Analys

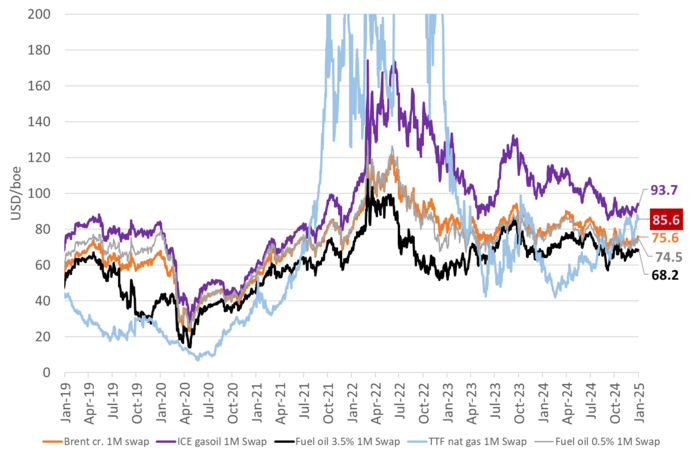

Brent crude falling back along with softer nat gas prices

Brent crude jumped USD 2.3/Brent crude to Friday 3 January. got off to a good start in 2025 with a gain of USD 2.3/b from Friday 27 December to Friday January 3. The close on Friday at USD 76.51/b was the highest close since October. Brent also rallied through the 100-day moving average last week with that measure now sitting at USD 74.35/b which is not too far below the current price after all. The RSI has crawled closer to overbought (70) with latest level at 63.7. This morning Brent is falling back 0.5% to USD 76.2/b along with softer industrial metals and initially at least a decline in EU nat gas prices of 2-3%.

Cold weather and end to Russian piped gas helped Brent higher. Brent crude probably got some help from lower US crude stocks, colder than normal weather in North-West Europe and the US, a rally in EU nat gas prices (cold weather and end of Russian piped gas to EU) and higher oil refining margins because of all that.

OPEC+ proved strong resolve on supply restraint in 2024. Supportive for 2025 outlook. On the positive side we have solid resolve by OPEC+ to keep oil prices steady. They have confirmed and reconfirmed this solid resolve again and again over the past half year by postponing heralded production hikes time and time again. There will be no increase in Q1-25, and then the latest plan is to increase production gradually by 2.2 m b/d over 18 months from April. If need be, they will likely postpone yet again if needed when we get towards April.

Curbs to Iranian oil exports are necessary for US oil production to rise strongly. Donald Trump has promised a large increase in US crude oil production. That is however only possible if oil prices do not fall. If the US embarked on a rapid increase in its crude oil production of 3 m b/d then OPEC+ would throw in the towel of production cuts, the oil price would crash, and US production would fall by 3 m b/d rather than to rise by 3 m b/d. US oil producers knows this very well and Donald Trump probably also understands this. The only possible way for a significant production increase in US crude oil production without crashing the price is if someone else in the global oil supply leaves the party. In the eyes of Donald Trump, that someone is probably Iran. Donald Trump has forced Iranian oil exports out of the market once before in 2018 when they went from around 2 m b/d to close to zero. A repeat of this would probably require cooperation from China. In a trade deal between the US and China it is not at all impossible with such a clause (that China stops importing oil from Iran). China may be content if oil supply is plentiful and affordable. And if troubles arise, China could always restart imports of Iranian crude oil.

China weakness is still disturbing. Chinese crude oil imports rose 1.3 m b/d to November as Chinese Teapot refineries got to borrow quotas from 2025. That gave strength to crude oil at the end of the year. But oil products supplied in China were down 380 k b/d y/y in November (Argus) to an estimated 15.3 m b/d. Chinese economy turning the corner in 2025 would blow away a lot of the bearish sentiment in the market.

Cold weather and an end to piped nat gas from Russia has probably helped Brent crude higher into the new year. Higher heating oil demand and higher refinery margins gave helped to lift Brent crude higher. Fuel oil 3.5%, 0.5% as well as Brent crude is now cheaper than nat gas. Historically very unusual except for the period since the Russian invasion of Ukraine.

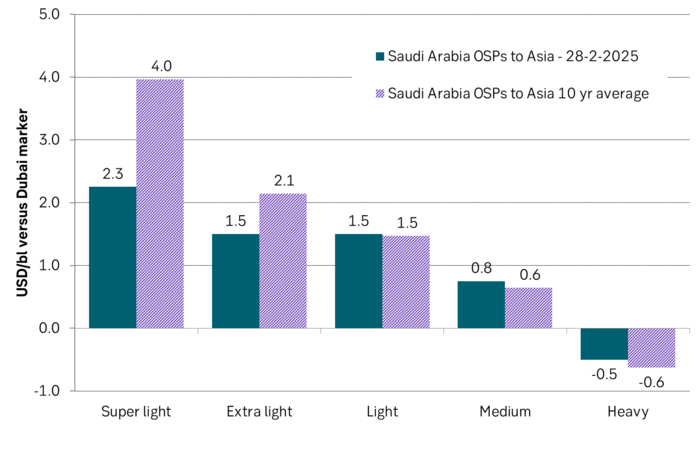

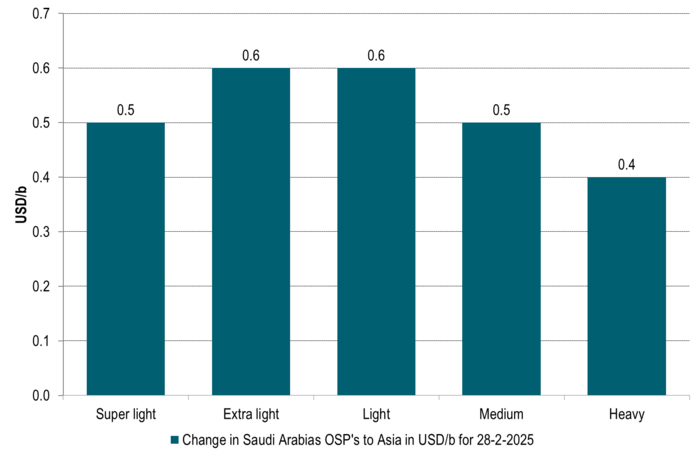

Saudi Arabia lifted its Official Selling Prices (OSPs) to Asia by USD 0.5-0.6/b. Proves confidence that they will sell their crude even at higher relative prices to the Dubai Marker. Stronger front-end backwardation in the Dubai marker in December is probably the reason.

Saudi Arabia’s OSPs to Asia for February are softer than 10yr average in the light-ends as the US shale oil boom has hurt that part, while OSPs are slightly stronger than the 10yr for the heavy end of the complex.