Analys

An age of unprecedented oil volatility

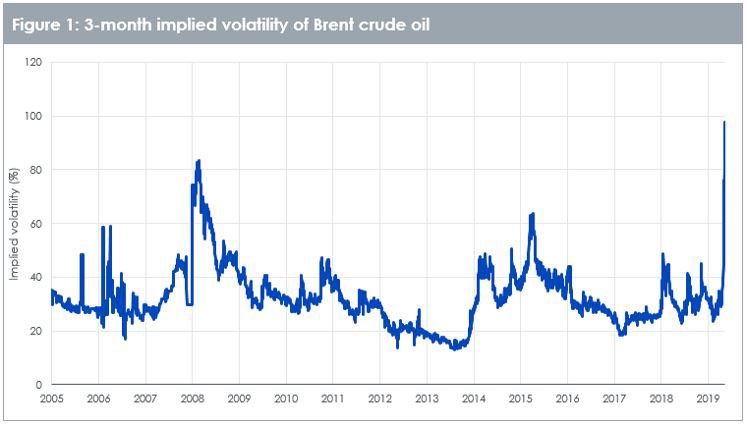

We are living in a time of unprecedented volatility in oil. That is the consequence of a twin shock: both demand is collapsing and supply is rising. Oil prices are now more volatile than they were in the Great Financial Crisis (that started in 2008) or the oil price war of 2014-2016.

The sheer drop in prices over a short timespan has rarely been seen before. Neither in 2008 nor 2014 did we see such a sharp decline. If we were to annualise the price decline we have seen in the past two weeks, it will outpace the price declines of 2008 and 2014.

The protagonist seeks vengeance

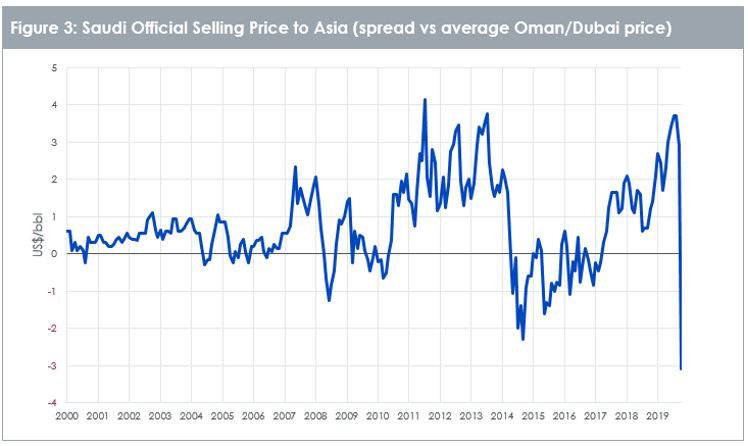

As we discussed in Post OPEC meeting note -OPEC’s Greek Tragedy, the events of 5th and 6th March profoundly changed the oil markets. The Organization of the Petroleum Exporting Countries (OPEC) and its partner countries (collectively known as OPEC+) failed to reach an agreement on policy. We believe that OPEC is functionally dead as a result. Since 2017, OPEC has been reliant on Russia to endorse OPEC’s policy and even though Russia has habitually failed to follow through with implementation of quotas in full, the unity has been symbolically important as Saudi Arabia has been willing to cut more than its fair share to compensate. With Russia’s betrayal to this alliance, Saudi Arabia is now slashing prices and raising production. The chart below shows the Saudi official selling price of Arab light crude oil to Asia as a spread over the average cash Dubai price and Oman crude oil future price. Saudi Arabia is selling oil at close to a US$3/bbl discount to its peers. After Saudi Arabia refused to participate in the Joint Technical Committee originally scheduled for March 18th, the meeting was cancelled.

To be clear, Saudi Arabia now has its own agenda: to inflict maximum pain on Russia and it doesn’t seem to care which casualties it will take with it. Saudi Arabia intends to expand capacity to 13 million barrels per day from 12 million barrels per day currently. Saudi Arabia was producing 9.6 million barrels per day in February 2020. If Saudi Arabia produces at capacity, the world will be awash with oil.

