Analys

Almost unanimous bearish consensus for 2020

Brent crude gained 2.4% on Friday with a close at $60.51/bl on the back of a partial US – China trade deal, Brexit optimism as well as a missile attack on the Iranian oil tanker near Jeddah in the Red Sea. The most important consequence of the “trade deal” was probably the cancellation of the planned US tariff increase on 15 October though with no guarantee in that the planned US December tariffs will be scrapped.

This morning Brent crude is pulling back 0.8% to $60/bl as the concerns over the attacks on the Iranian oil tanker last week are evaporating and the optimism over the US-China trade deal is fading. Disappointing Chinese imports/exports data with imports down 8.5% YoY and exports down 3.2% YoY is also weighing on the oil price as the temperature of the Chinese economy is of high importance to the oil market.

Chinese declined 2.2% from Aug to Sep in million ton per month measure. However, given that there are 3.3% more days in Aug than in Sep it still meant that in m bl/d terms Chinese crude imports went up by 1.1% MoM as well as +10.8% YoY.

A part reason for the limited impact on oil prices from last week’s missile attack on the Iranian oil tanker is probably due to the fact that Saudi Arabia now has initiated talks with the Houthi rebels in Yemen for the first time in two years. The UAE has been pulling out of Yemen since July and has left Saudi Arabia more and more alone in its endeavour there. The attack on Saudi Arabia’s oil infrastructure (Abqaiq and the oil field Khurais) some weeks ago also proved that Saudi Arabia is highly vulnerable and basically unable to protect its oil infrastructure from such attacks. The Houthi rebels were the once who claimed responsibility for the attacks on Saudi Arabia a few weeks ago. Suspicions though still go towards Iran. So solving the Yemen issue may not really solve the main problem in the Middle East.

At the Oil and Money conference there seemed to be an almost unanimous verdict that the risk to the oil price was to the downside amid plentiful supply growth in combination with a cooling global economy. That the oil price would be under bearish pressure for the coming months and would be lower than it is now in 12 months’ time. Assessment was still that the geopolitical risk is high at the moment and that the oil market is not pricing in any risk premium for this at the moment.

OPEC’s Secretary-General, Mohammad Barkindo did however counter these concerns by stating that the organisation will do “whatever it takes” to avoid oil price slump next year. Putin’s visit to Saudi Arabia today underlines this statement and adds credibility to the continued relationship and cooperation between Saudi Arabia and Russia. Bullishly the market does not seem to care too much about this today though.

During repeated rounds of sell-offs since the beginning of August the front month Brent price has only briefly traded below $58/bl. The front-end of the Brent crude curve has been in consistent backwardation reflecting a tight physical market. Still the oil market expert verdict continues to be “BEARISH”, both for the nearest months and for next year.

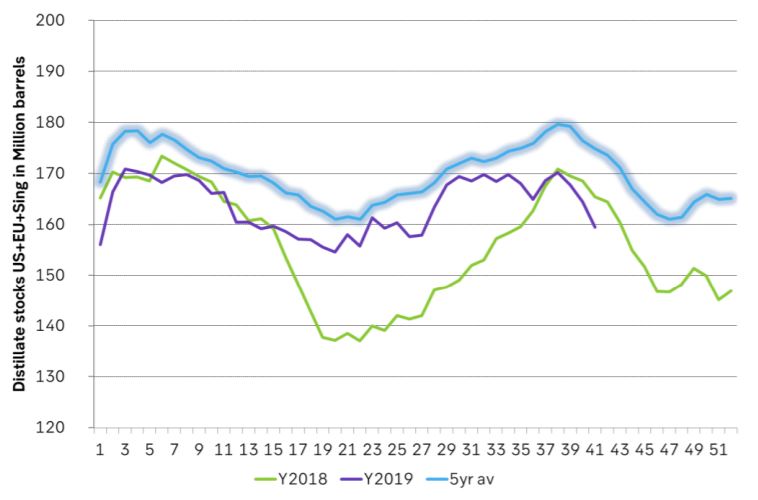

We do agree that the oil market has some headwinds in the near term with still robust US shale oil production growth amid a slowing global economy. The physical crude oil market is in spite of this actually tight right here and now. Middle distillate stocks are below normal as we head into the northern hemisphere winter season as well as the IMO-2020 switchover in January and the geopolitical risk is unusually high with no noticeable risk premium in oil prices to show for.

We believe that the IMO-2020 regulations in global shipping will have a tightening effect on the global oil market in 2020. Further that marginal US shale oil production growth will slow sharply next year and that the “US shale oil reaction function” versus the oil price is changing with a higher price needed before drilling activity moves higher.

One might also wonder whether the most bearish point in time macro-wise may be now and the nearest 3-6 months rather than 2020 as a whole. That 2020 may to a larger degree be dominated by stimulus and revival rather than further growth deterioration and thus that the more or less current almost unanimous bearish 2020 oil market verdict may miss the mark when it comes to the average oil price delivered in 2020.

Ch1: Middle distillates in US, EU and Sing (weekly data) are well below normal are falling sharply as we are moving into the Northern hemisphere winter as well as the IMO-2020 switchover in January

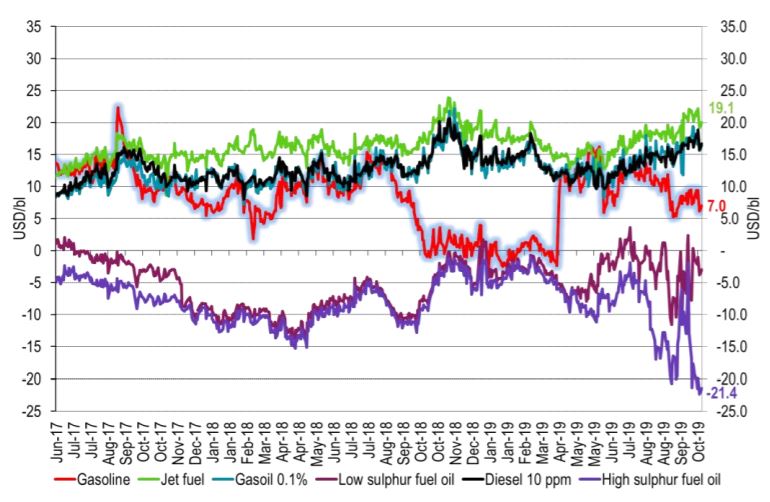

Ch2: High sulphur bunker oil refinery margins have crashed as we now are moving closer and closer to the IMO-2020 switchover in January. The middle distillate cracks have been ticking higher and higher since June and we expect more upside. The collapsing HFO 3.5% crack is the physical fingerprint IMO-2020 is coming and has started to rock the boat.