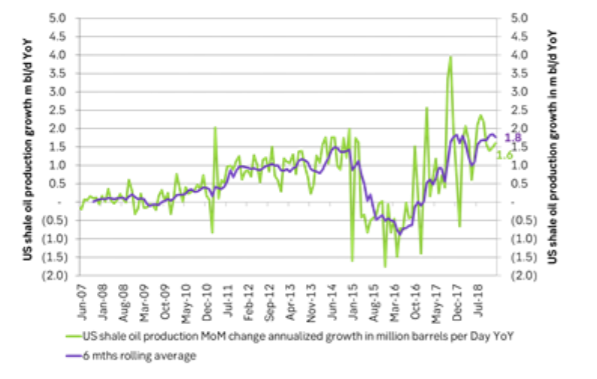

Ch4: US EIA drilling productivity report on Monday. Only bearish reading as of yet: higher drilling, higher DUCs, higher production, higher productivity and a marginal, annualized production rate of 1.6 m bl/d per year. Lower crude oil prices have not yet started to impact activity in December and January. But news above from Dimondback shows that prices are starting to hurt.