Analys

Brent crude tipping over the technical abyss

Brent crude ydy closed down 1.5% at $58.94/bl. That was the lowest level since early January, below the lows from June and below the technically important Fibonacci price level of $59.74/bl below which there is no real support before the $50/bl line. This abyss or lack of technical support below $59.74/bl has been high on the radar of many of our customers for a long time and now we have broken down below that level with an open abyss down to the $50/bl line.

Oil producers may pray that tight front end fundamentals and continued declining US crude oil stocks may save them but as of now the bearish and deteriorating global macro situation seems to have the upper hand, pushing lower and lower.

US crude oil stocks have now fallen 7 weeks in a row since early June with a total decline of 49 million barrels. API ydy released partial, indicative numbers pointing to yet another weekly draw in US crude stocks of 3.4 m bl, with Cushing crude stocks down 1.6 m bl, Gasoline stocks down 1.1 m bl and distillates stocks up 1.2 m bl.

So US crude oil stocks are likely to continue lower together with a range of other bullish elements: Mid-East geopolitical risk is likely to continue at an elevated level, OPEC+ will likely continue to hold back, US production growth will continue to slow further and refinery margins are likely to stay strong due to the IMO 2020 event. But the bearish macro sentiment still has the upper hand for now pushing lower.

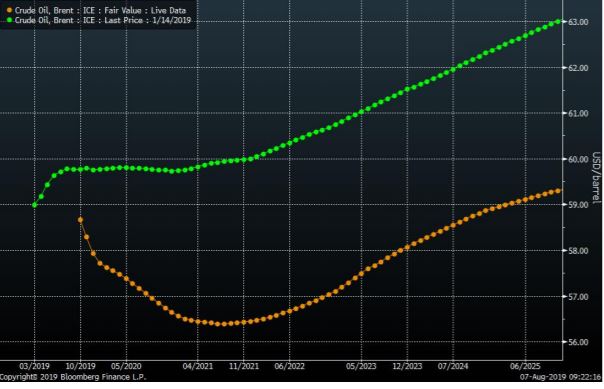

Last time we were at the current price level in early January the spot market was plentiful but the market was optimistic of the future. Now the spot market is tight with both the Brent and WTI crude curves in front-end backwardation. But since the market is very pessimistic of the future macro situation and future oil demand it has pushed the whole front end of the crude oil curve lower so that backwardated part of the curve now is below the longer dated contracts.

This is unlikely to change before we either get a major outage of supply giving an even stronger bullish force to the front end of the market or the macro sentiment turns from a bearish trend to a bullish trend. A partial or full stop in the flow of oil out of the Strait of Hurmuz would be bullish supply event which undoubtedly would drive the front end to the sky. A full or partial resolution to the ongoing US – China trade war would definitely be a turn to the positive from the macro side.

For now the bearish macro sentiment continues to push down the whole forward curve for both Brent and WTI paying little attention of the tight front end of the market. The US Fed did not rescue the macro situation. It was not enough to change the direction of the cooling global growth trend. Instead Donald Trump has upped the US – China trade war making it all worse.

While slowing US crude oil production growth is good for the global oil market balance it is not entirely positive for Brent crude in the first round of events.

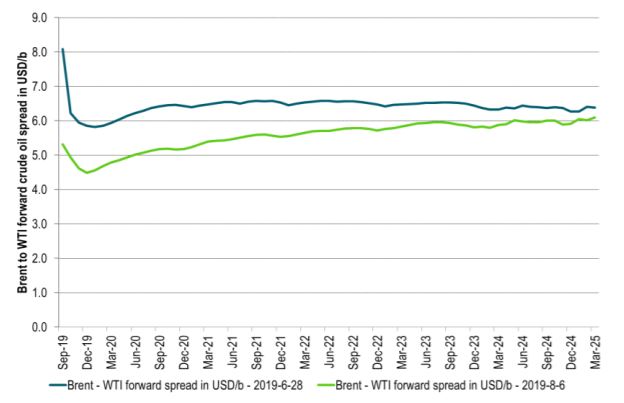

Much more US pipeline capacity from the Permian basin to the US Gulf in combination with slowing US crude oil production growth implies that Brent crude oil prices will move much closer to the WTI crude curve. I.e. global oil producers will lose the Brent crude oil premium over WTI which averaged $8.3/bl on average so far in 2019 and averaged $6.8/bl in 2018.

Lately we have seen marginal cost for transporting oil from the Permian to the US Gulf of $2.5/bl. So that is probably the Brent to WTI price spread we are heading towards.

The ongoing price dynamics shows how difficult it is for OPEC+ to prop up prices through production cuts in the face of cooling global growth. It was much easier when they initiated cuts in late 2016 with strong tailwind from accelerating global growth.

Ch1: The Brent crude oil forward curves in early January (green) versus now (yellow). Plentiful spot supply in January but coupled with a fairly positive view of the future. Today the spot market is tight in the front but the bearish macro sentiment is very bad. I.e. deep concerns for future demand is pushing down the whole forward crude curve

Ch2: Brent crude losing more and more of its premium over WTI. Here the spread between the two forward curves at the end of June versus the close yesterday. Brent had a premium of $6.8/bl in 2018 and $8.3/bl ytd average in 2019.

Ch3: Brent front month breaking down below the 38.2% Fibo level with basically open space down to the $50/bl line. I.e. Brent crude oil price is extremely vulnerable to the downside and to further deterioration in the global macro sentiment.