Analys

Carried higher by declining US oil rigs and declining oil inventories (and speculators rolling into the front end of the curve)

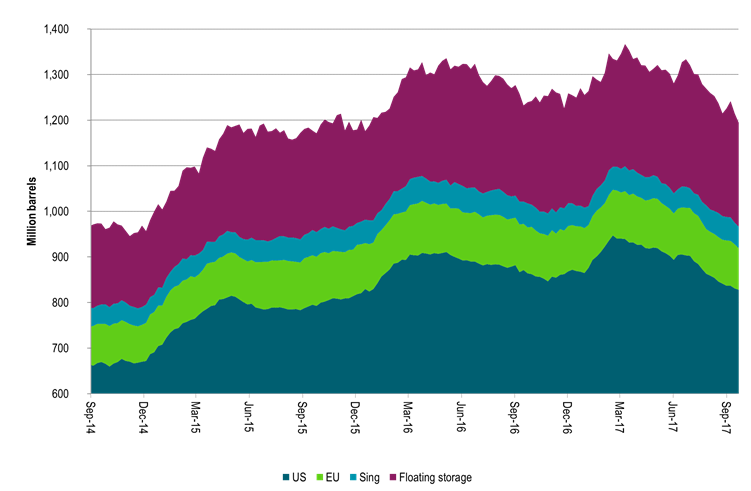

Inventories continue to decline steeply in weekly data with declines of 21 mb last week and 48 mb over the last two weeks, 59 mb over the last 6 weeks and 173 mb since mid-March (including floating storage / oil in transit). As a result the forward Brent crude oil curve continuous to bend further into backwardation in a way we have not seen since back in 2014.

The backwardated Brent crude curve is like honey for bees for investors and speculators as it hands investors with long positions at the front end of the curve with a positive roll yield even if the Brent crude spot price only moves sideways from here. So even if you as an investor is only neutral to oil prices it still makes sense to hold a long front month Brent crude position. Over the last 14 trading days the average, annualized Brent 1mth roll yield is 5.8% pa and today it stands at 9.9% annualized return. I.e. that is if the spot price moves sideways over the next 12 months and the backwardation continues at current steepness.

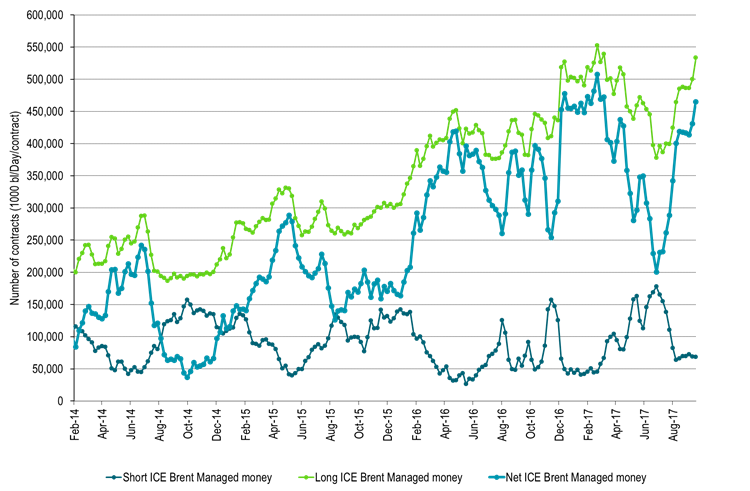

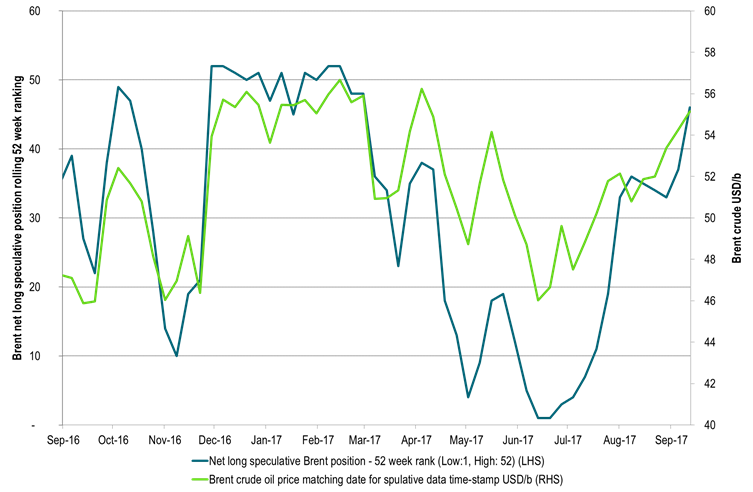

In a close to zero interest rate world this Brent backwardation positive roll yield must be like honey for bees. Speculative positions for Brent crude have not yet been updated this week. But if we look at positions published one week ago we see that the net long Brent crude position by managed money stood at the 46th highest level in 52 weeks and has probably increased further since then.