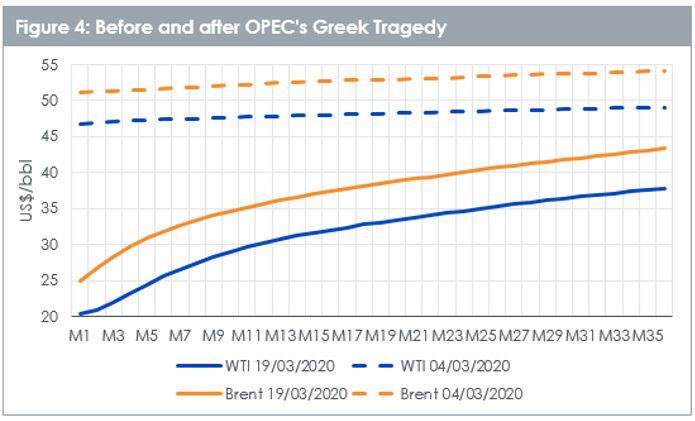

Twin shocks drive extreme contango

This supply shock is coming at a time when demand is severely hampered by COVID19. This double-whammy has caused extreme contango in the oil markets. The day before the OPEC meetings, oil was in mild contango, with the difference between 1st and 36th contract only between US$2bbl and US$3bbl (WTI and Brent). On 19th March 2020, the contango has become extreme, with the difference between 1st and 36th contract between US$17/bbl and US$18/bbl (WTI and Brent). Only in the depths of the 2008 Great Financial Crisis had we seen contango this deep.

Where will this end?

The pain from the 2014-2016 oil price war is still raw in OPEC countries’ memories, yet it failed to deter Saudi Arabia from engaging in a fresh price war with Russia. We don’t think that the group will change course anytime soon. We don’t think the rest of OPEC can operate without Saudi Arabia. Saudi has been responsible for most of the group’s swing-production – i.e. building spare production capacity that can be used in times of demand surges or supply outages.

We doubt that the rest of the world will be able to adjust to this new reality quickly. Most global oil companies do not use the Saudi Aramco (state oil company in Saudi Arabia) model of keeping redundant capacity. Shuttering production for most oil companies is slow and costly to the point of putting the company’s finances under fatal strain.

There have been discussions, confirmed by US Energy Secretary Dan Brouillette of the possibility of a joint US-Saudi oil alliance. It was only one of many strategies discussed by policy makers in the US and we doubt that the US will partake in a cartel that it has been criticizing for decades. But desperate times may call for desperate measures. After all, the OPEC cartel was designed on the Texan oil practices from the 1930s to 1970s2.

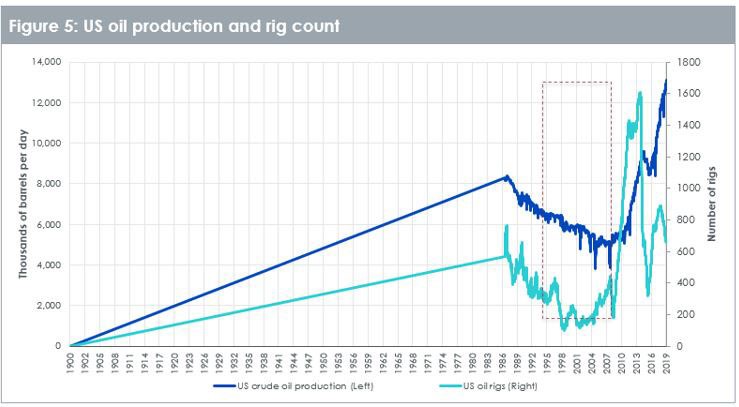

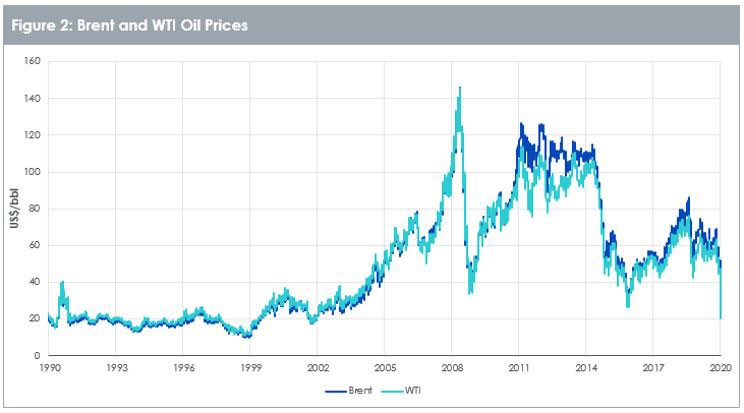

More likely, we believe that the US will allow market economics to trim back on production. Our working assumption is that the breakeven price for oil production in the US is US$50/bbl. With WTI prices at US$25/bbl at the time of writing, US oil producers are going to suffer and we expect bankruptcies to soar. In the 2014-2016 oil price war, rigs in operation in the US fell by two-thirds. The US is dominated by shale oil production, which does not have the same lengthy lead times for switching on and off production as traditional oil production. But the decline in rigs came at a time when technological improvements to production techniques were rising fast. So, the ultimate decline in production was not that steep. This time, rigs in operation which have already been declining for a year could be matched by commensurate declines in production. The US could in effect become the world’s new swing producer.