Analys

Bearish macro backdrop but bull-drivers inch it higher

Brent crude moved up 1.2% over the past week to a close of $66.67/bl yesterday. The move was mostly in the front part of the curve thus driving the curve more into backwardation. WTI lightly followed suite with a gain of 0.5% closing at $56.87/bl ydy.

As usual a range of oil price drivers are coming at the oil price from different angels.

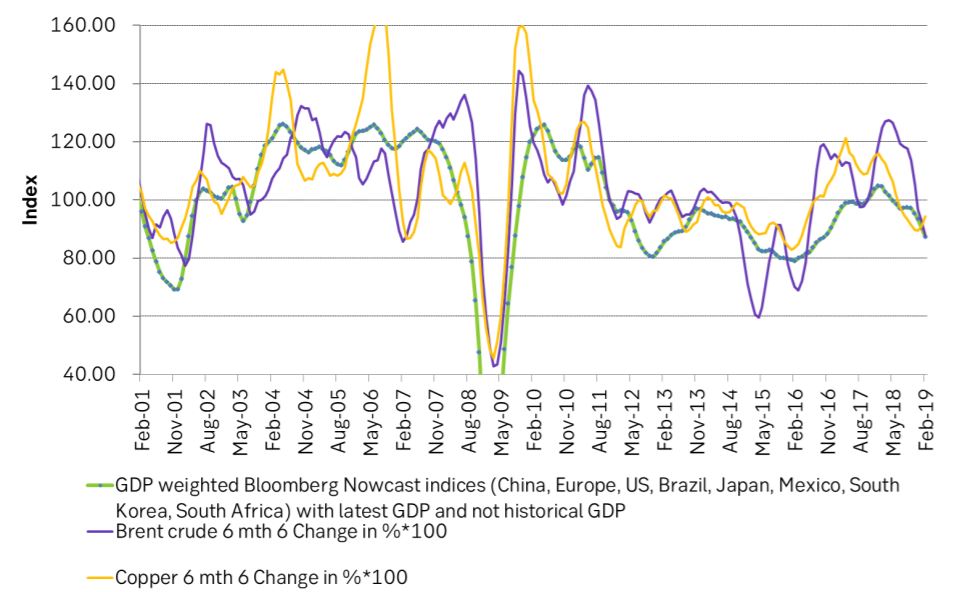

A deteriorating global macro-economic backdrop is a bearish drag on the oil price though oil demand growth still looks healthy.

On the bullish side we have a rapidly deteriorating situation in Venezuela with recent production down as low as 0.5 m bl/d. People no longer have time to protest against Maduro as they instead have to run around looking for food. US oil rig count is declining with shale oil focus shifting increasingly towards “Show me the money”. I.e. they cannot any longer grow production through piling up more debt.

Further on the bull side OPEC+ continues to deliver on pledged cuts and will likely decide to manage the market also in H2-19 when they meet in April.

A possible NOPEC legislation in the US could be a risk to the downside for the oil price. It would allow the US government to sue the cartel. It could potentially drive OPEC into all-in production mode and sink the oil price. Though it would prevent OPEC from cooperating on supply it would not prevent Saudi Arabia from intervening in the oil market alone which to a large degree is what they are doing anyway.

If the NOPEC legislation passes with a positive vote it would be a slap in the face of OPEC in general and Saudi Arabia specifically. It would be another nail in the coffin of the long lasting and close relationship and friendship between the US and Saudi Arabia. It would drive Saudi Arabia closer to both Russia and China. Given that future oil exports clearly will be towards Asia and China it might also help to warm Saudi Arabia to the thought of selling oil to China in CNY down the road.

Pompeo recently stated that the US is committed to drive Iranian oil exports to zero “when market conditions permit it”. So if the oil price is high the waivers will roll forward with no tightening of sanctions. If the oil price is low then sanctions will tighten and the oil price will rise. I.e. the US sanctions towards Iran now suddenly works as a price stabilizer.

On Brent crude price action and levels: Sideways at around $65/bl since mid-February. It is now inching closer and closer to the 50% level at $67.85/bl. From there it is not far up to the 200 ma level at $69.61/bl and then again a short distance up to the 61.8% Fibo level at $71.88/bl. I.e. some more bullish catalyst and we could in short distance break up through three important levels. It is currently quite a distance down to 38.2% at $63.82/bl.

Ch1:On Brent crude price action and levels: Sideways between 38.2 and 50% Fibo levels since mid-February. Inching closer and closer to the 50% level at $67.85/bl. From there it is not far up to the 200 ma level at $69.61/bl and then again a short distance up to the 61.8% Fibo level at $71.88/bl. I.e. some more bullish catalyst and we could in short distance break up through three important levels. Currently quite a distance down to 38.2% at $63.82/bl

Ch2: Still a bearishly developing macro-economic backdrop