Those who hold a plain long Brent 1mth position will get a roll yield due to the current backwardation. However, they are also exposed to the downside in case we get a setback in crude oil prices. There are probably in addition a lot of speculators who only want to speculate on the backwardation itself thus placing a long Brent 1mth contract against a short Brent 6mth contract betting on further inventory draws and yet steeper backwardation. Adding such speculations adds to the steepness of the backwardation during the process when speculators add them on to their books.

We also have passive Brent crude speculators holding long Brent crude ETFs which automatically places the financial long Brent position at the 12mth horizon when the Brent curve is in contango (to avoid steep losses from rolling in front end contango) but then automatically shifts this over to a Brent 1mth position when the curve shifts into backwardation. Thus when the curve naturally shifts into backwardation then the speculative shift will add to this due to the automatic selling out of long specs held on the 12mth horizon while adding length in the front end.

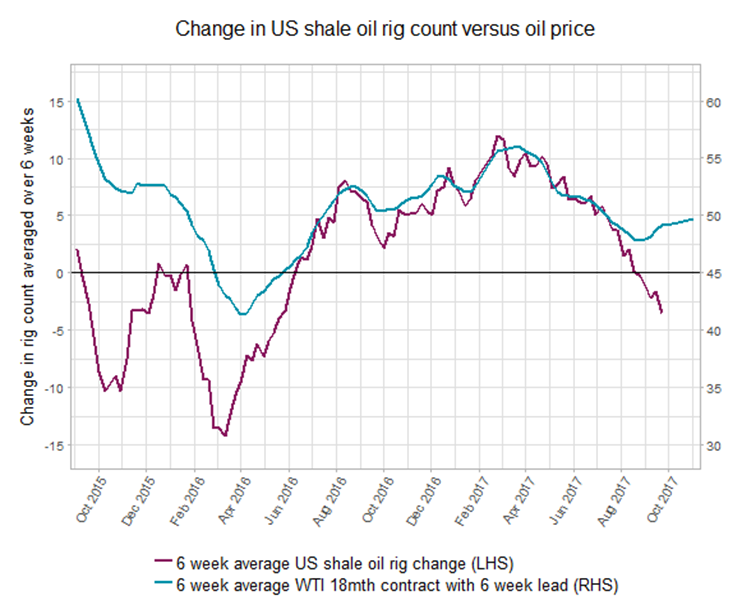

Inventories continue lower and the Brent crude curve continues to steepen due to both natural (inventory declines) reasons and speculative pressures. In addition we have sentimental support for the oil complex by the fact that US oil rigs have declined five out of the last six weeks. The decline is quite steep even though the relevant WTI forward crude prices have traded close to $50/b during the last 10 weeks. Thus US shale is currently saying: WTI @ $50/b is not enough for adding rigs at the moment. Actually it is too little.

Thus the arrows are pointing to higher levels (also supported by technical indicators) with ytd high of $58.37/b within reach as we now traded at $57.2/b. However, Brent speculative positions are getting stretched. Thus we will get a correction down the road. What the trigger might be is hard to say. An equity correction in combination with a USD rebound/rally (October and November usually strong dollar months), emerging market risk-off as well as a possible increasing concern for whether OPEC+ will roll forward its cuts beyond 1Q18 could be the outline for such a correction. The current steepening Brent backwardation would then get at setback as well. But as of now we are heading higher but beware of the of the altitude.

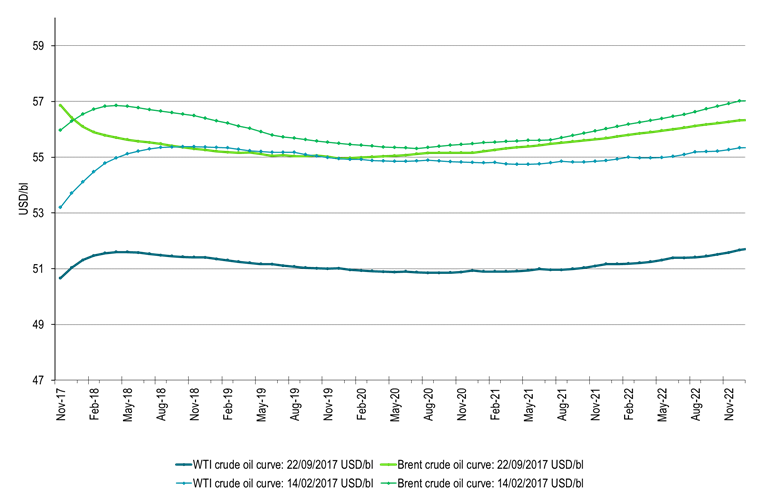

Ch1: Brent crude oil forward curves

Wider Brent to WTI in the front has rippled along the forward curve

Ch2: Brent to WTI December 2020 from zero spread start of year to more than four dollar now

