Analys

A neat OPEC+ deal: Carrot and Stick

OPEC+ struck a neat deal in our view at the end of last week. The carrot was that if all participants to the deal comply with their individual caps then Saudi Arabia will cut an additional 400 k bl/d versus its obligation. The stick is that the latest deal only stretches to March 2020 and then needs to be reviewed and renewed: “Get in line or you’ll be suffering already in March. Free-riding will be short-lived from now onwards.”

I.e. they will all receive the benefit of Saudi Arabia’s additional self-imposed restricted cap. However, if they do not comply with their own individual caps they will quickly get caught and brought to justice already in March. I.e. there is significant leveraged upside to comply (windfall from Saudi Arabia’s additional 400 k bl/d cut) and significant downside risk of not complying.

An ultimatum is of course always problematic in the sense that you might have to execute an action you don’t really want to. The main three offenders so far have been Russia, Iraq and Nigeria. Together the offenders produced 0.5 m bl/d above their caps in October 2019 so bringing them into line will help a lot versus overall production.

The new deal means that the risk for a strong stock-build in H1-2020 is significantly reduced and so is the risk for a sharp price drop towards the lower $50ies/bl for Brent.

If producers do not comply with their new caps in Q1-20 then we might be in for some bumps in March as Saudi Arabia then would retract its additional 400 k bl/d cut. It would however not necessarily imply that the whole deal falls apart other than the retraction of the 400 k bl/d additional Saudi cuts.

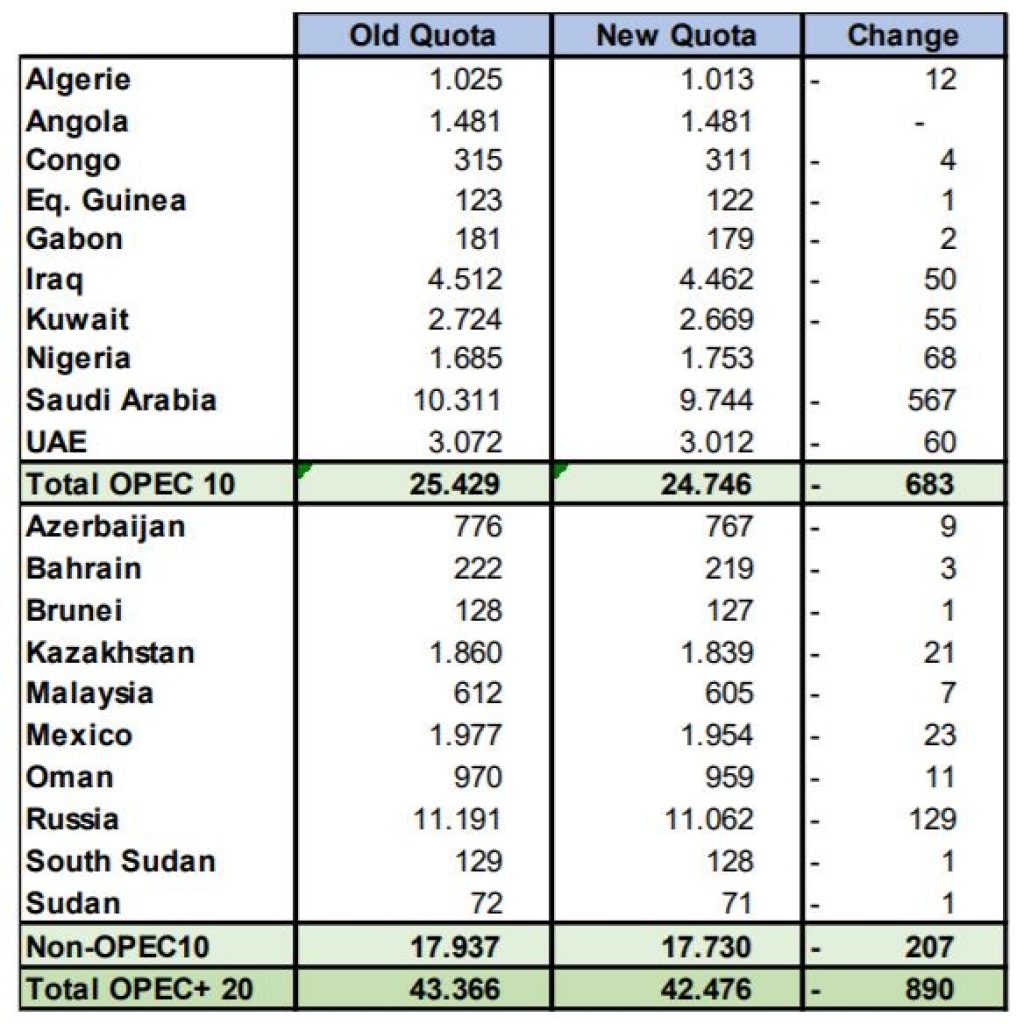

The sum of reductions in the deal from December 2018 equalled a 1,2 m bl/d reduction from individual 2018 October production levels. The additional cuts agreed last week in sum added 0.5 m bl/d to these cuts and then Saudi Arabia added the carrot of an additional self-imposed cut of 0.4 m bl/d. Thus, in total a reduction of 2,1 m bl/d from 2018 October prod. levels.

What skews the picture is of course the fact they all boosted production in the run-up to the OPEC+ meeting in December 2018. As a result, all these production cuts are coming from close to record high monthly values.

The media is constantly bashing OPEC and OPEC+ plus for cutting and cutting but getting nowhere. Fact is that there has not been a lot of cuts except for the misfortunes of Libya, Iran, Venezuela and Mexico.

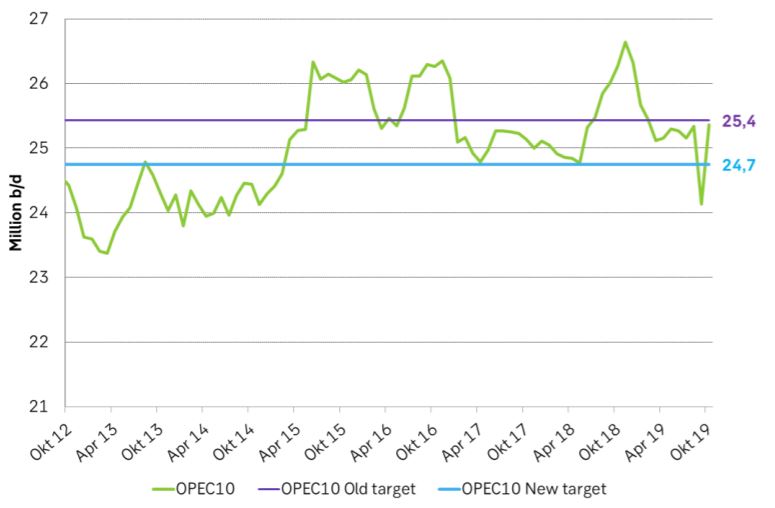

If all OPEC 10 members comply with their new production caps then they will produce only 0.7 m bl/d (-2.7%) below their 5 year average. The 10 non-OPEC cooperating countries would produce 0.5% above their 5-year average while the total OPEC+ (19) would produce only 1.4% below their 5-year average production.

Libya, Iran, Venezuela and Mexico are suffering but the others aren’t really suffering very much. They are only cutting their production at the margin. Even Saudi Arabia which is cutting the most on the face of it will produce just 4% below its 5-year average under the new cap. Its 5-year average production is 10.14 m bl/d while its new self-imposed cap is 9.75 m bl/d.

First and foremost, the deal from last week means that OPEC+ is not dropping the ball. It is not letting oil flow freely. It will work actively to prevent an above normal stock-building in H1-2020. High and above normal inventory levels mean a spot price discount versus longer dated prices. Normal to low inventories means a spot price premium of $5-10/bl. That is why OPEC+ so strongly wants to avoid a solid stock building in H1-2020. The longer dated price anchor is $60/bl. So a “premium” situation will hand oil producers a price of $65-70/bl while a surplus inventory situation would give them a $50-55/bl price level.

Adding some confusion to the OPEC mathematics: Ecuador is leaving OPEC in January. The 10 non-OPEC cooperating countries will subtract natural gas liquids from production before applying the new quotas => some problems with historical data.

Table one: Old and new quotas. We have not yet seen the new individual quotas for the non-OPEC countries. These will be adjusted versus new production levels excluding natural gas liquids. The reduction decided in December 2018 was 1.2 m bl/d from Oct-2018 levels. The new cuts are added to these with first 500 k bl/d divided amongst all members and then Saudi Arabia takes on an additional 400 k bl/d cut on top of that. Do note that Saudi Arabia’s average production from Jan-2019 to Oct-2019 was 9.78 m bl/d versus its new cap of 9.74 m bl/d.

Ch1: OPEC 10 production versus old and new cap in m bl/d