Analys

A moment in markets – was it a shift in sentiment?

On Tuesday, 11 August, gold fell by over 5% and silver retreated nearly 15% prompting investors to wonder if there had been a material shift in market sentiment. Are defensive hedges no longer required? How important are gold and silver as risk sentiment improves? A glance towards the wider market, and indeed economic fundaments, can help answer these questions.

A wider look at the market

Here is a look at how other defensive and risk assets have behaved since 11 August (‘the day’):

- Defensive assets:

- US dollar bounced up on the day – this triggered the initial sell-off in other safe-haven assets. It was unable to sustain its recovery and remains weak so far this year. The dollar basket is down around 3.7% year-to-date.

- 10-year US treasury yields added over 10 basis points over three days since the day but remain close to record lows at around 0.68% compared to around 1.9% at the start of the year.

- Risk assets:

- The S&P 500 has largely been flat since the day but generally been on a steady upward trajectory since March.

- The Euro Stoxx 50 Index has outpaced the S&P 500 Index since the day and is up around 1.4% since the close of 10 August (in EUR terms).

The question of sentiment

How will a shift in economic and risk sentiment affect asset markets? Consider the following scenarios:

- If sentiment improves: Risk assets, such as equities and cyclical commodities, will certainly benefit from an improvement in economic growth sentiment. And while treasuries may pull back, gold will remain in demand as a hedge against any uptick in inflation. Silver – on account of its high correlation with gold (historically between 0.7 and 0.8), and strong industrial demand (more than half of silver’s use comes from industrial applications including electronics, medical equipment and solar power generation) – will continue to offer a cautious play on the cyclical recovery.

- If sentiment deteriorates: Such a scenario will naturally not be conducive for risk assets. Having said that, US equities have shown meaningful resilience year-to-date owing to strong policy support and tech sector strength. A murkier economic outlook will bring the defensive elements of gold and silver into play.

Did sentiment shift last week?

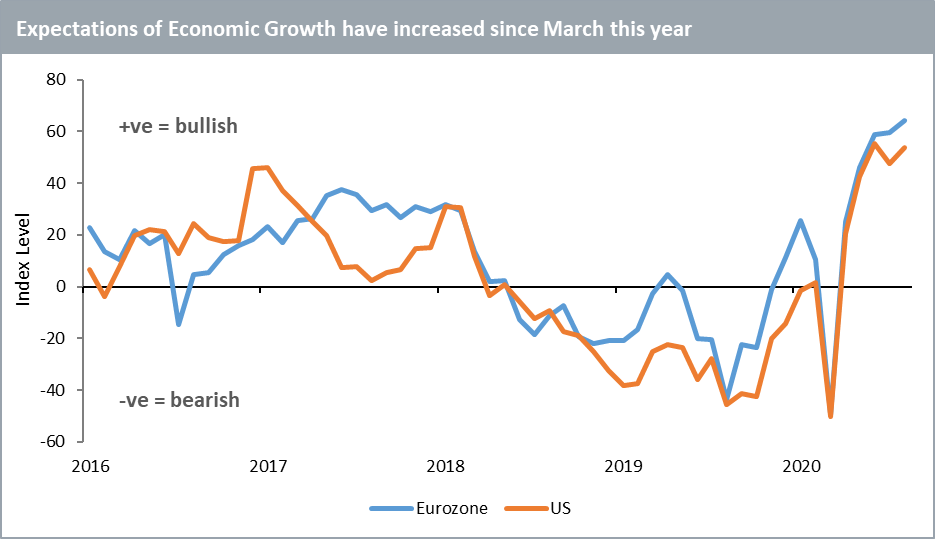

Sentiment – both among economists and in markets – has been improving since the peak of the crisis in March (see figure above). The release of the ZEW USA and Eurozone Expectations of Economic Growth Indices on Tuesday 11 August merely point to a continuation in the trend. The reversal in the CBOE Volatility Index (VIX) since March presents a similar picture of improving confidence in markets. Thus, sentiment did not shift last week but continued along the path it has been on since March.

After the acute contraction in the second quarter, the global economic recovery is likely to be slow and protracted. Gradually improving economic sentiment and a challenging outlook are not mutually exclusive. In fact, they are the ingredients of a steady, U-shaped economic recovery – our central scenario at WisdomTree.

Gold and silver are already making gains this week highlighting how they have become integral components of diversified portfolios. In an age of low to negative interest rates and uncertainty as the global economy recovers, they offer balance by participating in the upside but offering protection in the downside. Strategic investors would do well to ignore momentary volatility and tactical investors are likely to see the price declines, such as those of last week, as buying opportunities.

Mobeen Tahir, Associate Director, Research, WisdomTree

Unless otherwise stated data is source from WisdomTree, Bloomberg as of 17 August 2020.