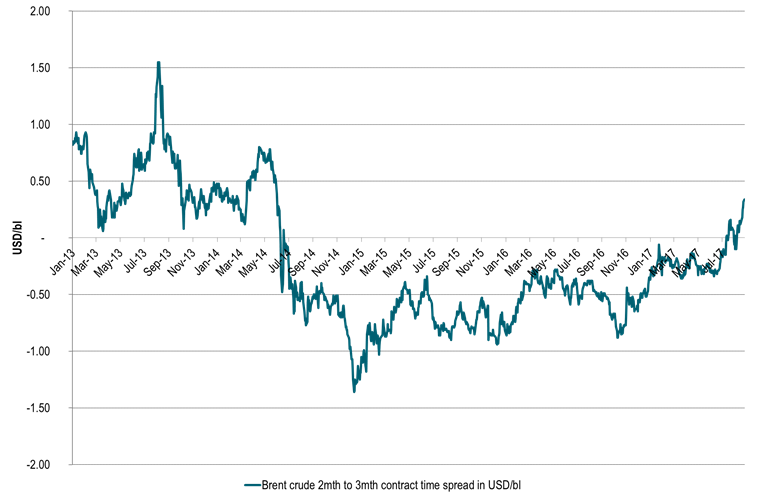

Ch3: Brent crude two to three month price spread. Bending, bending further into backwardation

Ch4: But WTI is left in contango due to rising production, hurricane Harvey damages and lack of export capacity out of Cushing

Ch5: Hurricane Harvey induced outage of refineries is blowing over

Ch6: Inventories in weekly data continues to decline steeply

Down 173 mb since mid-March (-0.9 mb/d on average)

Ch7: Net long Brent spec (last data point published last week) at 46/52 week high

Ch8: Net long Brent spec (last data point published last week) at 46/52 week high

When specs take money off the table eventually it will pull prices lower as well

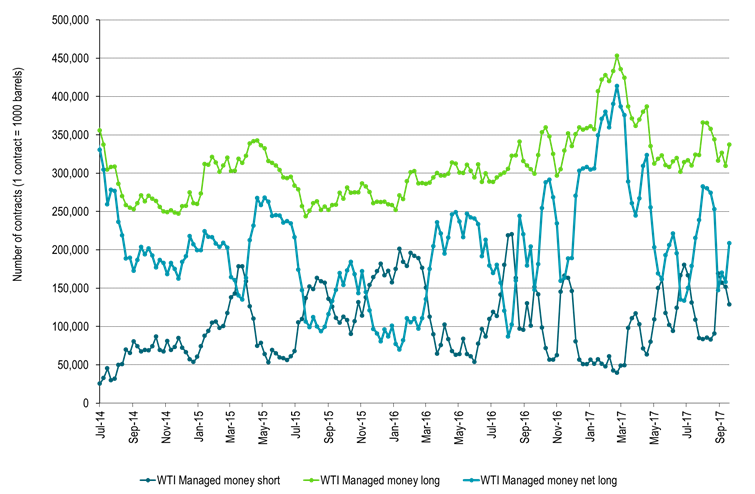

Ch9: WTI specs inching higher, but not same optimism as in Brent as WTI crude curve is in contango

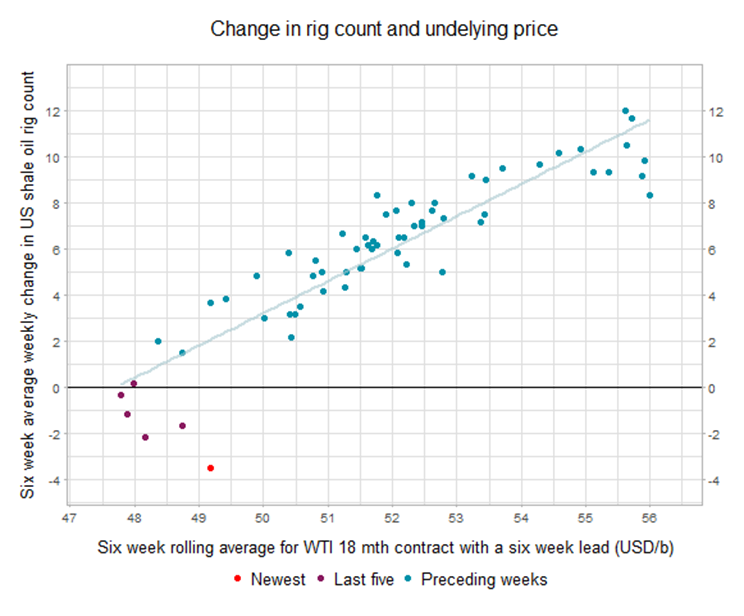

Ch10: The number of US oil rigs is declining. Down five out of six weeks

It is saying WTI @ $50/b is not enough. We’ll pull rigs out of the market at that price

When the rally for Brent backwardation ends this message will help to lift Brent 2019 and 2020 prices

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking